ACCT 3380 Study Guide - Quiz Guide: Dividend Yield, Price–Earnings Ratio, Current Yield

Document Summary

Get access

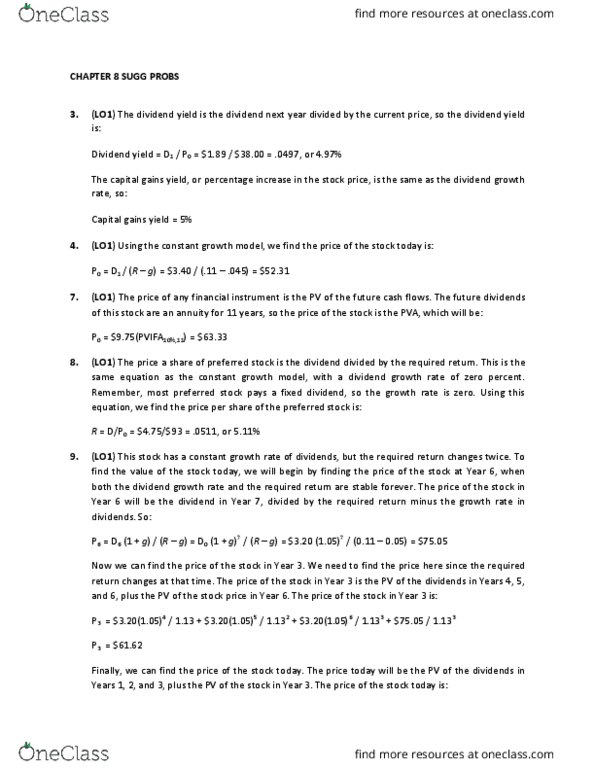

Related Documents

Related Questions

Estimating Share Value Using the DCF Model

Following are the income statement and balance sheet for TexasRoadhouse for the year ended December 29, 2015.

a. Assume the following forecasts for TXRHâs sales, NOPAT, andNOA for 2016 through 2019. Forecast the terminal period valuesassuming a 1% terminal period growth rate for all three modelinputs: Sales, NOPAT, and NOA.

Round your answers to the nearest dollar.

| Reported | Forecast Horizon | Terminal | ||||

|---|---|---|---|---|---|---|

| $ thousands | 2015 | 2016 | 2017 | 2018 | 2019 | Period |

| Sales | $1,807,368 | $2,069,436 | $2,369,504 | $2,547,217 | $2,738,258 | $Answer |

| NOPAT | 102,495 | 169,694 | 194,299 | 208,872 | 224,537 | $Answer |

| NOA | 662,502 | 758,591 | 868,587 | 933,731 | 1,003,760 | $Answer |

b. Estimate the value of a share of TXRH common stock using thediscounted cash flow (DCF) model as of December 29, 2015; assume adiscount rate (WACC) of 7%, common shares outstanding of 70,091thousand, net nonoperating obligations (NNO) of $(14,680) thousand,and noncontrolling interest (NCI) from the balance sheet of $7,520thousand. Note that NNO is negative because the companyâs cashexceeds its nonoperating liabilities.

Rounding instructions:

Use rounded answers for subsequent computations.

Round answers to the nearest whole number unless otherwisenoted.

Round discount factor to 5 decimal places and stock price pershare to two decimal places.

Do not use negative signs with any of your answers below.

| TXRH | Reported | Forecast Horizon | Terminal | |||

|---|---|---|---|---|---|---|

| $ thousands | 2015 | 2016 | 2017 | 2018 | 2019 | Period |

| Increase in NOA | $Answer | $Answer | $Answer | $Answer | $Answer | |

| FCFF (NOPAT - Increase in NOA) | Answer | Answer | Answer | Answer | Answer | |

| Discount factor [1 / (1 + rw)t ] | Answer | Answer | Answer | Answer | ||

| Present value of horizon FCFF | Answer | Answer | Answer | Answer | ||

| Cumulative PV of horizon FCFF | $Answer | |||||

| Present value of terminal FCFF | Answer | |||||

| Total firm value | Answer | |||||

| NNO | Answer | |||||

| NCI | Answer | |||||

| Firm equity value | $Answer | |||||

| Shares outstanding (thousands) | Answer | |||||

| Stock price per share | $Answer |

c. TXRH closed at $42.13 on February 26, 2016, the date the Form10-K was filed with the SEC. How does your valuation estimatecompare with this closing price?

Stock prices are a function of many factors. It is impossible tospeculate on the reasons for the difference.

Our stock price estimate is higher than the TXRH market price,indicating that we believe that the stock is slightly undervalued.Stock prices are a function of expected NOPAT and NOA, as well asthe WACC discount rate. Our higher stock price estimate might bedue to more optimistic forecasts or a lower discount rate comparedto other investors' and analysts' model assumptions.

Our stock price estimate is higher than the TXRH market price,indicating that we believe that the stock is slightly undervalued.Stock prices are a function of expected NOPAT and NOA, as well asthe WACC discount rate. Our higher stock price estimate might bedue to more pessimistic forecasts or a higher discount ratecompared to other investors' and analysts' model assumptions.

Our stock price estimate is slightly higher than the WMT marketprice, indicating that we believe that WMT stock is slightlyovervalued. Stock prices are a function of expected NOPAT and NOA,as well as the WACC discount rate. Our higher stock price estimatemight be due to more pessimistic forecasts or a higher discountrate compared to other investors' and analysts' modelassumptions.

d. If WACC had been 7.5%, what would the valuation estimate havebeen? What about if WACC has been 6.5%?

The valuation estimate at 7.5% would be lower than the estimatecalculated in part a because the discount rate increased. Incontrast, the valuation estimate at 6.5% would be higher than ourestimate.

The valuation estimate at 7.5% would be higher than the estimatecalculated in part a because the discount rate increased. Incontrast, the valuation estimate at 6.5% would be lower than ourestimate.

The valuation estimate would be the same regardless of the rateused to compute the estimate.

Modern Building Supply sells various building materials toretail outlets. The company has just approached Linden State Bankrequesting a $300,000 loan to strengthen the Cash account and topay certain pressing short-term obligations. The companyâsfinancial statements for the most recent two years follow:

| Modern Building Supply Comparative Balance Sheet | ||||

| This Year | Last Year | |||

| Assets | ||||

| Current assets: | ||||

| Cash | $ | 66,000 | $ | 136,000 |

| Marketablesecurities | 0 | 17,000 | ||

| Accounts receivable,net | 467,000 | 298,000 | ||

| Inventory | 934,000 | 599,000 | ||

| Prepaid expenses | 18,000 | 25,000 | ||

| Total current assets | 1,485,000 | 1,075,000 | ||

| Plant and equipment, net | 1,558,022 | 1,435,936 | ||

| Total assets | $ | 3,043,022 | $ | 2,510,936 |

| Liabilities and Stockholders'Equity | ||||

| Liabilities: | ||||

| Current liabilities | $ | 804,000 | $ | 432,000 |

| Bonds payable, 8% | 618,000 | 618,000 | ||

| Total liabilities | 1,422,000 | 1,050,000 | ||

| Stockholders' equity: | ||||

| Preferred stock, $25 par,7% | 275,000 | 275,000 | ||

| Common stock, $10par | 509,000 | 509,000 | ||

| Retained earnings | 837,022 | 676,936 | ||

| Total stockholders' equity | 1,621,022 | 1,460,936 | ||

| Total liabilities and stockholder's equity | $ | 3,043,022 | $ | 2,510,936 |

| Modern Building Supply Comparative Income Statement and Reconciliation | ||||

| This Year | Last Year | |||

| Sales | $ | 5,015,000 | $ | 4,354,000 |

| Costof goods sold | 3,859,000 | 3,444,000 | ||

| Gross margin | 1,156,000 | 910,000 | ||

| Selling and administrative expenses | 638,000 | 538,000 | ||

| Netoperating income | 518,000 | 372,000 | ||

| Interest expense | 49,440 | 49,440 | ||

| Netincome before taxes | 468,560 | 322,560 | ||

| Income taxes (40%) | 187,424 | 129,024 | ||

| Netincome | 281,136 | 193,536 | ||

| Dividends paid: | ||||

| Preferred dividends | 19,250 | 19,250 | ||

| Common dividends | 101,800 | 76,350 | ||

| Total dividends paid | 121,050 | 95,600 | ||

| Netincome retained | 160,086 | 97,936 | ||

| Retained earnings, beginning of year | 676,936 | 579,000 | ||

| Retained earnings, end of year | $ | 837,022 | $ | 676,936 |

During the past year,the company has expanded the number of lines that it carries inorder to stimulate sales and increase profits. It has also movedaggressively to acquire new customers. Sales terms are 2/10, n/30.All sales are on account. |

| Assume that the followingratios are typical of companies in the building supplyindustry: |

| Current ratio | 2.5 | |

| Acid-test ratio | 1.2 | |

| Average collection period | 18 | days |

| Average sale period | 50 | days |

| Debt-to-equity ratio | 0.75 | |

| Times interest earned ratio | 6.0 | |

| Return on total assets | 10 | % |

| Price-earnings ratio | 9 | |

Assume that you havejust inherited several hundred shares of Modern Building Supplystock. Not being acquainted with the company, you decide to do someanalytical work before making a decision about whether to retain orsell the stock you have inherited. |

| Required: | |

| 1. | You decide first to assess the well-being of the commonstockholders. For both this year and last year, compute thefollowing: |

| a. | The earnings per share.(Round your answers to 2 decimalplaces.) |

| This year | Last year | |

| Earnings per share | $ | $ |

| b. | The dividend yield ratio for common stock. The companyâs commonstock is currently selling for $34.51 per share; last year it soldfor $26.68 per share. (Round your intermediate calculationsto 2 decimal places and final answers to 1 decimalplace.) |

| This year | Last year | |

| Dividend yield ratio | % | % |

| c. | The dividend payout ratio for common stock. (Round yourintermediate calculations to 2 decimal places and final answers to1 decimal place.) |

| This year | Last year | |

| Dividend payout ratio | % | % |

| d. | The price-earnings ratio. (Round your intermediatecalculations to 2 decimal places and final answers to 1 decimalplace.) |

| This year | Last year | |

| Price-earnings ratio | times | times |

| e. | The book value per share of common stock. (Round youranswers to 2 decimal places.) |

| This year | Last year | |

| Bookvalue per share | $ | $ |

| 2. | You decide next to assess the companyâs rate of return. Computethe following for both this year and last year: |

| a. | The return on total assets. (Total assets at the beginning oflast year were $2,270,000.) (Round your intermediatecalculations to whole numbers and final answer to 1 decimalplace.) |

| This year | Last year | |

| Return on total assets | % | % |

| b. | The return on common stockholdersâ equity. (Stockholdersâ equityat the beginning of last year was $1,259,000.)(Round yourintermediate calculations to whole numbers and final answer to 1decimal place.) |

| This year | Last year | |

| Return on common stockholders' equity | % | % |