FIN 501 Study Guide - Libor, United States Treasury Security, Annual Percentage Rate

31 Jul 2012

School

Department

Course

Professor

Document Summary

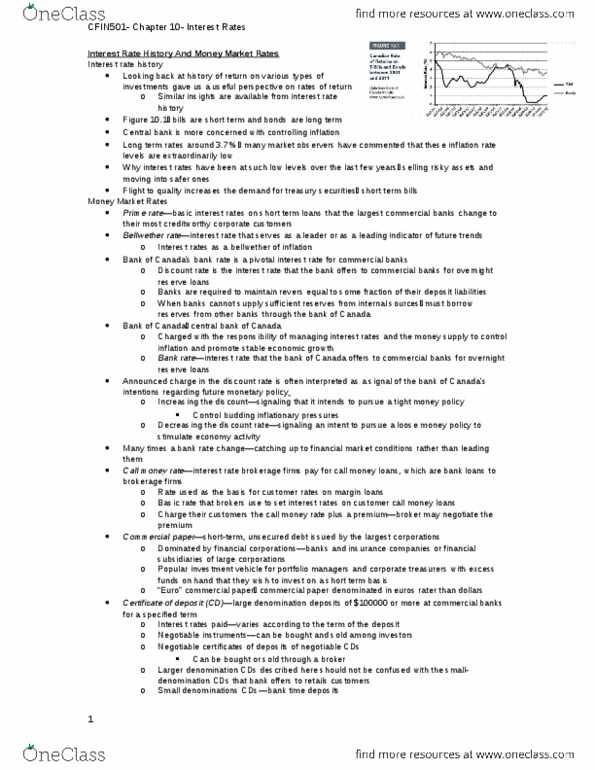

Prime rate: the basic interest rate on short-term loans that the largest commercial banks charge to their most creditworthy corporate customers. Rates are quoted as prime plus or minus a spread. Bellwether rate: interest rate that serves as a leader or as a leading indicator of future trends; interest rates as a bellwether of inflation. Bank rate: interest rate that the bank of canada offers to commercial banks for overnight-reserve loans: discount rate is the interest rate that the bank offers to commercial banks for overnight reserve loans. Increasing discount rate means bank may be signalling that it intends to pursue a tight-money policy, most likely to control budding inflationary pressures. Decreasing discount rate means bank may be signalling an intent to pursue a loose-money policy to stimulate economic activity. Call money rate: interest rate brokerage firms pay for call money loans, which are bank loans to brokerage firms.