COMMERCE 1AA3 Final: AccountingReview

8 Mar 2017

School

Department

Course

Professor

Document Summary

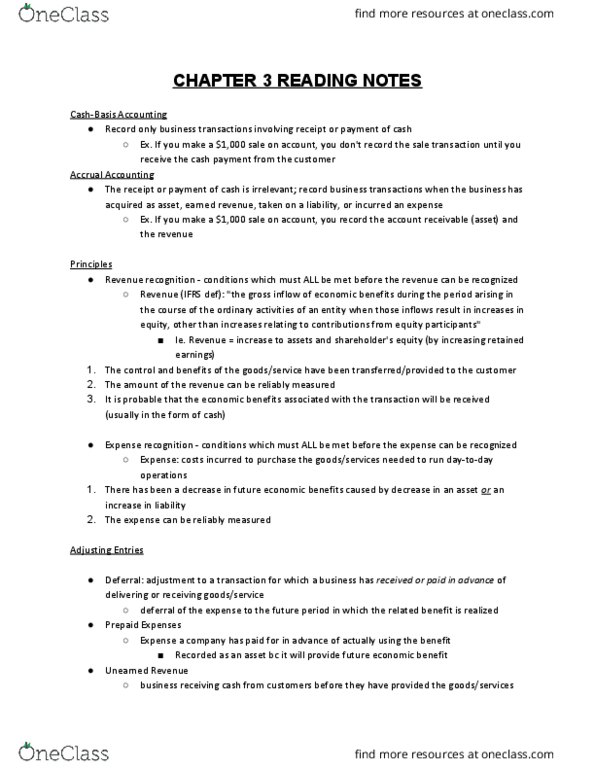

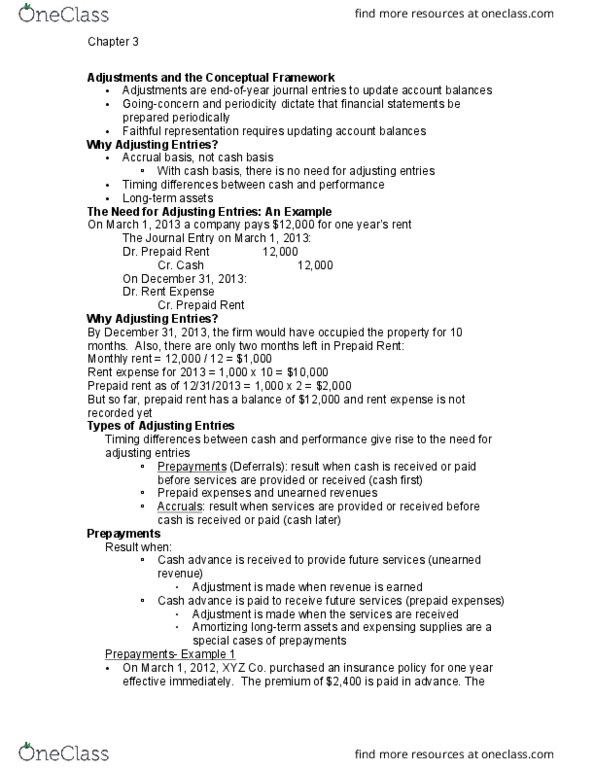

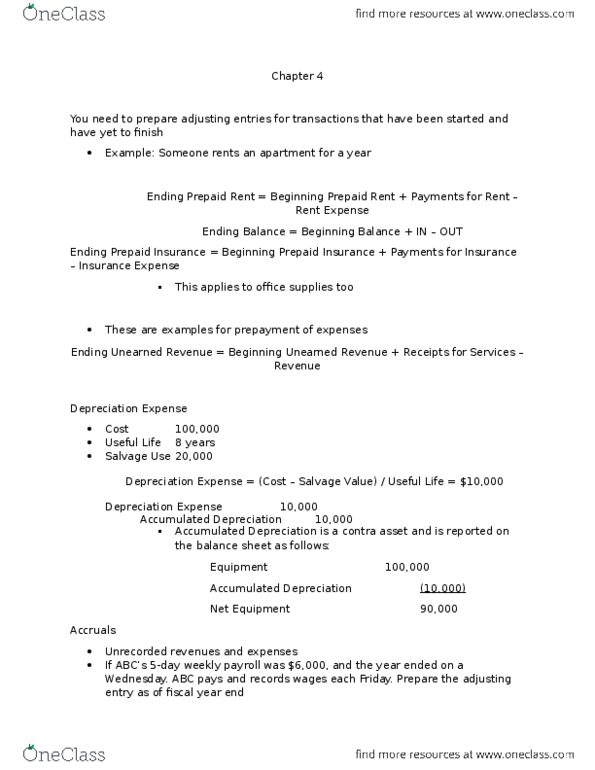

Debit - left, credit - right: purchasing assets. Gain on disposal: providing a service/good for cash. Payable: revenue earned but not yet billed or received. Going-concern assumption and periodicity, faithful representation, matching principle: unearned revenue is now earned. Revenue: prepaid expenses have now been used. Accumulated depreciation (*contra account: supplies have been used. Supplies: accrued expenses have been incurred but not yet paid or billed. Payable: accrued revenue has been earned but not yet billed or received cash. Direct write-off (unacceptable under ifrs because of faithful representation and matching principle) Allowance method (reports a/r at net realizable value - acceptable under ifrs: estimate bad debts expense. Allowance for doubtful accounts: write-off accounts receivable determined to be uncollectible. Accounts receivable: recovery of account previously written-off. Required to close the temporary income statement accounts to prepare for the next period: close the revenue accounts. Assets + expenses + dividends = liabilities + capital + beginning re + revenue.