ACC210 Study Guide - Final Guide: Variable Cost, Accounts Payable, Fixed Cost

Management Accounting Study

Costing methods:

Direct material – consumed in the manufacturing process of the product. Variable Cost

Direct Labour – wages and labour hrs

Manufacturing Over Heads – everything in the cost but material and labour. Examples include,

depreciation, rent, equipment, everything that happens in the factory i.e. electricity, oil, indirect

factory supplies. Indirect material and labour and OH

BOM: Bill of materials useful for standard costing system

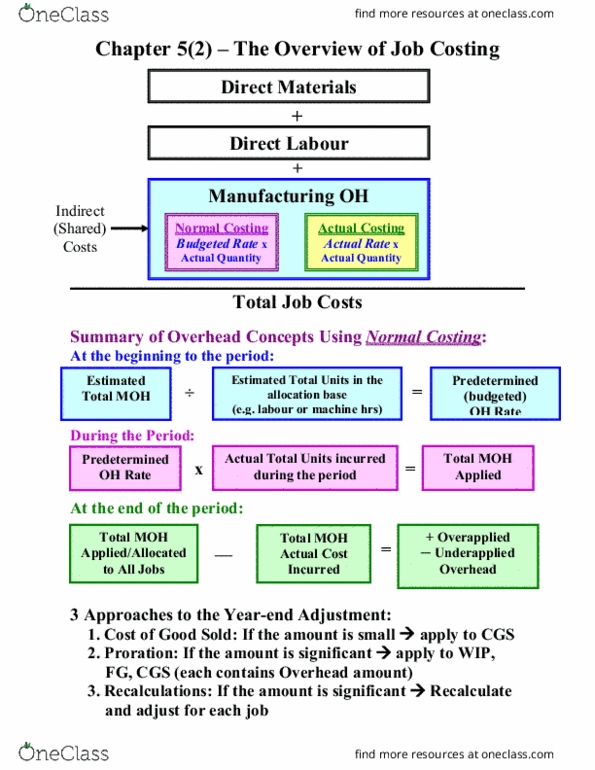

Job cost sheet: includes the direct materials, direct labour and overhead costs.

Over Heads – have to allocate as its impossible to direct it at one single job or product. Assigned to

direct labour hrs or machine hrs.

Estimated total manufacturing OH costs / estimated total units base(activity) = predetermined OH

rate (+ variable OH rate per if there)

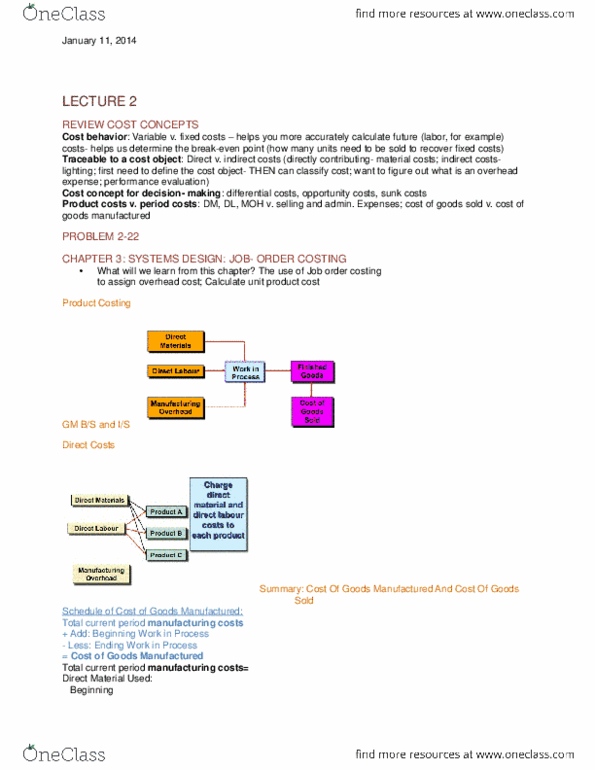

Job Costing used in manufacturing where many different products or batches are done in each

period which are different i.e. furniture manufacturing, job cost sheet is the key document and unit

costs are determined by the jobs. This is also undertaken in service offices such as accountants and

lawyers.

Process Costing single homogenous products running long periods of time i.e. brick or cement

factory . Costs are accumulated by the department.

1. Analyse the physical flow of units

2. Calculate the equivalent units

3. Calculate unit costs (FIFO and Average method)

4. Analyse total costs

physical flow equivalent units transfers out + ending inventory

Equivalent units = Number of physical units × Percentage of completion.

Operation Costing Operation costing is a mix of job costing and process costing, and is used in

either of the following situations:

A product initially uses different raw materials, and is then finished using a common process

that is the same for a group of products; or

A product initially has identical processing for a group of products, and is then finished using

more product-specific procedures.

Joint Costing Joint cost is the manufacturing cost incurred on a joint production process which

takes common inputs but simultaneously produces multiple products called joint-products

relative sales method sale value of product/sales value of total production x total joint costs

NetRelisableValue (products need further processing)= estimates sales values – estimated cost to

further process and sell

Period costs costs other than product costs excluding OVERHEAD

by-products products incidentally made in the production of making something else

Subsidary cost ledger:

find more resources at oneclass.com

find more resources at oneclass.com

DR and CR accounts

Purchase of direct materials – direct/indirect

Raw Materials DR

Acc Payable CR

Use of raw materials/return

When direct materials are issued to production: Dr WIP; Cr Materials Control.

Reverse when materials are returned to store: Dr Materials Control; Cr WIP.

Use of in-direct materials

Manufacturing OverHead DR

Manufacturing Supplies inventory (raw materials)CR

Labour hours/cost (Direct)

Charging direct labour to jobs -

Work In Process inventory (WIP) DR

Manufacturing Overhead DR

Wages Payable CR

(Indirect)

Manufacturing Overhead DR

Wages Payable CR

Manufacturing Overhead Costs

Dr Manufacturing Over Head

Cr Accounts payable

Cost of Goods Manufactured

Dr Finished Goods

Cr Work in Process

Cost of Goods Sold

Dr COGS

Cr Finished goods

The application of manufacturing OH – clearing account(control account) – reconciliation between

the actual over head and the over head allocated

find more resources at oneclass.com

find more resources at oneclass.com

Product Costing:

Product costs – costs assigned to goods

period costs – costs identified at the period they are incurred eg. Electricity used for variable OH

costs in variable costing

Variable costs – costs the vary in relation to changes in activity. Referred to in dollar amounts

(marginal)

Fixed costs – costs not affected by changed in activity eg. rent/level of activity. decrease with

increased levels of production

direct and indirect – must first relate to a segment the business i.e. product line, division. Direct cost

is traced to a specific product or segment. Indirect is a cost incurred and must be allocated in order

to be assigned to a product or department

Differential cost/marginal cost – adding one more unit to a product or price = increase. Or the

decrease due to a manufacturing/product/price

Prime Cost = Direct Materials + Direct Labour

Conversion Cost = Direct Labour + Manufacturing Overhead

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Direct material consumed in the manufacturing process of the product. Manufacturing over heads everything in the cost but material and labour. Examples include, depreciation, rent, equipment, everything that happens in the factory i. e. electricity, oil, indirect factory supplies. Bom: bill of materials useful for standard costing system. Job cost sheet: includes the direct materials, direct labour and overhead costs. Over heads have to allocate as its impossible to direct it at one single job or product. Assigned to direct labour hrs or machine hrs. Estimated total manufacturing oh costs / estimated total units base(activity) = predetermined oh rate (+ variable oh rate per if there) Job costing used in manufacturing where many different products or batches are done in each period which are different i. e. furniture manufacturing, job cost sheet is the key document and unit costs are determined by the jobs. This is also undertaken in service offices such as accountants and lawyers.