COMMERCE 1BA3 Study Guide - Midterm Guide: International Financial Reporting Standards, Deferral, Revenue Recognition

11 Oct 2013

School

Department

Course

Professor

Document Summary

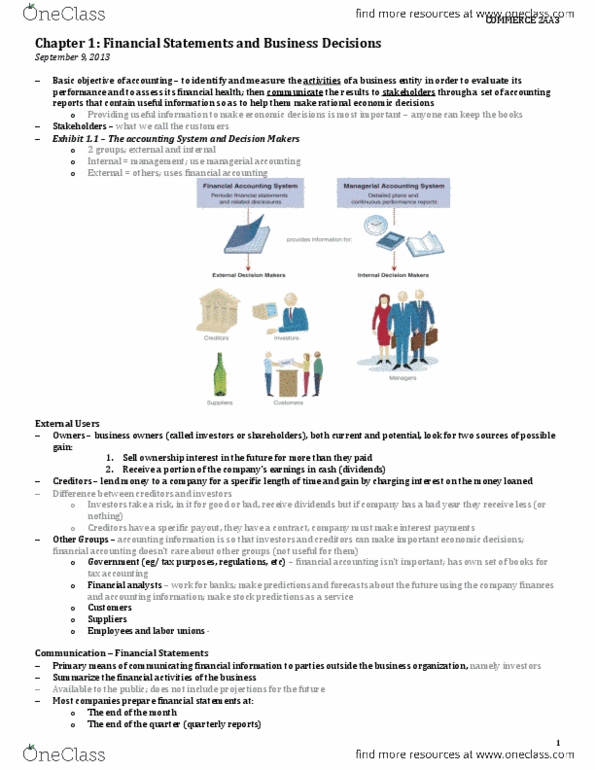

Creditors lend money to a company for a specific length of time; gain by charging interest on money loaned: not associated with risk; contract binds company to specific payout. Other groups (not important) government (tax, regulations), financial analysts, customers, suppliers, employees and labor unions. Primary means of communicating financial information to parties outside organization; summarize financial activities of business. Prepared at end of month, quarter (quarterly), year (annually) annual shows broader picture, more accurate; monthly can cause unwarranted worry. Generally accepted accounting principles (gaap) replaced by international financial reporting standards (ifrs) Covers a period of time: revenue earnings from the sale of goods or services; increase in assets or settlement of liabilities from ongoing operations; Revenue recognition principle recognize when service performed or goods delivered (not with cash payment: expenses dollar amount of resources used by the entity to earn revenues during a period. + profit for the year (income from i/s)