RECL 3P70 Study Guide - Final Guide: Economic Impact Analysis, Lemonade, Yield Management

Get access

Related Documents

Related Questions

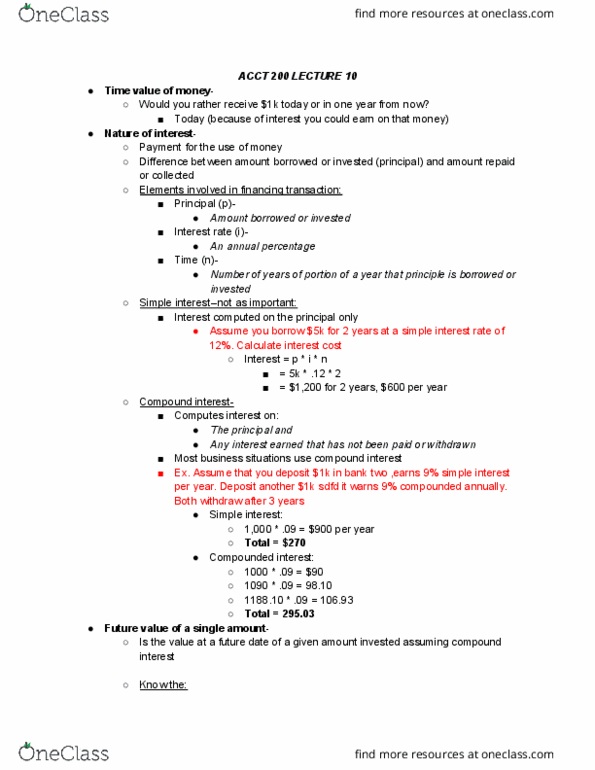

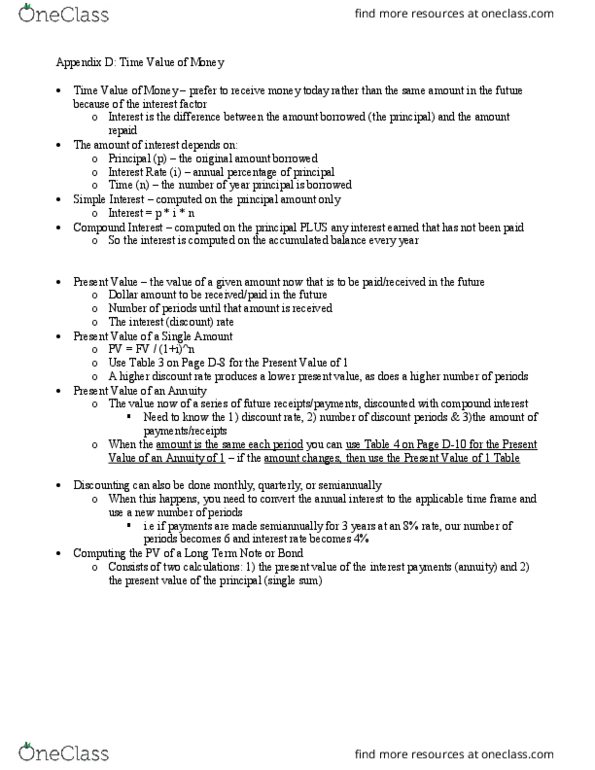

Assume that you have $1,000 to invest, so insert 1000 as your Present Value in the following table. Assume that you want to invest your money for 5 years (insert 5 for Number of Periods). Assume an annual interest rate of 3.00% (insert 3 for Interest Rate per Period). The table will determine the Future Value of your investment. If you input the numbers correctly, your Future Value is computed to be $1.159, which is what your investment will be worth in 5 years. Now revise the input to reflect your actual savings and the prevailing interest rate so that you can see how your savings will grow in 5 years. Even if you have no savings now, you can at least see how the interest rate affects the future value of savings by revising your input in the Interest Rate per Period and then observing the change in the Future Value. Future Value of a Present Amount Present Value $1,500 Number of Periods 5 Interest Rate per Period 3.0% FV = PV*(1+R)^N Future Value $1,739 2. Assume that you have $1,000 to invest at the end of each of the next 5 years, so insert 1000 as your Payment per Period in the following table. Assume that you want to invest your money for 5 years (insert 5 for Number of Periods). Assume an annual interest rate of 3.00% (insert 3 for Interest Rate per Period). The following table will determine the Future Value of your investment. If you input the numbers correctly, your Future Value is computed to be $5,309, which is what your investments will be worth in 5 years. Now revise the input to reflect your actual expected savings per year over the next 5 years, and existing interest rate quotations so that you can estimate how your savings will grow in 5 years. You can now revise the table to fit your own desired level of saving. Future Value of an Annuity Payment per Period $1,500 Number of Periods 5 Interest Rate per Period 3.0% FV = FV(R, N, PMT, (PV), beginning=1, end=0) Future Value $7,964 3. Assume that you want to deposit savings that will be worth $10,000 in 5 years, so insert 10000 as the Future Amount and 5 as the Number of Periods in the following table. Assume an annual interest rate of 3.00% (insert 3 for Interest Rate per Period). The following table will determine the Present Value, which represents the amount of savings you need today that would accumulate to be worth $10,000 in 5 years. If you input the numbers correctly, the Present Value is estimated in the table to be $8,606. Now revise the input to reflect your own desired savings amount in 5 years so that you can estimate how much you need now to achieve your savings goal in 5 years. Present Value of a Future Amount Future Amount $20,000 Number of Periods 5 Interest Rate per Period 3.0% PV = FV / (1+R)^N Present Value $17,252 4. Assume that you want to deposit savings at the end of each of the next 5 years so that you will have $10,000 in 5 years. So insert 10000 as the Future Amount and 5 for Number of Periods. Assume an annual interest rate of 3.00% (insert 3 for Interest Rate per Period). The following table will determine the Annual Payment, which represents the annual payments that will accumulate to your future desired investment. If you input the numbers correctly, your Annual Payment is computed to be $1,884. Now revise the input to reflect your own desired savings amount in 5 years so that you can estimate how much you need to save per year to achieve your savings goal in 5 years. Compute Payment Needed to Achieve Future Amount Future Amount $20,000.00 Number of Periods 5.00 Interest Rate per Period 3.00% PMT = FV / [FV(R, N, -1)] Annual Payment $3,767

Decisions 1. Using the above formulas and understanding of the impact of interest rates and time on your savings, report on how much you must save per year and the return you must earn to meet your savings goal for graduation, and your savings goal in your first three years of post-graduation life.

I need a report on how much to save per year and the return to earn to meet savings goal for graduation, and savings goal in the first three years of post graduation. Can you please use the numbers above that are already calculated in the formula. I have had an answer on this below. I don't understand why the periods don't stay the same for 5 years. The annuity is 7964 I took that divided b y 60 = 132.7 per month and multiplied it by 12 for a year and got 1592.4. Is that the savings for the answer to saving for a year. IF not I need help figuring out the calculation for the return to meet after gradutaion and the next three years post graduation.

| Goal 1 | Savings Goal for graduation, FV | $ 20,000 | |||||

| Time till graduation (Number of periods) | 5 | ||||||

| Present value of savings | $ - | ||||||

| Expected interest rates | 3% | ||||||

| Savings needed per year, PMT | $3,767.09 | =PMT(3%,5,0,20000,) | |||||

| Goal 2 | Savings Goal for 1st year of post graduation, FV | $ 15,000 | |||||

| Time till post graduation year 1 (Number of periods) | 6 | ||||||

| Present value of savings | $ - | ||||||

| Expected interest rates | 3% | ||||||

| Savings needed per year, PMT | $2,318.96 | =PMT(3%,6,0,15000,) | |||||

| Goal 3 | Savings Goal for 2nd year of post graduation, FV | $ 15,300 | |||||

| Time till post graduation year 1 (Number of periods) | 7 | ||||||

| Present value of savings | $ - | ||||||

| Expected interest rates | 3% | ||||||

| Savings needed per year, PMT | $1,996.75 | =PMT(3%,7,0,15300,) | |||||

| Goal 4 | Savings Goal for 3rd year of post graduation, FV | $ 15,606 | |||||

| Time till post graduation year 1 (Number of periods) | 8 | ||||||

| Present value of savings | $ - | ||||||

| Expected interest rates | 3% | ||||||

| Savings needed per year, PMT | $1,754.99 | =PMT(3%,8,0,15606,) | |||||

Select the term that best fits each of the following definitions and descriptions.

| a. | Notes receivable |

| b. | Nontrade receivables |

| c. | Net realizable value |

| d. | Direct write-off method |

| e. | Interest-bearing note |

| f. | Maturity date |

| g. | Promissory note |

| h. | Factoring receivables |

| i. | Trade discount |

| j. | Present value |

| k. | Allowance method |

| l. | Sales discount |

| m. | Negotiable note |

| n. | Non-interest-bearing note |

| o. | Assignment of receivables |

| p. | Valuation date |

____ 21. Receivables that are evidenced by a formal written promise to pay a certain sum of money at a specified date.

____ 22. The date the principal amount of a note is due to be paid.

____ 23. The sum of future receipts or payments discounted to the present date at an appropriate rate of interest.

____ 24. A method of recognizing the estimated losses from uncollectible accounts as expenses during the period in which the sales occur.

____ 25. A note that is legally transferable by endorsement and delivery.

____ 26. Any receivable arising from transactions that are not directly associated with the normal operating activities of a business.

____ 27. A note written in the form where the face amount includes the interest charges.

____ 28. The borrowing of money with receivables pledged as security on the loan.

____ 29. A note written in the form where the maker promises to pay the face amount plus interest at a specified rate.

____ 30. An unconditional written promise to pay a certain sum of money at a specified time.