COMMERCE 3FA3 Study Guide - Midterm Guide: Canadian Airlines, Air Canada, Financial Distress

5 Jun 2018

School

Department

Course

Professor

The

ratio of a company

•

The Capital Structure Question

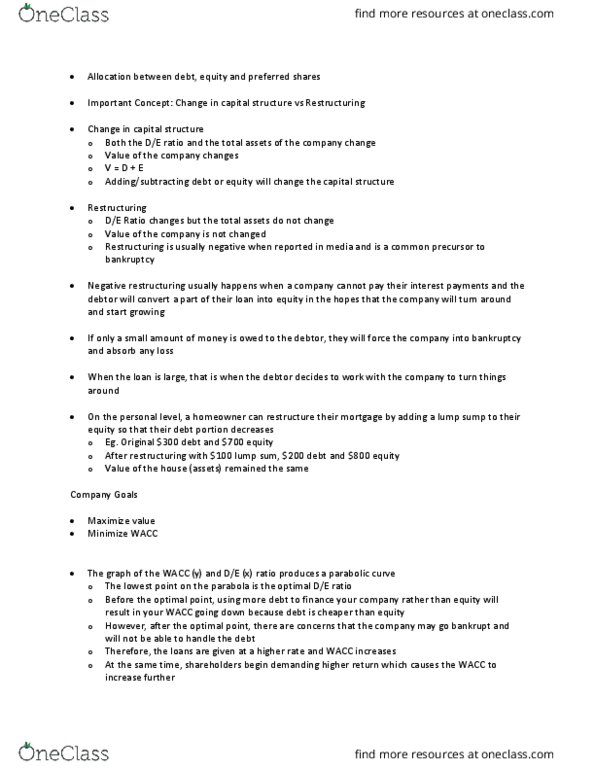

Change in capital structure includes raising money to fund growth, debt or equity

•

Negative when features conversion of debt to equity

○

Positive when features the issuing of equity to repay debt (shares are overvalued), or the issuing of debt to buy

back equity (when shares are undervalued)

○

Restructuring often features bankruptcy

•

Restructuring

Change in Capital Structure

ratio changes

ratio changes

Total assets do not change

Total assets change

Generally assumed to be bad

Generally assumed to be good

Minimizing WACC maximizes the value of the firm's cashflows so the optimal capital structure is the target capital

structure of the firm

•

Effect on WACC

Financial leverage is the extent to which a firm relies on debt

•

Can alter payoff to shareholders, but may not affect the WACC

•

Using debt to finance makes EPS and ROE more risky

•

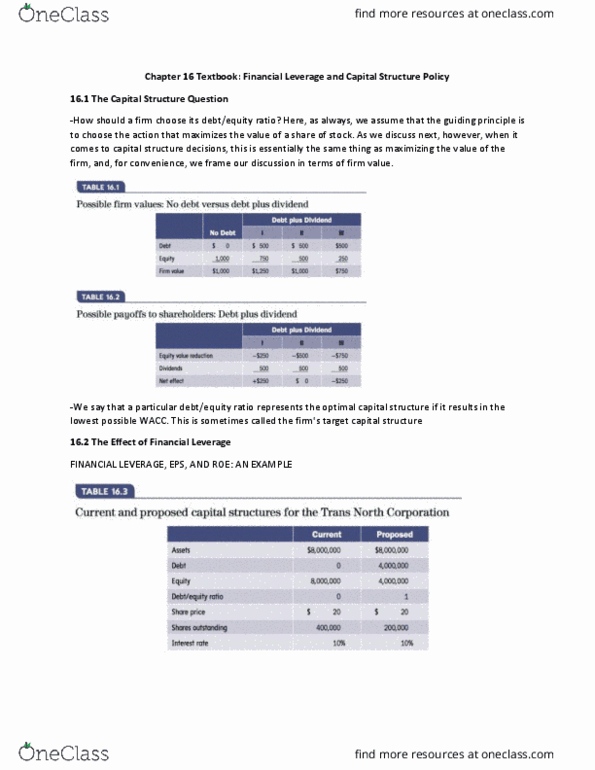

The Effect of Financial Leverage

The effect of financial leverage depends on EBIT - when EBIT is projected to increase, leverage is beneficial

•

Leverage increases returns to shareholders, measured by ROE and EPS

•

More risk due to EPS and ROE sensitivity to changes in EBIT

•

Capital structure is irrelevant when individuals borrow at the same rate as corporations

•

Homemade leverage is the use of personal borrowing to change the overall amount of financial leverage to which an

individual is exposed

•

Homemade Leverage and Corporate Borrowing

Capital Structure and the Cost of Equity Capital

WACC is the same no matter what capital structure used

○

Goal to maximize value of the firm

○

M&M Proposition I states that it is irrelevant how a firm chooses how to arrange its finances, the value of the firm is

independent of the capital structure

•

Debt financing is highly advantageous and WACC decreases as firm relies on debt financing

○

With taxes (Case 2), the value of the firm leveraged equals the value of the firm unleveraged plus the present value of

the interest tax shield

•

M&M Propositions

= value of unlevered firm - firm without debt

= equity required return for unlevered firm

= market value of equity

= market value of debt

= earnings before interest and tax/perpetual

operating income

With tax case.

= amount of debt

= tax rate

= tax shield

Financial Leverage and Capital Structure Policy

January 20, 2018

2:06 PM

Managerial Finance Page 1

Document Summary

The capital structure question ratio of a company. Generally assumed to be bad generally assumed to be good. Change in capital structure includes raising money to fund growth, debt or equity. Negative when features conversion of debt to equity. Positive when features the issuing of equity to repay debt (shares are overvalued), or the issuing of debt to buy back equity (when shares are undervalued) Minimizing wacc maximizes the value of the firm"s cashflows so the optimal capital structure is the target capital structure of the firm. Financial leverage is the extent to which a firm relies on debt. Can alter payoff to shareholders, but may not affect the wacc. Using debt to finance makes eps and roe more risky. The effect of financial leverage depends on ebit - when ebit is projected to increase, leverage is beneficial. Leverage increases returns to shareholders, measured by roe and eps. More risk due to eps and roe sensitivity to changes in ebit.