ACC 100 Lecture Notes - Capital Account, Retained Earnings, Income Statement

4 Nov 2012

School

Department

Course

Professor

Document Summary

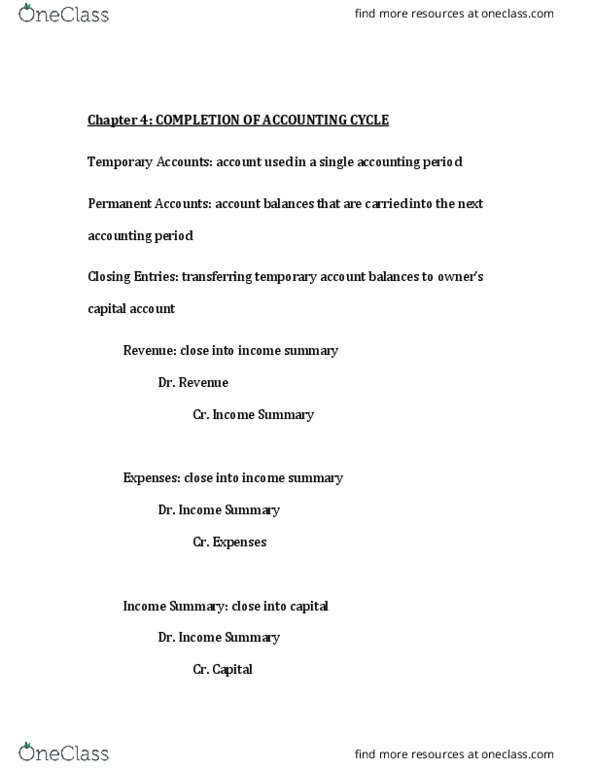

To update the balance in the owner"s capital account, accountants close revenue, expense, and drawing accounts at the end of each fiscal year or, occasionally, at the end of each accounting period. For this reason, these types of accounts are calledtemporary or nominal accounts. Assets, liabilities, and the owner"s capital account, in contrast, are called permanent or real accounts because their ending balance in one accounting period is always the starting balance in the subsequent accounting period. When an accountant closes an account, the account balance returns to zero. Starting with zero balances in the temporary accounts each year makes it easier to track revenues, expenses, and withdrawals and to compare them from one year to the next. The purpose of the income summary account is simply to keep the permanent owner"s capital or retained earnings account uncluttered: close the owner"s drawing account to the owner"s capital account.