COMMERCE 2AB3 Study Guide - Midterm Guide: Direct Labor Cost, Cost Driver, Cost Estimate

7 Feb 2014

School

Department

Course

Professor

Document Summary

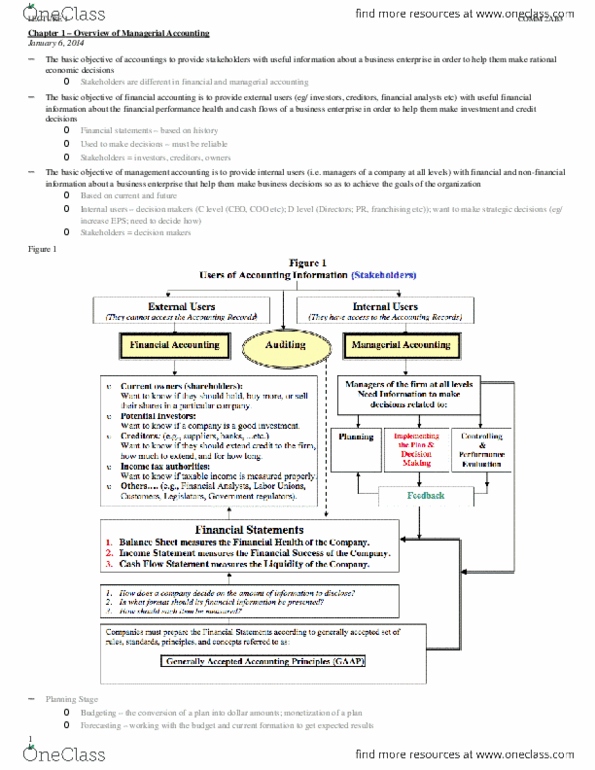

To provide stakeholders with useful information about a business enterprise. To provide external users with useful financial information in order to make investment and credit decisions. To provide internal user with financial information and non-financial information as to achieve the goals of the organization. Planning: establishing goals and objectives, predicting results, and drawing a detailed plan of who will do what, when and how to achieve the desired goals. Implementing the plan and decision making: directing, motivating and measuring performance. Controlling and performance evaluation: keeping the firm"s activities on track and ensuring that the plan has been followed in the implementation process. Agency theory: decision maker does not think about the company but only for themselves. Similarities and differences between financial and managerial accounting. Internal users: managers of a firm at all levels. General purpose to help external users make investment & credit decisions. Special-purpose for a particular user for a specific decision.