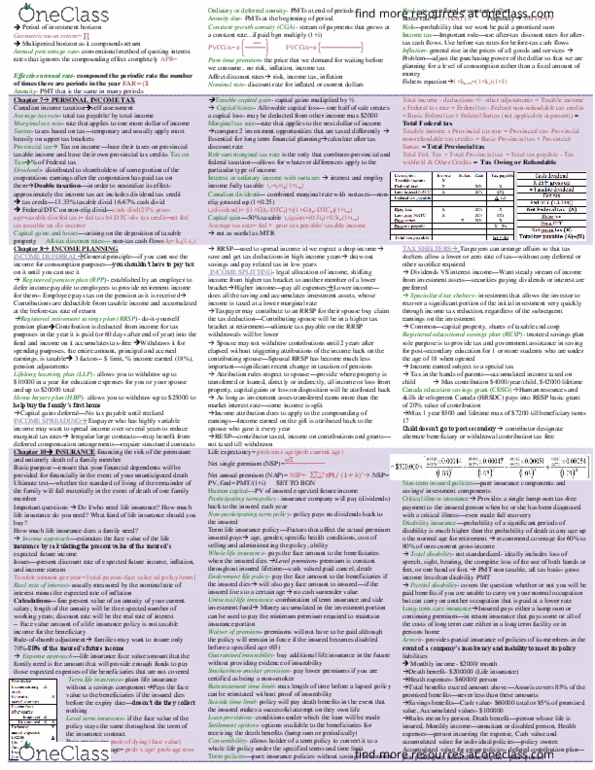

FIN 502 Study Guide - Final Guide: Tax Rate, Surtax, Tax Bracket

Document Summary

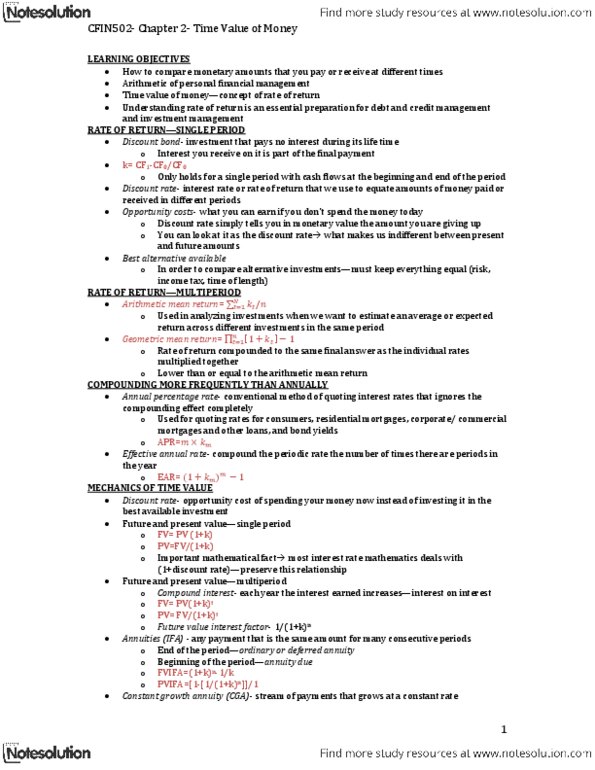

Annual percentage rate- conventional method of quoting interest rates that ignores the compounding effect completely apr= Effective annual rate- compound the periodic rate the number of times there are periods in the year ear= Annuity- pmt that is the same in many periods. Average tax rate- total tax payable/ by total income. Marginal tax rate- rate that applies to one more dollar of income. Surtax- taxes based on tax temporary and usually apply most heavily on upper tax brackets. Provincial tax tax on income base their taxes on provincial taxable income and have their own provincial tax credits tax on. Dividends- distributed to shareholders of some portion of the corporations earnings after the corporation has paid tax on them double taxation in order to neutralize its effect- approximately the income tax act includes dividend tax credit. Tax credit 13. 33% taxable divid 16. 67% cash divid.