COMM 112 Study Guide - Midterm Guide: 2011 Nfl Season, Fixed Cost, Earnings Before Interest And Taxes

10 Feb 2013

School

Department

Course

Professor

Document Summary

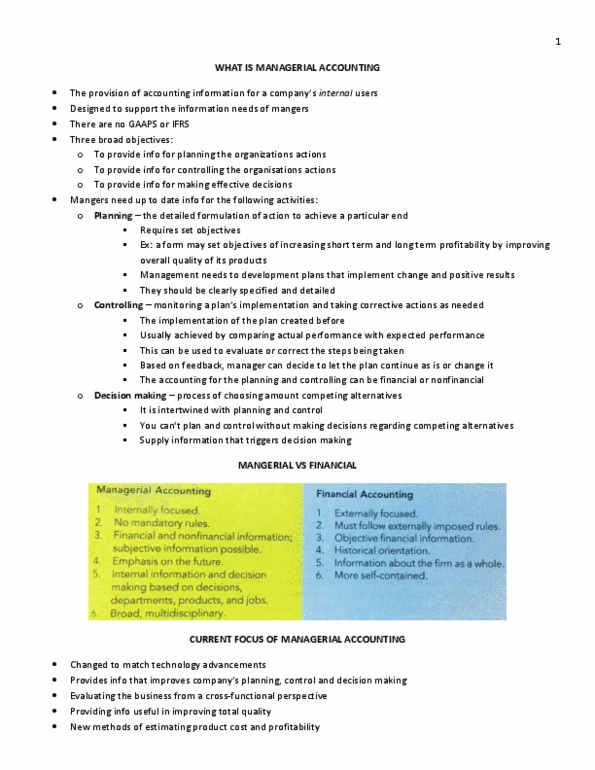

Managerial accounting the provision of accounting information for a company"s internal users. It is the firm"s internal accounting system and is designed to support the information needs of managers particular end corrective action as needed. Value chain the set of business functions that add value to an organization"s products or services. Information for decision making the process of choosing among alternatives. Information for planning the detailed formation of action to achieve a. Information for controlling monitoring a plan"s implementation and taking. Continuous improvement the continual search for ways to increase the overall efficiency and productivity of activities by reducing waste, increasing quality, and managing costs. Total quality management (tqm) manufacturers strive to create an environment that will enable workers to manufacture perfect (zero-defect) products. Lean accounting organizes costs according to the value chain and collects both financial and nonfinancial information. Line positions positions that have direct responsibility for the basic objectives of an organization.