BUSN1001 Study Guide - Final Guide: Bank Reconciliation, Petty Cash, Bank Statement

Working Capital Management

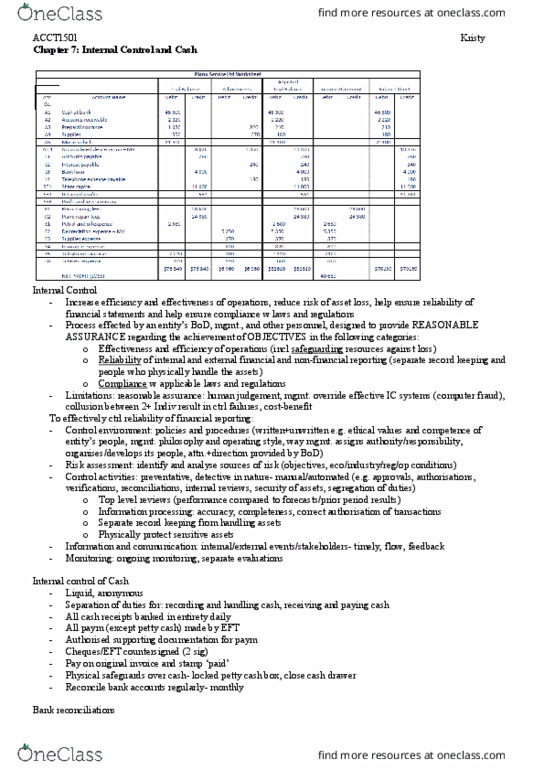

Cash Control Procedures

• Internal control - all the policies and procedures that are used by management to

ensure the effectiveness and efficiency of operations as well as the reliability of

financial reporting and compliance with laws and regulations.

• Internal control activities - includes approvals, authorisations, verifications,

reconciliations, review of operating performance, security of assets, and segregations

of duties.

Payment perspective:

• Separation of duties

o Separation of recording and handling cash.

o Separation of receiving and paying cash.

• Approval and authorisation

o Payments made after document has been authorised.

o All paying (except petty cash) made by cheque.

o Cheques signed by two staff who are independent of invoice approval.

Receiving money:

• Security of assets

o All cash receipts banked intact daily.

o Physical safeguards over cash.

• Reconciliations

o Reconcile bank accounts regularly.

Bank Reconciliation

• Reconciliations - explaining differences between two sets of records.

• Steps:

1. Reconciling process

2. Bank reconciliation statement

o What are added to a bank reconciliation statement?

o Recorded in the company's book but not yet in the bank statement.

o Timing differences that will self-correct.

3. Journal entries

o What are recorded in the company book?

o The records in the bank statement but not yet in the company book.

o Errors to be corrected.

Managing Inventory

• There are two methods of keeping records of inventory transactions:

1. Perpetual – continuously updates the inventory for each purchase and sale.

2. Periodic – does not maintain a running balance of inventory but counts inventory

at end of period.

o COGS (deduced) = beginning bal. (count) + purchases (records) - ending bal.

(count).

• Cash flow assumptions:

o FIFO - assumes that first in are first sold.

o In times of rising prices, this method results in the highest inventory asset value

and the lowest COGS, giving the highest gross profit.

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Internal control - all the policies and procedures that are used by management to ensure the effectiveness and efficiency of operations as well as the reliability of financial reporting and compliance with laws and regulations. Internal control activities - includes approvals, authorisations, verifications, reconciliations, review of operating performance, security of assets, and segregations of duties. Receiving money: security of assets, all cash receipts banked intact daily, physical safeguards over cash, reconciliations, reconcile bank accounts regularly. In times of rising prices, this method results in the highest inventory asset value and the lowest cogs, giving the highest gross profit: weighted average - calculate every price after every purchase. If a perceptual system is used, the average cost will change each time there is a purchase of inventory. If the periodic system is used, inventory items will be valued at an annual weighted average.