BUSI 2001 Quiz: Tutorial chapter 10- assets held for sale

24 Jan 2016

School

Department

Course

Professor

Document Summary

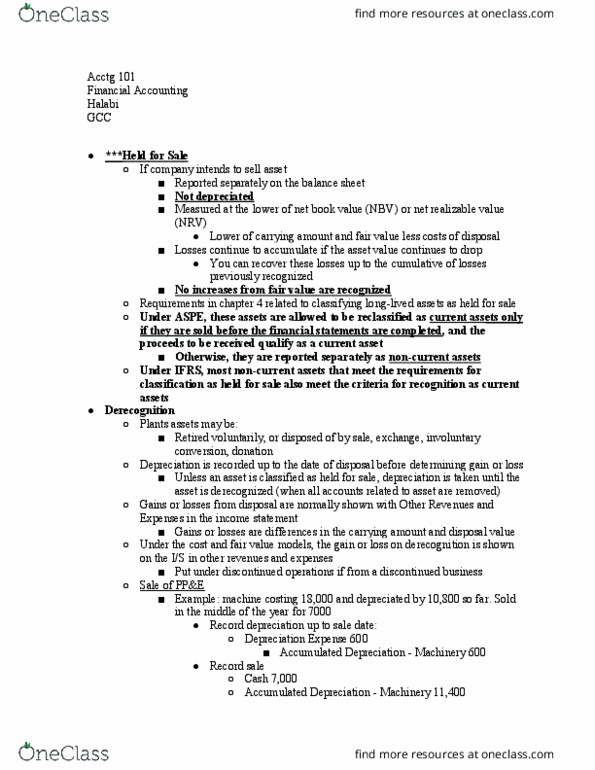

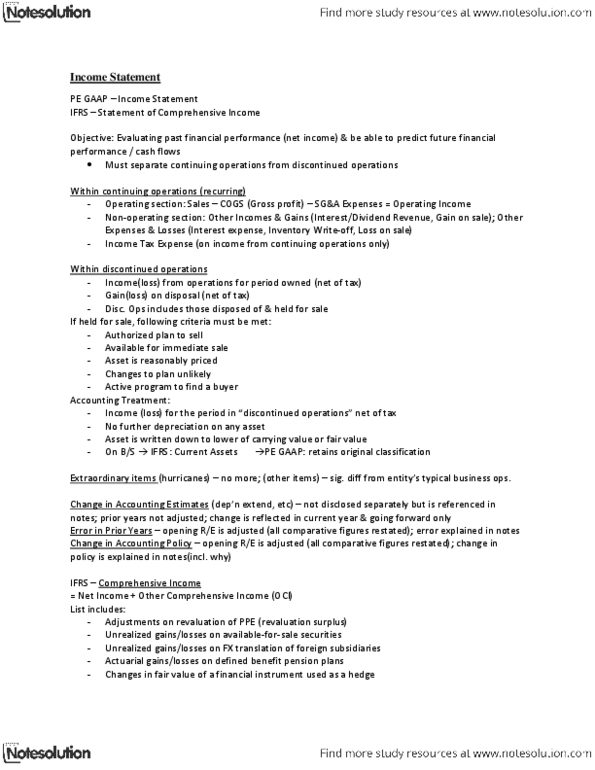

Chapter 10 assets held for sale and discontinued. Under ifrs 5, when an asset is classified as held for sale . The asset has to be reclassified at fair value less costs to sell: any impairment loss resulting from the reclassification of the asset should be reported net of tax in the income statement as: loss from discontinued operations. The asset is presented under current assets in the statement of financial position. The correct statements are: i and ii, iii and iv, ii and iii, i and iv, you have the following information about an asset reclassified as held for sale on december 31, On december 31, 2013, the fair value less costs to sell the asset is determined to be ,000. Determine the impairment gain, if any, the company can record on this asset. ,000: sh, public companies are not allowed to reverse impairment losses, ,000, ,000, ,000. 1: ,000, ,000, ,667, ,333, ,000, ,000, ,000, ,000.