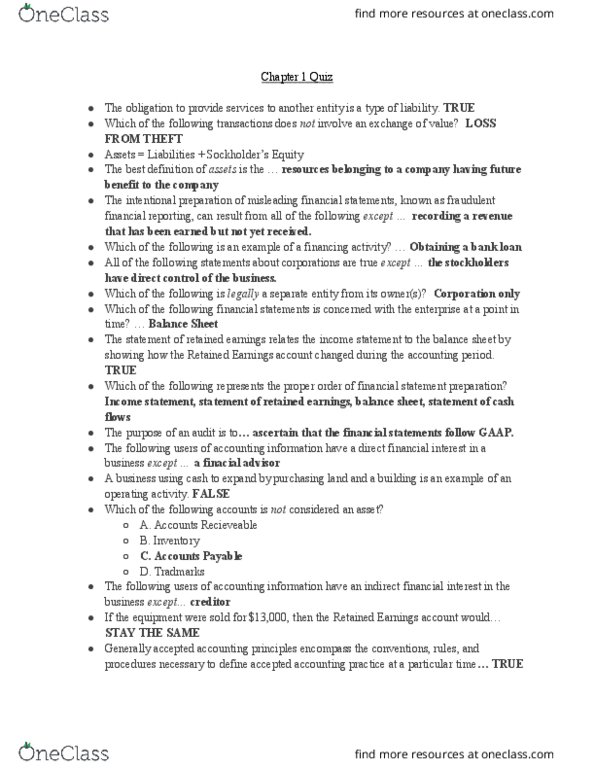

Bessrawl Corporation is a U.S.-based company that prepares its consolidated financialstatements in

accordance with U.S. GAAP. The company reported income in 2020 of $1,000,000 and

stockholders’ equity at December 31, 2020, of $8,000,000.

The CFO of Bessrawl has learned that the U.S. Securities and Exchange Commission is

considering requiring U.S. companies to use IFRS in preparing consolidated financial statements.

The company wishes to determine the impact that a switch to IFRS would have on its financial

statements and has engaged you to prepare a reconciliation of income and stockholders’ equity from

U.S. GAAP to IFRS. You have identified the following five areas in which Bessrawl’s accounting

principles is based on U.S. GAAP differ from IFRS.

1. Inventory

2. Property, plant, and equipment

3. Intangible assets

4. Research and development costs

5. Sale-and-leaseback transaction

Bessrawl provides the following information with respect to each of these accounting differences.

Inventory

At year-end 2020, inventory had a historical cost of $250,000, a replacement cost of $180,000, a net

realizable value of $190,000, and a normal profit margin of 20 percent.

Property, Plant, and Equipment

The company acquired a building at the beginning of 2019 at a cost of $2,750,000. The building

has an estimated useful life of 25 years, an estimated residual value of $250,000, and is being

depreciated on a straight-line basis. At the beginning of 2020, the building was appraised and

determined to have a fair value of $3,250,000. There is no change in estimated useful life or residual

value. In a switch to IFRS, the company would use the reevaluation model in IAS 16 to determine

the carrying value of property, plant, and equipment subsequent to acquisition.

Intangible Assets

As part of a business combination in 2017, the company acquired a brand with a fair value of

$40,000. The brand is classified as an intangible asset with an indefinite life. At year-end 2020, the

brand is determined to have a selling price of $35,000 with zero cost to sell. Expected future cash

flows from continued use of the brand are $42,000 and the present value of the expected future cash

flows is $34,000.

Research and Development Costs

The company incurred research and development costs of $200,000 in 2020. Of this amount, 40

percent related to development activities subsequent to the point at which criteria had been met

indicating that an intangible asset existed. As of the end of the 2020, development of the new

product had not been completed.

3

Sale-and-Leaseback

In January 2018, the company realized a gain of the sale-and-leaseback of an office building in the

amount of $150,000. The lease is accounted for as an operating lease, and the term of the lease is

five years.

Required

a) Prepare a reconciliation schedule to convert 2020 income, and December 31, 2020, stockholders’

equity from a U.S. GAAP basis to IFRS. Ignore income taxes. Prepare a note to explain each

adjustment made in the reconciliation schedule.

b) Discuss each relevant accounting standards with references to journal article(s) by using

disclosure examples of companies.

Bessrawl Corporation is a U.S.-based company that prepares its consolidated financialstatements in

accordance with U.S. GAAP. The company reported income in 2020 of $1,000,000 and

stockholders’ equity at December 31, 2020, of $8,000,000.

The CFO of Bessrawl has learned that the U.S. Securities and Exchange Commission is

considering requiring U.S. companies to use IFRS in preparing consolidated financial statements.

The company wishes to determine the impact that a switch to IFRS would have on its financial

statements and has engaged you to prepare a reconciliation of income and stockholders’ equity from

U.S. GAAP to IFRS. You have identified the following five areas in which Bessrawl’s accounting

principles is based on U.S. GAAP differ from IFRS.

1. Inventory

2. Property, plant, and equipment

3. Intangible assets

4. Research and development costs

5. Sale-and-leaseback transaction

Bessrawl provides the following information with respect to each of these accounting differences.

Inventory

At year-end 2020, inventory had a historical cost of $250,000, a replacement cost of $180,000, a net

realizable value of $190,000, and a normal profit margin of 20 percent.

Property, Plant, and Equipment

The company acquired a building at the beginning of 2019 at a cost of $2,750,000. The building

has an estimated useful life of 25 years, an estimated residual value of $250,000, and is being

depreciated on a straight-line basis. At the beginning of 2020, the building was appraised and

determined to have a fair value of $3,250,000. There is no change in estimated useful life or residual

value. In a switch to IFRS, the company would use the reevaluation model in IAS 16 to determine

the carrying value of property, plant, and equipment subsequent to acquisition.

Intangible Assets

As part of a business combination in 2017, the company acquired a brand with a fair value of

$40,000. The brand is classified as an intangible asset with an indefinite life. At year-end 2020, the

brand is determined to have a selling price of $35,000 with zero cost to sell. Expected future cash

flows from continued use of the brand are $42,000 and the present value of the expected future cash

flows is $34,000.

Research and Development Costs

The company incurred research and development costs of $200,000 in 2020. Of this amount, 40

percent related to development activities subsequent to the point at which criteria had been met

indicating that an intangible asset existed. As of the end of the 2020, development of the new

product had not been completed.

3

Sale-and-Leaseback

In January 2018, the company realized a gain of the sale-and-leaseback of an office building in the

amount of $150,000. The lease is accounted for as an operating lease, and the term of the lease is

five years.

Required

a) Prepare a reconciliation schedule to convert 2020 income, and December 31, 2020, stockholders’

equity from a U.S. GAAP basis to IFRS. Ignore income taxes. Prepare a note to explain each

adjustment made in the reconciliation schedule.

b) Discuss each relevant accounting standards with references to journal article(s) by using

disclosure examples of companies.

Related questions

Case 10-1

Swisscom AG, the principal provider of telecommunications inSwitzerland, prepares consolidated financial statements inaccordance with IFRS. Until 2007, Swisscom also reconciled its netincome and stockholdersâ equity to US GAAP. Swisscom consolidatedfinancial statements from a recent annual report are presented intheir original format in Column 1 of the following worksheet. Note27, Differences between IFRS and GAAP, which includes Swisscomâs USGAAP reconciliation, also is provided.

Required

Use the information in Note 27 to restate Swisscomâsconsolidated financial statements in accordance with US GAAP. Beginby constructing debit/credit entries for each reconciliation item,and then post these entries to columns 2 and 3 in the worksheetsprovided.

Calculate each of the following ratios under both IFRS and GAAPand determine the percentage differences between them, using IFRSratios as the base:

Net income/net revenue

Operating income/net revenues

Operating income/total assets

Net income/shareholdersâ equity

Operating income/total shareholdersâ equity

Current assets/current liabilities

Total liabilities/total shareholdersâ equity

Which of these ratios is most (least) affected by the accountingstandards used?

| Worksheet for theRestatement of Swisscom's Financial Statements from IFRS to USGAAP | ||||

| Reconciling | Adjustment | |||

| IFRS | DR | CR | US GAAP | |

| Consolidated Statement of Operations | ||||

| Net revenue | 9,842 | |||

| Capitalized cost and changes ininventory | 277 | |||

| Total | 10,119 | |||

| Goods and services purchased | 1,666 | |||

| Personnel expenses | 2,584 | |||

| Other operating expenses | 2,090 | |||

| Depreciation and amortization | 1,739 | |||

| Restructuring charges | 1,726 | |||

| Total operating expenses | 9,805 | |||

| Operating income | 314 | |||

| Interest expense | (428) | |||

| Financial income | 25 | |||

| Income(loss) before incometaxes and equity in net loss of affiliated companies | (89) | |||

| Income tax expense | 1 | |||

| Income(loss) before equity innet loss of affiliated companies | (90) | |||

| Equity in net loss of affiliatedcompanies | (325) | |||

| Net income(loss) | (415) | |||

| Consolidated Retained EarningsStatement | ||||

| Retained earnings, 1/1 | (151) | |||

| Net loss | (415) | |||

| Profit distribution declared | (1,282) | |||

| Conversion of loan payable to equity | 3,200 | |||

| Retained earnings, 12/31 | 1,352 | |||

| Assets | ||||

| Current assets | ||||

| Cash and equivalents | 256 | |||

| Securities available for sale | 51 | |||

| Trade accounts receivable | 2,052 | |||

| Inventories | 169 | |||

| Other current assets | 34 | |||

| Total current assets | 2,562 | |||

| Noncurrent assets | ||||

| Property, plant and equipment | 11,453 | |||

| Investments | 1,238 | |||

| Other noncurrent assets | 220 | |||

| Total noncurrent assets | 12,911 | |||

| Total assets | 15,473 | |||

| Current liabilities | ||||

| Short-term debt | 1,178 | |||

| Trade accounts payable | 889 | |||

| Accrued pension cost | 789 | |||

| Other current liabilities | 2,213 | |||

| Total current liabilities | 5,069 | |||

| Long-term liabilities | ||||

| Long-term debt | 6,200 | |||

| Finance lease obligation | 439 | |||

| Accrued pension cost | 1,488 | |||

| Accrued liabilities | 709 | |||

| Other long-term liabilities | 338 | |||

| Total long-term liabilities | 9,174 | |||

| Total liabilities | 14,243 | |||

| Shareholders' equity | ||||

| Retained earnings | 1,352 | |||

| Unrealized market valueadjustment on securities available for sale | 39 | |||

| Cumulative translation adjustment | (161) | |||

| Total shareholders' equity | 1,230 | |||

| Total liabilities and shareholders'equity | 15,473 | |||

27. Differences between IFRS and GAAP

The consolidated financial statements of Swisscom have beenprepared in accordance with IFRS, which differ in certain respectsfrom GAAP in the US. Application of US GAAP would have affected thebalance sheet and net income (loss) to the extent described below.A description of the material differences between IFRS and GAAP asthey relate to Swisscom are discussed in further detail below.

Reconciliation of net income (loss) from IFRS toGAAP

The following schedule illustrates the significant adjustmentsto reconcile net income (loss) in accordance with US GAAP to theamounts determined under IFRS, for the current year ended December31.

| (CHF in millions) | ||

| Net income (loss) according toIFRS | (415) | |

| US GAAP adjustments: | ||

| Capitalization of interest cost | 8 | |

| Restructuring charges | 205 | |

| Depreciation expense | -5 | |

| Capitalization of software | 182 | |

| Restructuring charges byaffiliates | 50 | |

| Net income according to GAAP | 25 | |

Reconciliation of shareholdersâ equity from IFRS toGAAP

The following is a reconciliation of the significant adjustmentsnecessary to reconcile shareholdersâ equity in accordance with USGAAP to the amounts determined under IFRS as at December 31 of thecurrent year.

| (CHF in millions) | ||

| Shareholders' equity accordingto IFRS | 1230 | |

| US GAAP adjustments: | ||

| Capitalization of interest cost | 54 | |

| Restructuring charges | 205 | |

| Depreciation expense | -5 | |

| Capitalization of software | 475 | |

| Restructuring charges byaffiliates | 50 | |

| Shareholders' equity accordingto GAAP | 2009 | |

Capitalization of interest cost

Swisscom expenses all interest costs as incurred. US GAAPrequires interest costs incurred during the construction ofproperty, plant and equipment to be capitalized. Under US GAAP,Swisscom would have capitalized CHF 13 million and amortized CHF 5million for the current year.

Restructuring charges

During the current year, Swisscom recognized under IFRSrestructuring charges totaling CHF 1726 million. The followingschedule illustrates adjustments necessary to reconcile thesecharges to amounts determined under US GAAP.

| Restructuringcharges in accordance with IFRS | ||

| Personnel restructuringcharges | 1326 | |

| Write-down of long-livedassets | 316 | |

| Misc. restructuring charges | 84 | |

| Total in accordance with IFRS | 1726 | |

| Adjustments to restructuringcharges to accord with GAAP | (205) | |

| Restructuring charges inaccordance with GAAP | 1521 | |

Reconciliation of restructuring charges | ||

| Restructuring chargesaccording to US GAAP consist of the following: | ||

| Personnel restructuringcharges | 1228 | |

| Write-down of long-livedassets | 209 | |

| Misc. restructuring charges | 84 | |

| Restructuring charges inaccordance with GAAP | 1521 | |

Depreciation expense

Due to the difference in carrying value of long-lived assetsafter write-downs describe in (b), there is a difference in theamount of depreciation expense taken under IFRS and GAAP. Anadjustment is made for the current year to record an additional CHF5 million of depreciation under US GAAP.

Capitalization of software

Swisscom has expensed software costs as incurred. For US GAAPpurposes, external consultant costs incurred I the development ofsoftware for internal use has been capitalized. These costs arebeing amortized over a 3 year period. The capitalization ofsoftware costs accords with common practice in the UStelecommunications industry.

Swisscom has capitalized, as disclosed in the reconciliation ofnet income (loss) and shareholdersâ equity to US GAAP, CHF 220million and amortized CHF 37 million in the previous year andcapitalized CHF 370 million and amortized CHF 188 million in thecurrent year.

Restructuring charges of affiliates

During the current year, Swisscomâs share of personnel and otherrestructuring charges recorded by affiliates amounted to CHF 50million. These restructuring charges do not meet all therecognition criteria contained in EITF 94-3 and therefore cannot beexpensed in the current year, under US GAAP.