ACCG101 Study Guide - Final Guide: Cost Driver, Life Insurance, Book Value

24 Jul 2018

School

Department

Course

Professor

ACCG101 – ACCOUNTING 1B

Week 1 – Revision

The Accounting Cycle

1. Transaction analysis

2. Journalise transactions

3. Post to ledger accounts

4. Prepare trial balance

5. Journalise & post adjusting entries

6. Prepare adjusted trial balance

7. Prepare financial statements

8. Journalise & post closing entries

9. Prepare post-closing trial balance

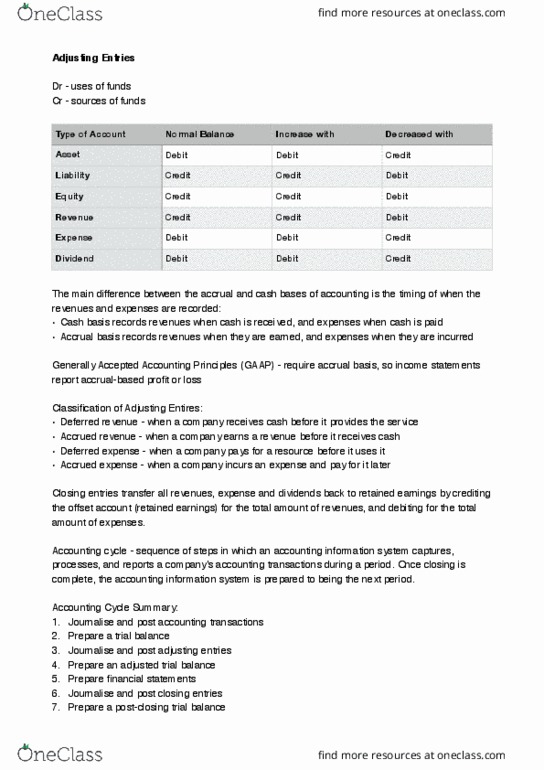

The Accounting Equation

• Assets = Liabilities – Owners Equity

• Debit is the normal balance and to increase - expense, asset

• Credit is the normal balance and to increase – income, liability, equity

Bad Debts

• There are two methods to record bad debts:

1. Direct Write-Off Method:

• Used by some small companies – bad debts expensed with no allowance for doubtful debts.

2. Allowance Method:

• Most widely used method - estimate bad debts first, then determine the actual amount or account is bad

• AASB 137 Provision, Contingent Liabilities and Contingent Assets.

• Adjustment Entry: To estimate a general amount as uncollectable through the bad debts expense. Use ‘percentage of net

credit sales method’. Percentage will be specified in question.

• Write Off: Then, write off the actual ‘account receivable’ account as a bad debt (real amount not estimation). Note that,

both the control and subsidiary accounts must be credited.

• Recover Bad Debt: Must establish part of the account receivable previously written off as bad and collect cash. Note

that, recovery is treated as revenue, must update subsidiary ledger and record in cash receipt journal.

Jun 30 DR Bad Debts Expense $6000

CR Accounts Receivable $6000

(Bad debts expensed)

Jun 30 DR Bad Debts Expense $19600

CR Allowance for Doubtful Debts $19600

(Estimated bad debts expense)

Jun 30 DR Allowance for Doubtful Debts $1562

CR Accounts Receivable $1562

(Real bad debts expense)

Jun 30 DR Accounts Receivable $781

CR Bad Debts Recovered $781

(Re-establish part of the account receivable written off as bad)

Jun 30 DR Cash at Banks $781

CR Accounts Receivable $781

(Cash collection)

• You may be given an ‘ageing schedule’ from which you must calculate the estimated doubtful debts.

• The total of the estimated doubtful debts must then be recorded in the general ledger as ‘balance c/d’. From this

you can calculate the ‘Bad Debt Expense’ to balance the ledger.

• Note that everything in black in this example was given.

• This would be recorded in the general journal as the following:

• And recorded in the balance sheet as the following:

Adjusting Entries

Deferrals (Prepayments) – Prepaid Expenses

• Cost paid in advance, but not yet consumed.

• One method for depreciation expense.

• Two methods for prepaid expenses such as, prepaid rent, prepaid insurance, office supplies.

• Method 1: Initially recorded as an asset. Unused to used.

Ageing Accounts

Amount in Accounts

Percentage

Estimated Doubtful Debts

Accounts Not Due

$145,500

0.1%

$145.50

1 – 30 Days

$43,000

2.0%

$860.00

31 – 60 Days

$28,000

5.0%

$1400.00

61 – 150 Days

$14,000

25%

$3500.00

151 Days +

$5,000

55%

$2700.00

$235,500

$8655.50

General Ledger

Allowance for Doubtful Debts.

30/5 Accounts Receivable Written Off $7,815.00

30/5 Balance c/d $8,655.50

$16,470.50

1/5 Balance b/d $7,500.00

30/5 Bad Debt Expense $8,970.50

$16,470.50

30/5 DR Bad Debt Expense $8970.50

CR Allowance for Doubtful Debts $8970.50

Heather Ltd.

Balance Sheet (Partial)

As at 30 June 2013

ASSETS

Accounts Receivable $235,000.00

Less: Allowance for doubtful debts $8970.50

1 Jun DR Mercedes Car (Asset) $92,700

CR Cash at Bank $92,700

(Purchased Mercedes car in cash)

30 Jun DR Depreciation Expense $1,636.25

CR Accumulated Depreciation $1,636.25

(Adjusting entry to record depreciation – 19,635 x 1/12)

1 Jun DR Prepaid Insurance (Asset) $10,800

CR Cash at Bank $10,800

(To record the purchase of insurance policy)

30 Jun DR Insurance Expense $900

CR Prepaid Insurance $900

(Adjusting entry for expired portion – 10,800 x 1/12)

$16,470.50

– $7,500 =

$8,970.50

• Method 2: Initially recorded as an expense. Used to unused.

Deferrals (Prepayments) – Unearned Revenue

• Cash received in advanced, but not yet earned.

• Two methods for unearned revenue such as, unearned service revenue, subscription revenue, rent received in advanced.

• Method 1: Initially recorded as a liability. (Preferred method)

• Method 2: Initially recorded as a revenue.

Accruals (Unrecorded) – Accrued Expenses

• Unrecorded expenses that have been incurred, but payment has not yet been made or recorded.

• Eg. Wages and salaries expense, utilities expense, and interest expense.

Accruals (Unrecorded) – Accrued Revenue

• Unrecorded revenues, revenue earned but not yet received.

• Eg. Interest revenue, rent revenue and commission revenue.

Closing Entries

2. Close all income accounts:

1 Jun DR Insurance Expense (Expense) $10,800

CR Cash at Bank $10,800

(To record the purchase of insurance policy)

30 Jun DR Prepaid Insurance $9,900

CR Insurance Expense $9,900

(Adjusting entry for unexpired portion – 10,800 x 11/12)

1 Jun DR Cash $240

CR Unearned Revenue (Liability) $240

(Collect revenue in advance)

30 Jun DR Unearned Revenue $20

CR Revenue $20

(Adjusting entry for earned portion – 240 x 1/12)

1 Jun DR Cash at Bank $240

CR Revenue (Revenue) $240

(Collect revenue in advance)

30 Jun DR Revenue $220

CR Unearned Revenue $220

(Adjusting entry for unearned portion – 240 x 11/12)

30 Jun DR Salaries Expense (Expense) $1,990

CR Salaries Payable (Liability) $1,990

(Adjusting entry for salaries earned, but not yet paid)

30 Jun DR Interest Receivable (Asset) $79

CR Interest Revenue (Revenue) $79

(Adjusting entry to record interest earned, but not yet received)

Jun 30 DR Each Individual Income Account

CR P&L Summary

(To close income accounts)