ACC 514 Study Guide - Finance Lease, Cash Flow, Accrual

Document Summary

Get access

Related Documents

Related Questions

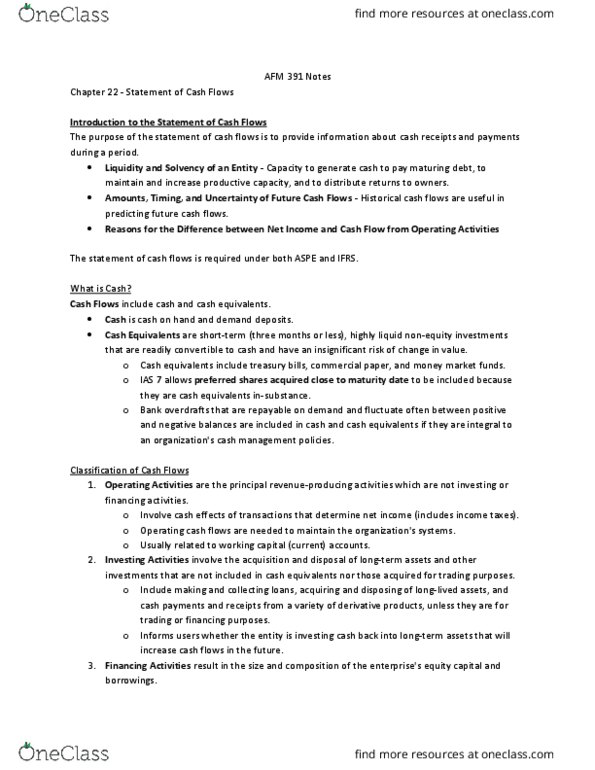

Perform a vertical and horizontal analysis of Wal-Mart Stores,Inc.âs income statements and balance sheets as of January 31, 2015.In performing this analysis, consider any notable trends or changesthat you observe that may provide useful information concerning itsfinancial condition. Also use as many yearsâ worth of statements asyou feel necessary.

| WAL MART STORESINC | ||||

| 10-K | ||||

| Statement of CashFlows | ||||

| (Amounts in millions) | ||||

| Fiscal Year Ended January 31, | 2015 | 2014 | 2013 | 2012 |

| Cash flows from operating activities: | ||||

| Consolidated net income | $17,099 | $16,695 | $17,756 | $16,387 |

| (Income) Loss from discontinuedoperations, net of tax | (285) | (144) | (52) | 21 |

| Income from continuing operations | 16,814 | 16,551 | 17,704 | 16,408 |

| Adjustments to reconcileincome from continuing operations to net cash provided by operatingactivities | ||||

| Depreciation and amortization | 9,173 | 8,870 | 8,478 | 8,106 |

| Deferred income taxes | (503) | (279) | (133) | 1,050 |

| Other operating activities | 785 | 938 | 602 | 468 |

| Changes in certain assets and liabilities,net of effects of acquisitions: | ||||

| Increase in accounts receivable | (569) | (566) | (614) | (796) |

| Increase in inventories | (1,229) | (1,667) | (2,759) | (3,727) |

| Increase in accounts payable | 2,678 | 531 | 1,061 | 2,687 |

| Increase in accrued liabilities | 1,249 | 103 | 271 | 30 |

| (Decrease) Increase in accrued incometaxes | 166 | (1,224) | 981 | 29 |

| Net cash provided by operatingactivities | 28,564 | 23,257 | 25,591 | 24,255 |

| Cash flows from investing activities: | ||||

| Payments for property and equipment | (12,174) | (13,115) | (12,898) | (13,510) |

| Proceeds from disposal of property andequipment | 570 | 727 | 532 | 580 |

| Proceeds from disposal of certainoperations | 671 | 0 | 0 | 0 |

| Other investing activities | (192) | (138) | (271) | (3,679) |

| Net cash used in investingactivities | (11,125) | (12,526) | (12,637) | (16,609) |

| Cash flows from financing activities: | ||||

| Net change in short-term borrowings | (6,288) | 911 | 2,754 | 3,019 |

| Proceeds from issuance of long-termdebt | 5,174 | 7,072 | 211 | 5,050 |

| Payment of long-term debt | (3,904) | (4,968) | (1,478) | (4,584) |

| Dividends paid | (6,185) | (6,139) | (5,361) | (5,048) |

| Purchase of Company stock | (1,015) | (6,683) | (7,600) | (6,298) |

| Dividends paid to noncontrollinginterest | (600) | (426) | (282) | (526) |

| Purchase of noncontrolling interest | (1,844) | (296) | (132) | 0 |

| Other financing activities | (409) | (260) | (58) | (71) |

| Net cash used in financingactivities | (15,071) | (10,789) | (11,946) | (8,458) |

| Effect of exchange rates on cash | (514) | (442) | 223 | (33) |

| Net (decrease) increase in cash and cashequivalents | 1,854 | (500) | 1,231 | (845) |

| Cash and cash equivalents at beginning ofyear | 7,281 | 7,781 | 6,550 | 7,395 |

| Cash and cash equivalents at endof year | $9,135 | $7,281 | $7,781 | $6,550 |

| Supplemental disclosure of cash flowinformation | ||||

| Income tax paid | 8,169 | 8,641 | 7,304 | 5,889 |

| Interest paid | 2,433 | 2,362 | 2,262 | 2,346 |

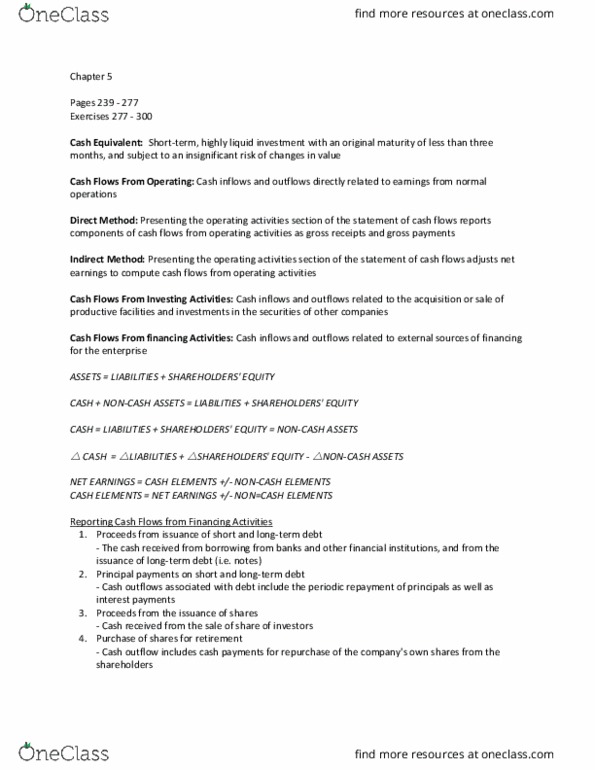

| Assess Wal-Mart, Stores Inc. concerning liquidity, solvency,profitability, and stock performance as of January 31, 2015. Foreach area, you should calculate the ratios we discussed in classand provide an analysis of the ratios calculated. I includehistorical stock price information and outstanding common shareinformation below.

WAL MART STORES INC | |||||||||||||||||||

| 10-K | |||||||||||||||||||

| Statement of CashFlows | |||||||||||||||||||

| (Amounts in millions) | |||||||||||||||||||

| Fiscal Year Ended January 31, | 2015 | 2014 | 2013 | 2012 | |||||||||||||||

| Cash flows from operating activities: | |||||||||||||||||||

| Consolidated net income | $17,099 | $16,695 | $17,756 | $16,387 | |||||||||||||||

| (Income) Loss from discontinuedoperations, net of tax | (285) | (144) | (52) | 21 | |||||||||||||||

| Income from continuing operations | 16,814 | 16,551 | 17,704 | 16,408 | |||||||||||||||

| Adjustments to reconcileincome from continuing operations to net cash provided by operatingactivities | |||||||||||||||||||

| Depreciation and amortization | 9,173 | 8,870 | 8,478 | 8,106 | |||||||||||||||

| Deferred income taxes | (503) | (279) | (133) | 1,050 | |||||||||||||||

| Other operating activities | 785 | 938 | 602 | 468 | |||||||||||||||

| Changes in certain assets and liabilities,net of effects of acquisitions: | |||||||||||||||||||

| Increase in accounts receivable | (569) | (566) | (614) | (796) | |||||||||||||||

| Increase in inventories | (1,229) | (1,667) | (2,759) | (3,727) | |||||||||||||||

| Increase in accounts payable | 2,678 | 531 | 1,061 | 2,687 | |||||||||||||||

| Increase in accrued liabilities | 1,249 | 103 | 271 | 30 | |||||||||||||||

| (Decrease) Increase in accrued incometaxes | 166 | (1,224) | 981 | 29 | |||||||||||||||

| Net cash provided by operatingactivities | 28,564 | 23,257 | 25,591 | 24,255 | |||||||||||||||

| Cash flows from investing activities: | |||||||||||||||||||

| Payments for property and equipment | (12,174) | (13,115) | (12,898) | (13,510) | |||||||||||||||

| Proceeds from disposal of property andequipment | 570 | 727 | 532 | 580 | |||||||||||||||

| Proceeds from disposal of certainoperations | 671 | 0 | 0 | 0 | |||||||||||||||

| Other investing activities | (192) | (138) | (271) | (3,679) | |||||||||||||||

| Net cash used in investingactivities | (11,125) | (12,526) | (12,637) | (16,609) | |||||||||||||||

| Cash flows from financing activities: | |||||||||||||||||||

| Net change in short-term borrowings | (6,288) | 911 | 2,754 | 3,019 | |||||||||||||||

| Proceeds from issuance of long-termdebt | 5,174 | 7,072 | 211 | 5,050 | |||||||||||||||

| Payment of long-term debt | (3,904) | (4,968) | (1,478) | (4,584) | |||||||||||||||

| Dividends paid | (6,185) | (6,139) | (5,361) | (5,048) | |||||||||||||||

| Purchase of Company stock | (1,015) | (6,683) | (7,600) | (6,298) | |||||||||||||||

| Dividends paid to noncontrollinginterest | (600) | (426) | (282) | (526) | |||||||||||||||

| Purchase of noncontrolling interest | (1,844) | (296) | (132) | 0 | |||||||||||||||

| Other financing activities | (409) | (260) | (58) | (71) | |||||||||||||||

| Net cash used in financingactivities | (15,071) | (10,789) | (11,946) | (8,458) | |||||||||||||||

| Effect of exchange rates on cash | (514) | (442) | 223 | (33) | |||||||||||||||

| Net (decrease) increase in cash and cashequivalents | 1,854 | (500) | 1,231 | (845) | |||||||||||||||

| Cash and cash equivalents at beginning ofyear | 7,281 | 7,781 | 6,550 | 7,395 | |||||||||||||||

| Cash and cash equivalents at endof year | $9,135 | $7,281 | $7,781 | $6,550 | |||||||||||||||

| Supplemental disclosure of cash flowinformation | |||||||||||||||||||

| Income tax paid | 8,169 | 8,641 | 7,304 | 5,889 | |||||||||||||||

| Interest paid | 2,433 | 2,362 | 2,262 | 2,346 | |||||||||||||||

Stock Performance

Calculations:

Book value per common share: book value ofequity / common shares outstanding = Step by st for2015 =

Earnings per share (Basic) according to Income Statementis $5.07

Earnings per share (Diluted) according to IncomeStatement is $5.05

P/E Ratio: adjusted closing price / earningsper share (diluted) = Step by step for 2015=

Dividend yield: dividend per share / adjustedclosing price = Step by step for 2015=

Dividend payout: dividend per share / earningsper share (diluted) = Step by step for 2015=

Adjusted basic EPS: adjusted net income /Weighted average shares outstanding: basic

Adjusted diluted EPS: adjusted net income /Weighted average shares outstanding: diluted

Adjusted P/E ratio: adjusted closing price /adjusted diluted EPS

Adjusted dividend payout: Dividends per share /adjusted diluted EPS

Fiscal Year Ended | 2/1/2015 | 2/2/2014 | 2/3/2013 | 1/29/2012 |

Book value per common share | ? | ? | ? | ? |

Earnings per share (basic) | ? | ? | ? | ? |

Earnings per share (diluted) | ? | ? | ? | ? |

P/E Ratio | ? | ? | ? | ? |

Dividend yield | ? | ? | ? | ? |

Dividend payout | ? | ? | ? | ? |

Adjusted Basic EPS | ? | ? | ? | ? |

Adjusted Diluted EPS | ? | ? | ? | ? |

Adjusted P/E Ratio | ? | ? | ? | ? |

Adjusted dividend payout | ? | ? | ? | ? |

Book value of equity | ? | ? | ? | ? |

Common shares outstanding | ? | ? | ? | ? |

Adjusted closing price | ? | ? | ? | ? |

Dividends per share | ? | ? | ? | ? |

Information:

| WAL MART STORESINC | ||||

| 10-K | ||||

| Statement of CashFlows | ||||

| (Amounts in millions) | ||||

| Fiscal Year Ended January 31, | 2015 | 2014 | 2013 | 2012 |

| Cash flows from operating activities: | ||||

| Consolidated net income | $17,099 | $16,695 | $17,756 | $16,387 |

| (Income) Loss from discontinuedoperations, net of tax | (285) | (144) | (52) | 21 |

| Income from continuing operations | 16,814 | 16,551 | 17,704 | 16,408 |

| Adjustments to reconcileincome from continuing operations to net cash provided by operatingactivities | ||||

| Depreciation and amortization | 9,173 | 8,870 | 8,478 | 8,106 |

| Deferred income taxes | (503) | (279) | (133) | 1,050 |

| Other operating activities | 785 | 938 | 602 | 468 |

| Changes in certain assets and liabilities,net of effects of acquisitions: | ||||

| Increase in accounts receivable | (569) | (566) | (614) | (796) |

| Increase in inventories | (1,229) | (1,667) | (2,759) | (3,727) |

| Increase in accounts payable | 2,678 | 531 | 1,061 | 2,687 |

| Increase in accrued liabilities | 1,249 | 103 | 271 | 30 |

| (Decrease) Increase in accrued incometaxes | 166 | (1,224) | 981 | 29 |

| Net cash provided by operatingactivities | 28,564 | 23,257 | 25,591 | 24,255 |

| Cash flows from investing activities: | ||||

| Payments for property and equipment | (12,174) | (13,115) | (12,898) | (13,510) |

| Proceeds from disposal of property andequipment | 570 | 727 | 532 | 580 |

| Proceeds from disposal of certainoperations | 671 | 0 | 0 | 0 |

| Other investing activities | (192) | (138) | (271) | (3,679) |

| Net cash used in investingactivities | (11,125) | (12,526) | (12,637) | (16,609) |

| Cash flows from financing activities: | ||||

| Net change in short-term borrowings | (6,288) | 911 | 2,754 | 3,019 |

| Proceeds from issuance of long-termdebt | 5,174 | 7,072 | 211 | 5,050 |

| Payment of long-term debt | (3,904) | (4,968) | (1,478) | (4,584) |

| Dividends paid | (6,185) | (6,139) | (5,361) | (5,048) |

| Purchase of Company stock | (1,015) | (6,683) | (7,600) | (6,298) |

| Dividends paid to noncontrollinginterest | (600) | (426) | (282) | (526) |

| Purchase of noncontrolling interest | (1,844) | (296) | (132) | 0 |

| Other financing activities | (409) | (260) | (58) | (71) |

| Net cash used in financingactivities | (15,071) | (10,789) | (11,946) | (8,458) |

| Effect of exchange rates on cash | (514) | (442) | 223 | (33) |

| Net (decrease) increase in cash and cashequivalents | 1,854 | (500) | 1,231 | (845) |

| Cash and cash equivalents at beginning ofyear | 7,281 | 7,781 | 6,550 | 7,395 |

| Cash and cash equivalents at endof year | $9,135 | $7,281 | $7,781 | $6,550 |

| Supplemental disclosure of cash flowinformation | ||||

| Income tax paid | 8,169 | 8,641 | 7,304 | 5,889 |

| Interest paid | 2,433 | 2,362 | 2,262 | 2,346 |

| WAL MART STORESINC | ||||

| 10-K | ||||

| Balance Sheet | ||||

| (Amounts in millions except per sharedata) | ||||

| January 31, | 2015 | 2014 | 2013 | 2012 |

| ASSETS | ||||

| Current assets: | ||||

| Cash and cash equivalents | $9,135 | $7,281 | $7,781 | $6,550 |

| Receivables | 6,778 | 6,677 | 6,768 | 5,937 |

| Inventories | 45,141 | 44,858 | 43,803 | 40,714 |

| Prepaid expenses and other | 2,224 | 1,909 | 1,551 | 1,685 |

| Current assets of discontinuedoperations | 0 | 460 | 37 | 89 |

| Total current assets | $63,278 | $61,185 | $59,940 | $54,975 |

| Property and equipment, at cost | 177,395 | 173,089 | 165,825 | 155,002 |

| Less accumulated depreciation | (63,115) | (57,725) | (51,896) | (45,399) |

| Property and equipment, net | 114,280 | 115,364 | 113,929 | 109,603 |

| Property under capital lease | 5,239 | 5,589 | 5,899 | 5,936 |

| Less accumulated amortization | (2,864) | (3,046) | (3,147) | (3,215) |

| Property under capital lease, net | 2,375 | 2,543 | 2,752 | 2,721 |

| Goodwill | 18,102 | 19,510 | 20,497 | 20,651 |

| Other assets and deferred charges | 5,671 | 6,149 | 5,987 | 5,456 |

| Total assets | $203,706 | $204,751 | $203,105 | $193,406 |

| LIABILITIES ANDSHAREHOLDERS EQUITY | ||||

| Current liabilities: | ||||

| Short-term borrowings | $1,592 | $7,670 | $6,805 | $4,047 |

| Accounts payable | 38,410 | 37,415 | 38,080 | 36,608 |

| Accrued liabilities | 19,152 | 18,793 | 18,808 | 18,154 |

| Accrued income taxes | 1,021 | 966 | 2,211 | 1,164 |

| Long-term debt due within one year | 4,810 | 4,103 | 5,587 | 1,975 |

| Obligations under capital leases duewithin one year | 287 | 309 | 327 | 326 |

| Current liabilities of discontinuedoperations | 0 | 89 | 0 | 26 |

| Total currentliabilities | 65,272 | 69,345 | 71,818 | 62,300 |

| Long-term debt | 41,086 | 41,771 | 38,394 | 44,070 |

| Long-term obligations under capitalleases | 2,606 | 2,788 | 3,023 | 3,009 |

| Deferred income taxes and other | 8,805 | 8,017 | 7,613 | 7,862 |

| Redeemable non-controlling interest | 0 | 1,491 | 519 | 404 |

| Commitments and contingencies | 0 | 0 | 0 | 0 |

| Shareholders equity: | ||||

| Common stock | 323 | 323 | 332 | 342 |

| Capital in excess of par value | 2,462 | 2,362 | 3,620 | 3,692 |

| Retained earnings | 85,777 | 76,566 | 72,978 | 68,691 |

| Accumulated other comprehensive income(loss) | (7,168) | (2,996) | (587) | (1,410) |

| Total Walmart shareholders' equity | 81,394 | 76,255 | 76,343 | 71,315 |

| Noncontrolling interest | 4,543 | 5,084 | 5,395 | 4,446 |

| Total equity | 85,937 | 81,339 | 81,738 | 75,761 |

| Total liabilities and shareholdersequity | $203,706 | $204,751 | $203,105 | $193,406 |

| WAL MART STORESINC | ||||

| 10-K | ||||

| Income Statement | ||||

| (Amounts in millions except per sharedata) | ||||

| Fiscal Year Ended January 31, | 2015 | 2014 | 2013 | 2012 |

| Revenues: | ||||

| Net sales | $482,229 | $473,076 | ####### | $443,416 |

| Membership and other income | 3,422 | 3,218 | 3,047 | 3,093 |

| 485,651 | 476,294 | 468,651 | 446,509 | |

| Costs and expenses: | ||||

| Cost of sales | 365,086 | 358,069 | 352,297 | 334,993 |

| Operating, selling, general andadministrative expenses | 93,418 | 91,353 | 88,629 | 85,025 |

| Operating income | 27,147 | 26,872 | 27,725 | 26,491 |

| Interest: | ||||

| Debt | 2,161 | 2,072 | 1,977 | 2,034 |

| Capital leases | 300 | 263 | 272 | 286 |

| Interest expense | 2,461 | 2,335 | 2,249 | 2,320 |

| Interest income | (113) | (119) | (186) | (161) |

| Interest, net | 2,348 | 2,216 | 2,063 | 2,159 |

| Income from continuing operations beforeincome taxes | 24,799 | 24,656 | 25,662 | 24,332 |

| Provision for income taxes: | ||||

| Current | 8,504 | 8,619 | 7,976 | 6,722 |

| Deferred | (519) | (514) | (18) | 1,202 |

| Total provision for income taxes | 7,985 | 8,105 | 7,958 | 7,924 |

| Income from continuing operations | 16,814 | 16,551 | 17,704 | 16,408 |

| Income (Loss) from discontinuedoperations, net of tax | 285 | 144 | 52 | (21) |

| Consolidated net income | 17,099 | 16,695 | 17,756 | 16,387 |

| Consolidated net income attributable tononcontrolling interest | (736) | (673) | (757) | (688) |

| Consolidated net incomeattributable to Walmart | $16,363 | $16,022 | $16,999 | $15,699 |

| Net income per common share: | ||||

| Basic income per common share fromcontinuing operations to Walmart | $5.01 | $4.87 | $5.03 | $4.55 |

| Basic income (loss) per common share fromdiscontinued operations | $0.06 | $0.03 | $0.01 | ($0.01) |

| Basic net income per common shareattributable to Walmart | $5.07 | $4.90 | $5.04 | $4.54 |

| Diluted income per common share fromcontinuing operations to Walmart | $4.99 | $4.85 | $5.01 | $4.53 |

| Diluted income (loss) per common sharefrom discontinued operations | $0.06 | $0.03 | $0.01 | ($0.01) |

| Diluted net income per common share | $5.05 | $4.88 | $5.02 | $4.52 |

| Weighted-average number of commonshares: | ||||

| Basic | 3,230 | 3,269 | 3,374 | 3,460 |

| Diluted | 3,243 | 3,283 | 3,389 | 3,474 |

| Dividends declared per common share | $1.92 | $1.88 | $1.59 | $1.46 |

Fiscal Year Ended | 1/31/2015 | 1/31/2014 | 1/31/2013 | 1/31/2012 |

Adjusted Closing Price | $83.94 | $71.97 | $65.79 | $56.32 |

Common Shares Outstanding (millions) | 3,228 | 3,233 | 3,314 | 3,418 |