FIN 502 Study Guide - Tax Rate, Dividend Tax, Tax Bracket

Document Summary

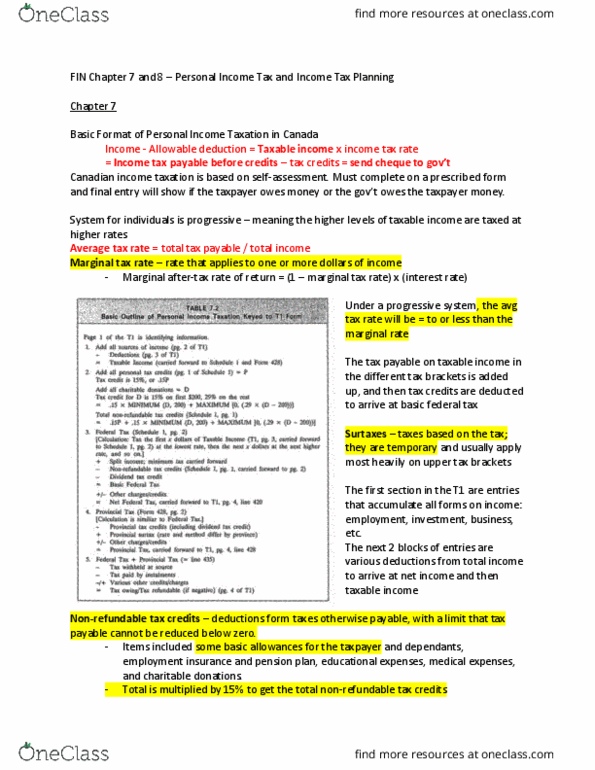

Income tax act - stature of parliament = law. Frequently diff parts affected by federal govt budget administered by canada rev agency (cra) General concepts of income taxation based on self assessment limited corp, trusts, indiv complete income tax return on prescribed forms legally responsible. Canadian taxed at system = progressive - higher levels of taxable income higher rates average rate marginal rate lower rate applies to all income up to specified level, above level . Marginal after tax rate of return you re/ = (1 - marginal tax rate)(interest rate) On amt over tax brackets - d/ whether to invest $ in term deposit surtaxes - taxes based on the tax temporary, apply heavily on upper tax bracket fin effect identical to basic tax rate. Basic outline of personal income taxation: add all sources of income. = taxable income (carried forward to schedule 1: add all personal tax credits = p.