COMM-2016EL Study Guide - Midterm Guide: Fixed Cost, Toronto General Hospital

28 Oct 2017

School

Department

Course

Professor

Cost Terms

A more detailed look at cost terms will help further our analysis of quantifying how

activities of an organization affect the levels of costs. Many activities affect costs, but for

some costs, volume of a product produced or service provided is the primary driver. Other

costs are more affected by activities not directly related to volume and often have multiple

cost drivers.

There are two types of costs that combine the characteristics of both fixed and variable

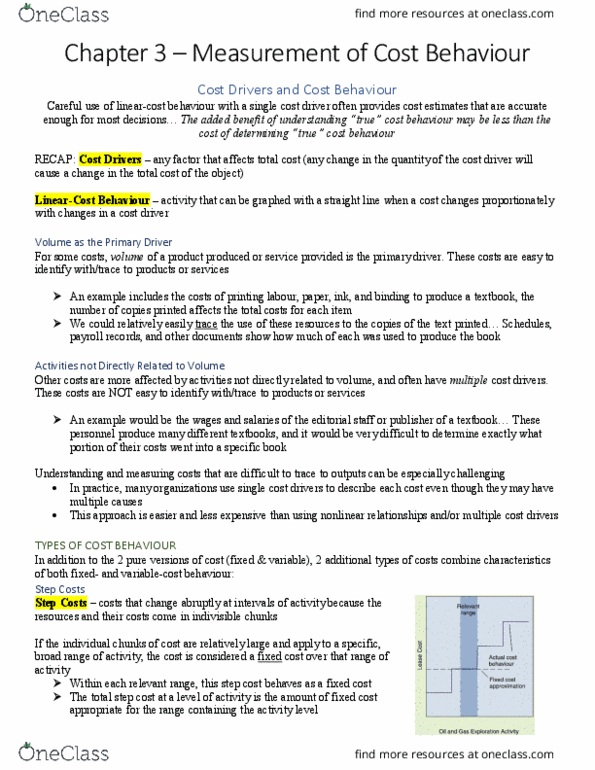

costs behaviour. These are called step costs and mixed costs.

Step- Fixed Costs- within the relevant range, step cost behave like fixed costs. The costs

usually remain fixed when the range is large and a broad range of activities.

Step- Variable Costs- Step costs can also be variable when the range is small. The costs are

variable because a small change in activity changes the costs. For example one waiter can

serve 80 customers in a four hour shift however if between 80-160 customers are expected

than another waiter has to be called in. Thus the number of waiters depends on the block

changes in the number of customers.

Mixed Costs- Contain both fixed and variable behaviours. The cost behaviour is similar to

that of the step fixed costs. Within the relevant range the costs remain fixed. The variable

costs are different than the step- variable costs as these variable costs are incurred in

addition to the fixed cost. Essentially mixed costs are the fixed cost plus the variable costs

incurred. For Example: Toronto General Hospital has an X-ray machine that has a fixed

component which is depreciation and salaries for technicians, however it also has a

variable component such as X-ray film, and supplies. Fixed costs are the costs just to have

machine ready for use, variable costs are based on actual consumption or use.

Committed Fixed Costs- Relates to the investment in facilities and the basic organizational

structure. Usually incurred for the long term and cannot be cut to zero without seriously

impairing the profitability of the company. Even if operations are cut back committed costs

will unchanged. For example: mortgage costs or property taxes.

Discretionary Fixed Costs- (also known as managed fixed costs) - fixed costs that do not

change with the level of production however these are costs that can potentially be added

or deducted during the budget process. For example advertising, research and

development. Discretionary costs are different than committed cost in the sense that these

cost are made for short term planning (annual decisions) and can be cut without impairing

the company profits in the long term.

Document Summary

A more detailed look at cost terms will help further our analysis of quantifying how activities of an organization affect the levels of costs. Many activities affect costs, but for some costs, volume of a product produced or service provided is the primary driver. Other costs are more affected by activities not directly related to volume and often have multiple cost drivers. There are two types of costs that combine the characteristics of both fixed and variable costs behaviour. These are called step costs and mixed costs. Step- fixed costs- within the relevant range, step cost behave like fixed costs. The costs usually remain fixed when the range is large and a broad range of activities. Step- variable costs- step costs can also be variable when the range is small. The costs are variable because a small change in activity changes the costs.