BUSN1001 Study Guide - Final Guide: General Ledger, Trial Balance, Financial Statement

Recording Business Transactions Underlying the Reports

Accounting Terms

• Journal - provides a complete record of all transactions in chronological order.

• Ledgers - books that have a separate page or account code for each individual account

referred to in the books of original entry/a collection of all individual accounts.

• Posting - transferring the amounts from the journal to the accounts in the ledger.

• T-Account - an individual account within the general ledger.

• Basic format of a T- account:

• Rules of debit and credit: Debits = Credits

Accounting Procedures

• Transaction (buy equipment with cash) + Source Documents (purchase invoice, tax

invoice) → Journal (increase equipment, decrease cash) → Ledger (record in equip and

cash account) → Trial Balance (list acc. Balances) → financial statements.

Step 1 & 2:

Record

Transactions

• Identify and analyse a transaction:

- Not all events are accounting transactions.

- Criteria: exchange between the company and an external

party.

• For transactions, get the source documents.

• Determine the accounts affected - at least two accounts.

• Apply debit and credit rules.

• Record transaction in journal: date and description, name of

account affected & amount.

Step 3: Post

to Ledgers

• Ledgers = collection of accounts.

• Separate account for each item of asset, liability, owner's equity,

revenue and expense.

• Record of increases and decreases.

• Post to appropriate account in the ledger according to journal entry.

Step 4: The

Trial Balance

• Because the general ledger contains all the accounts, all of which

come from balanced journal entries, it must balance.

• Because errors might have been made a trial balance is done.

• All the balances of each accounts in the ledger are listed on the trial

balance.

• Provides a check on the accuracy of the double entry system (i.e.

debits = credits).

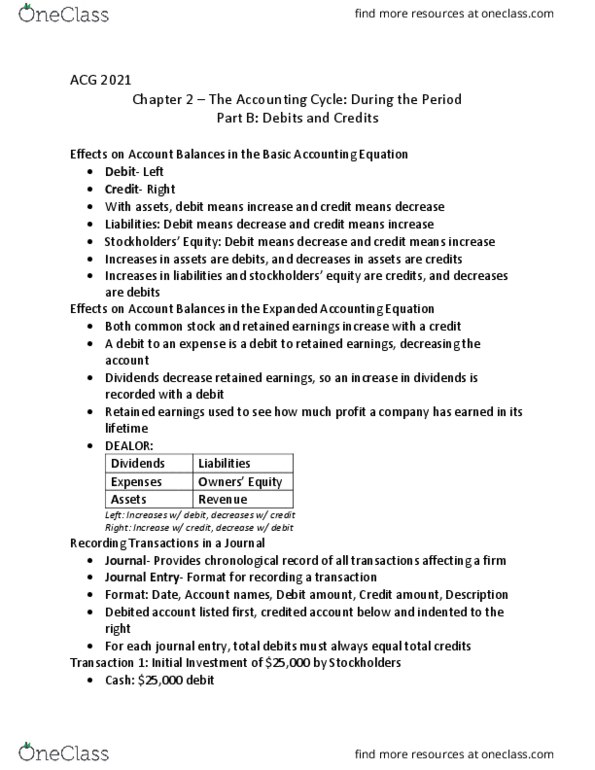

Summary of Debit/Credit Rules

Step 5:

Adjusting

Entries

• At the end of each accounting period, it is necessary to adjust the

revenue and expense accounts to reflect expenses incurred but not

yet paid, revenues earned but not yet received, cash received from

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Journal - provides a complete record of all transactions in chronological order. Accounting procedures: transaction (buy equipment with cash) + source documents (purchase invoice, tax invoice) journal (increase equipment, decrease cash) ledger (record in equip and cash account) trial balance (list acc. Step 3: post to ledgers account affected & amount. Ledgers = collection of accounts: separate account for each item of asset, liability, owner"s equity, Accrual basis - transactions recorded when revenues earned, when expenses incurred, regardless of when cash is received or paid. Provides more complete information useful to decision- makers. Cash basis - transactions recorded when cash received, when cash paid, regardless of when revenue earned or expenses incurred. Need for adjusting entries: accounts need to be adjusted at year end to correctly recognise revenue and expenses, and bring related asset and liability accounts to correct balances. Postponement of the recognition of expense already paid or revenue already received.