ECON1101 Study Guide - Final Guide: Sunk Costs, Demand Curve, Marginal Cost

ECON1101 Kristy

Chapter 1

- Opportunity cost

o Value of the next best alternative (implicit value + explicit cost)

o OC = ∆/∆

o Absolute advantage: can carry on activity w less resources than another agent

- Your first economic model

o 2 activities, 2 individuals, no transaction costs/barriers to entry

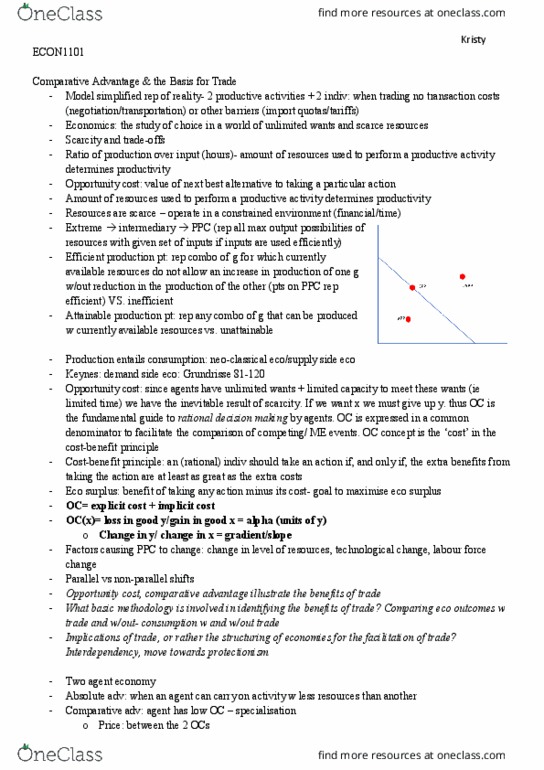

- The Production Possibilities Curve

o Graphical representation of all possible maximum output combinations, given a set

of inputs used efficiently

o Efficient, inefficient, attainable, unattainable

o Productivity, scarce resources

- The benefits of specialisation and trade

o Comparative advantage- lower OC (greater gains when OC differs more)

o Principle of comparative advantage: everyone is better off if each agent specialises in

activities for which they have a comparative advantage

- The economy wide PPC

o Low hanging fruit principle (increasing opportunity cost): in the process of increasing

the production of any good, one first employs those resources with the lowest

opportunity cost and only once they are exhausted turn to resources with higher

cost

o Increase in infrastructure/capital, increase in population/labour, advancements in

knowledge and technology

- Trading between 2 economies: International trade

o Consumption possibility curve: all possible combinations of goods feasibly consumed

when open to international trade (parallel tangent) (national income/good 1,2 price)

▪ Closed economy: CPC = PPC (welfare)

▪ Open economy: CPC > PPC

o Trading price is between the 2 OCs

- Classic critiques of the model

o No psychological costs, no transaction costs/barriers to trade, sunk cost, no

preference changes

Chapter 2

- How an individual decides what and how much produce

- Perfectly competitive market

o Homogenous goods

o Free entry and exit

o Full information

o Goods are rival and excludable

o No externalities

o Producers/consumers are price takers

- The importance of thinking in terms of marginal costs and benefits

o Marginal benefit: extra benefit accrued for producing the additional unit

o Marginal cost: extra cost associated with producing that unit (OC)

o Cost-benefit principle: atio should e take if MB ≥ MC (eco surplus: MB – MC)

- Deriving the supply curve of a firm

find more resources at oneclass.com

find more resources at oneclass.com

ECON1101 Kristy

o Law of supply: tendency of a producer to offer more of the good when the price rises

(supply curve is upward sloping)

o Horizontal/vertical interpretation

o Producer reservation price: minimum amount of money producer is willing to accept

to produce that good

o Sunk cost: cost once paid cannot be recovered (does not affect OC)

o Fixed cost: cost associated w factor of production does not vary with quantity

produced (SR onto 1 is fixed)

o Variable cost: cost associated w it tends to vary w the number of units produced (LR

when all factors of production are variable)

o TC= FC + VC, AVC= VC/Q, ATC= TC/Q, MC= ∆TC/∆Q (graphs)

o Profit= TR – TC (price of the good)

o Short run shut down condition: profit < -FC (P below min AVC)

▪ Supply curve = MC curve above AVC

o Long run shut down condition: profit < 0 (exit industry profit = 0) (P below min ATC)

▪ Supply curve = MC curve above ATC

o Shift MC curve: technology (productivity), (variable) input prices, expectations (fut

pries/dead, ∆ i prie/dead of other goods, # of suppliers

- Price elasticity of supply

o Percentage change in quantity supplied resulting from a small change in price

(responsiveness of supply to changes in P)

o ∆Q/Q ÷ ∆P/P = P/Q* 1/m

o e>1 (elastic), e = 1 (unit elastic), e<1 (inelastic)

o determinants: availability of raw materials, factors mobility, inventories/excess

capacity (increase variable factors of production), time horizon

Chapter 3

- Utility: the basic model of consumer choice

o Measures the satisfaction an individual derives from consuming a good (utils/hr)

o Decreasing marginal utility: utility from consuming an extra unit of a given good

decreases with the number of units previously consumed

- Deriving the individual demand curve

o Substitution effect: captures the change in the quantity demanded following a

change in its relative price (-ve + stronger than Y fx)

o Income effect: captures the change in the quantity demanded following a reduction

i the osuer’s purhasig poer (+ve/-ve)

o Law of demand, horizontal/vertical interpretation, D curve = MB curve for consumer

o Consumer reservation price: maximum amount of money an individual is willing to

pay for a certain g/s

- Properties of goods: normal vs. inferior (giffen P increase, Q demanded increase),

complements vs. substitutes

o Substitutes: increase in the P of one causes an increase in the demand of the other

o Complements: increase in the P of one causes a decrease in the demand of the other

- Price elasticity of demand

o Percentage change in Q demanded resulting from a small change in price,

responsiveness of demand to changes in P (P/Q * 1/m) (|-ve|) elastic >1, unit = 1,

inelastic <1

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Opportunity cost: value of the next best alternative (implicit value + explicit cost, oc(cid:894)(cid:454)(cid:895) = (cid:455)/ (cid:454, absolute advantage: can carry on activity w less resources than another agent. Your first economic model: 2 activities, 2 individuals, no transaction costs/barriers to entry. The production possibilities curve: graphical representation of all possible maximum output combinations, given a set of inputs used efficiently, efficient, inefficient, attainable, unattainable, productivity, scarce resources. The benefits of specialisation and trade: comparative advantage- lower oc (greater gains when oc differs more, principle of comparative advantage: everyone is better off if each agent specialises in activities for which they have a comparative advantage. Increase in infrastructure/capital, increase in population/labour, advancements in knowledge and technology. Classic critiques of the model: no psychological costs, no transaction costs/barriers to trade, sunk cost, no preference changes. How an individual decides what and how much produce.