COMMERCE 1AA3 Study Guide - Final Guide: Gross Profit, Debt Ratio, Current Liability

12 Dec 2016

School

Department

Course

Professor

Document Summary

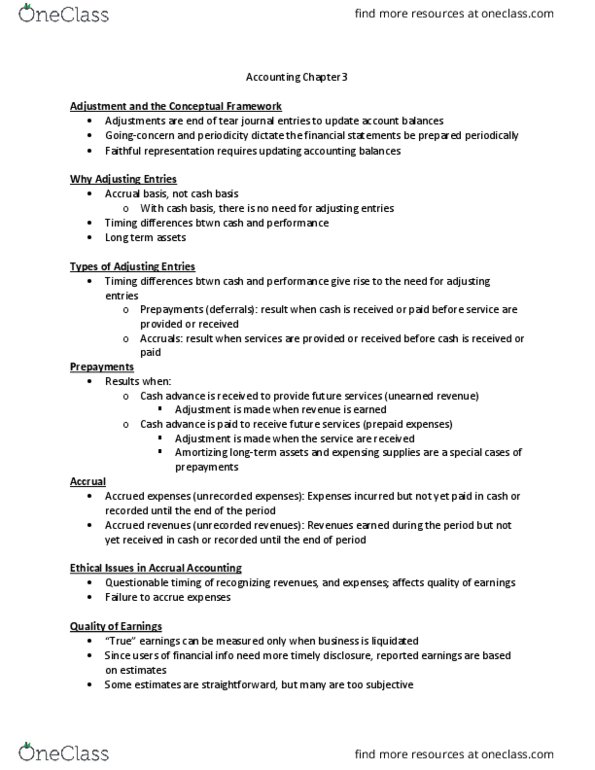

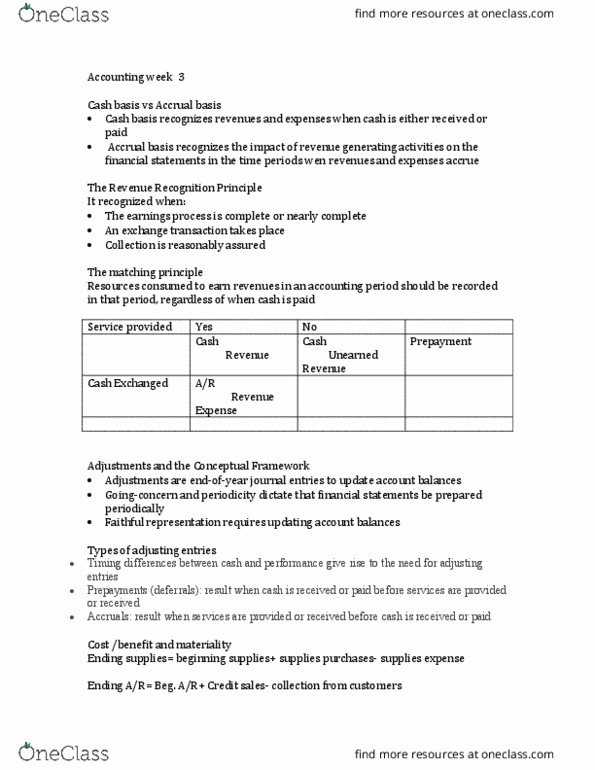

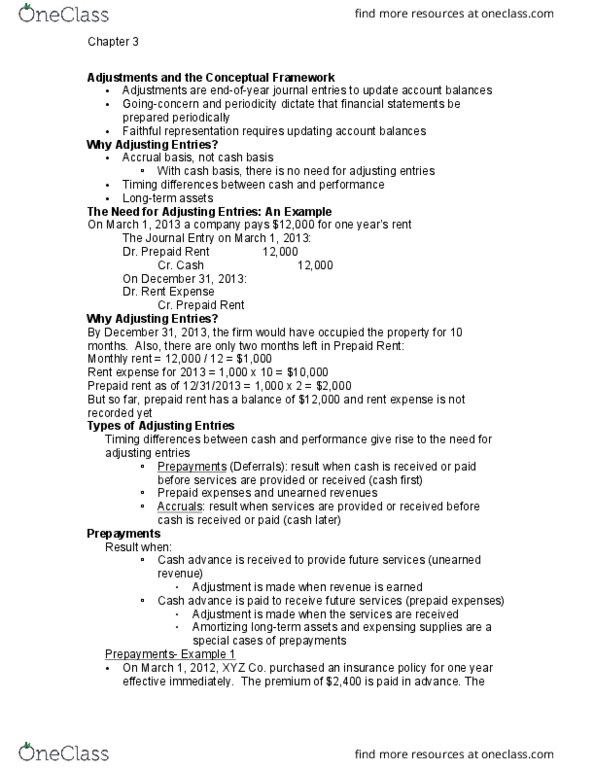

Adjustments: adjustments are end-of-year journal entries to update account balances. Adjusting entries are needed to bring the books up to date for transactions that have taken place but that may not be associated with a single, economic event. Certain revenues and expenses have not been recorded by the end of the period. Adjusting entries ensure that revenues and expenses, and therefore net income, are correct. The revenues and expenses referred to above also have an effect on related asset and liability accounts. Adjusting entries are needed to ensure all balance sheet accounts carry correct balances. Going-concern and periodicity dictate that financial statements be prepared periodically. Faithful representation requires updating account balances: adjusting entries are only required under accrual basis. Deferral prepaid expenses: require adjustment because the cash is paid in one period, but the resource is not completely used until a later period. Examples include prepaid rent, prepaid insurance, and supplies.