COMM 305 Study Guide - Final Guide: Afterall, Cost Accounting, Finished Good

4 Dec 2018

School

Department

Course

Professor

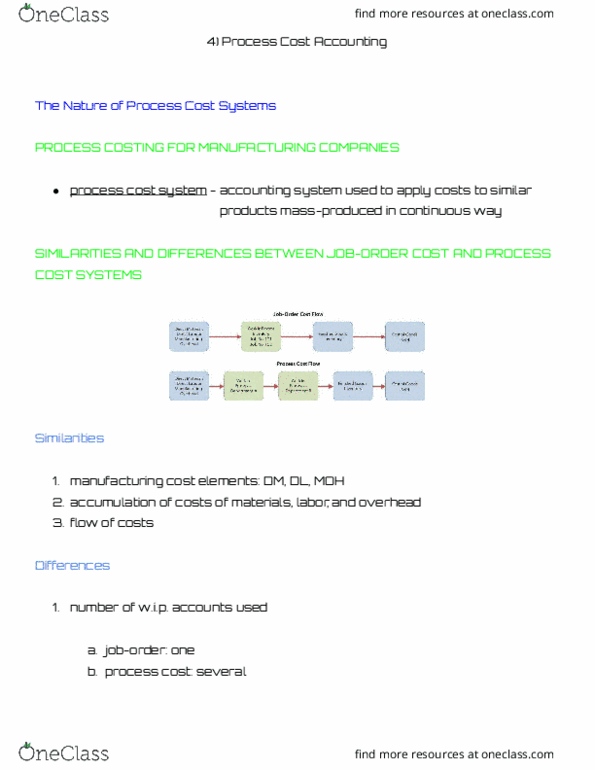

Process cost systems are used to apply costs to merchandise inventory.

True

False

In a process cost system, costs are tracked through individual jobs.

True

False

One Work in Process account is used in a process cost system.

True

False

The accumulation of the three manufacturing cost elements to Work in Process in a process cost

system differs significantly from how they are assigned in a job-order cost system.

True

False

A primary driver of overhead costs in continuous manufacturing operations is direct labour hours.

True

False

When goods are completed, the entry to record the transfer of the goods out of the last

department includes a debit to Cost of Goods Sold.

True

False

Equivalent units of production are used to determine the cost per unit of all products, whether

completed or not.

True

False

Equivalent units of production is an expression of the number of units that would have been

started and finished if all of the effort were directed at that purpose.

True

False

Beginning Work in Process is added to units completed and transferred out to determine

equivalent units of production under the weighted-average method.

True

False

Under the weighted-average method, the physical units in a department are the actual units in a

department regardless of the degree of any work performed.

True

False

Which of the following items is not a characteristic of a process cost system?

Once production begins, it continues until the finished product emerges.

The products produced are heterogeneous in nature.

The focus is on continually producing similar products.

When the finished product emerges, all units have exactly the same amount of materials,

labour, and overhead.

Which of the following is a characteristic of products that are mass-produced in a continuous

fashion?

They are grouped in batches.

They are produced all in one process.

Each batch of costs is accumulated in a separate cost of goods sold account.

The products are identical or very similar in nature.

Which one of the following is a difference between a job-order cost and a process cost system?

The manufacturing cost elements are different.

Costs are totalled at different points in the manufacturing process.

The costs flow through the accounts differently.

Three primary costs make up the costs of products in a job-order system, while only two

costs are used in process costing.

Which one of the following is a true statement about process cost systems?

In process cost systems, costs are accumulated and assigned.

A process cost system has one Work in Process account for each job.

In process cost systems, costs are summarized by batch.

Unit costs are ignored in process cost systems because they are identical.

A major difference between process costing and job-order costing is

Document Summary

Process cost systems are used to apply costs to merchandise inventory. In a process cost system, costs are tracked through individual jobs. One work in process account is used in a process cost system. The accumulation of the three manufacturing cost elements to work in process in a process cost system differs significantly from how they are assigned in a job-order cost system. A primary driver of overhead costs in continuous manufacturing operations is direct labour hours. When goods are completed, the entry to record the transfer of the goods out of the last department includes a debit to cost of goods sold. Equivalent units of production are used to determine the cost per unit of all products, whether completed or not. Equivalent units of production is an expression of the number of units that would have been started and finished if all of the effort were directed at that purpose.