COMMERCE 1AA3 Quiz: 1AA3 TB Notes

Document Summary

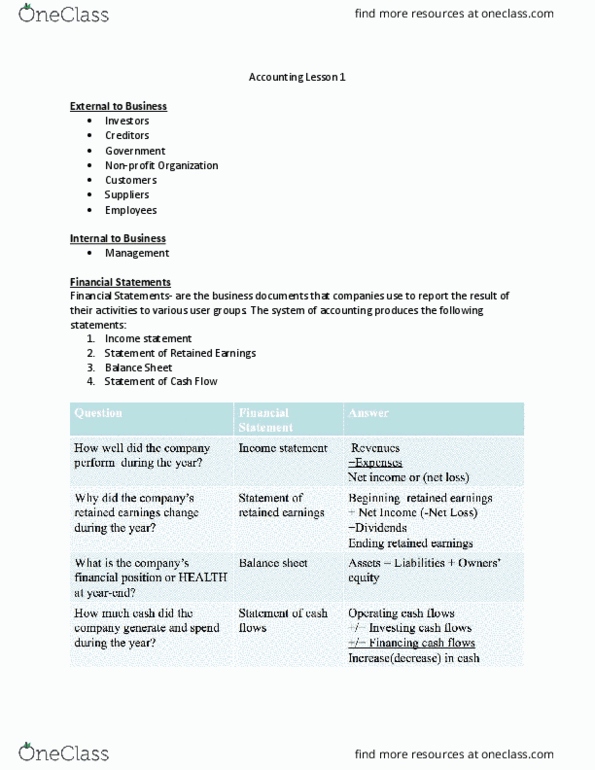

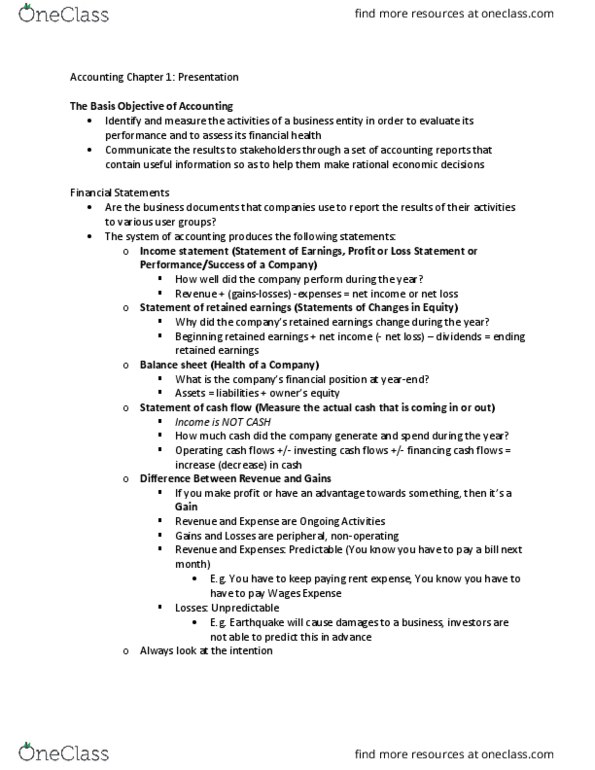

2014-09-09 5:22:00 pm: chapter 1, financial statements, income statement: the statement of profit or loss, measures a company"s operating performance for a specified period of time. The period of time covered by an income statement is typically a month, a quarter (3. Months), or a year: retained earnings: represent the accumulated net income (or net earnings) of the company since the day it started business, less any net losses and dividends declared during this time. They tend to be small businesses or individual professional organizations. The proprietor is personally liable for all business debts. Personal finances are not included: partnerships: is an unincorporated business with two or more parties as co-owners and each owner is a partner. Each partner is personally liable for all partnership debts: corporations: a corporation is an incorporated business owned by uts shareholders who own shares representing partial ownership of the corporation.