BUS 321 Study Guide - Midterm Guide: Shares Outstanding, Stock Split, Conversion Marketing

23 Sep 2017

School

Department

Course

Professor

Document Summary

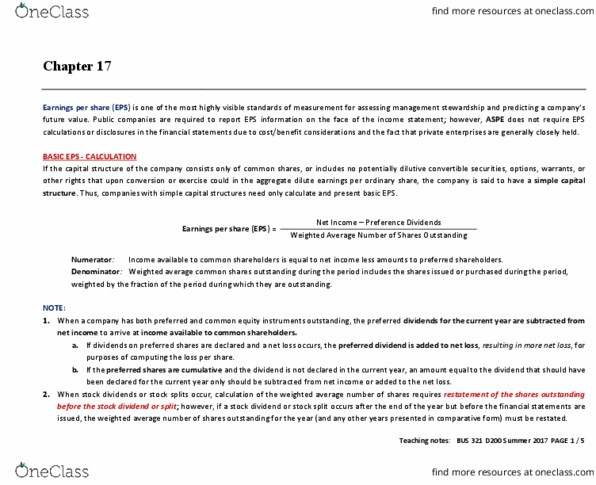

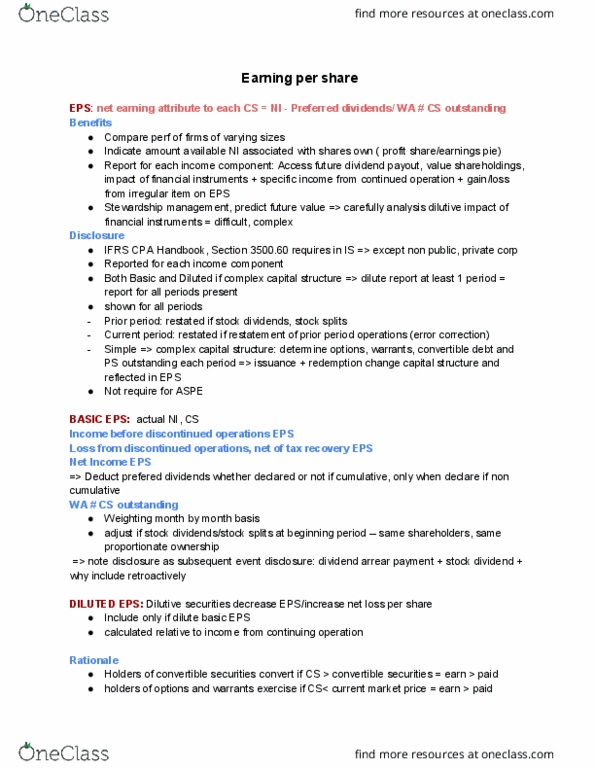

Chapter 17 c/s have residual interest in company: roi =/= based on predetermined int, time, fv, eps normally calc for only c/s. If divs on p/s declared & nl occurs, pref div added to the loss in calc loss per share. In reporting eps, divs declared on p/s should be subtracted from income from cont ops & ni: divs on p/s =/= deducted in calc eps from discount ops, cumulative cond: If p/s = non-cumulative, ded only declared divs. If p/s = cumulative, ded only declared di(cid:448)s or if (cid:374)o di(cid:448)s de(cid:272)la(cid:396)ed, dedu(cid:272)t 1 (cid:455)(cid:396)"s (cid:449)o(cid:396)th of di(cid:448)s. If stock div/split, all per share amts of prior period earnings should be restated using new wacs. If these shares are issuable simply w/passage of time, =/= considered contingent b/c time will pass: where they are issuable based on something else (e. g. performance targets), incl in calc of basic eps when cond satisfied.