BUS 329 Study Guide - Midterm Guide: Welfare, Life Insurance, Child Care

20 Sep 2017

School

Department

Course

Professor

Document Summary

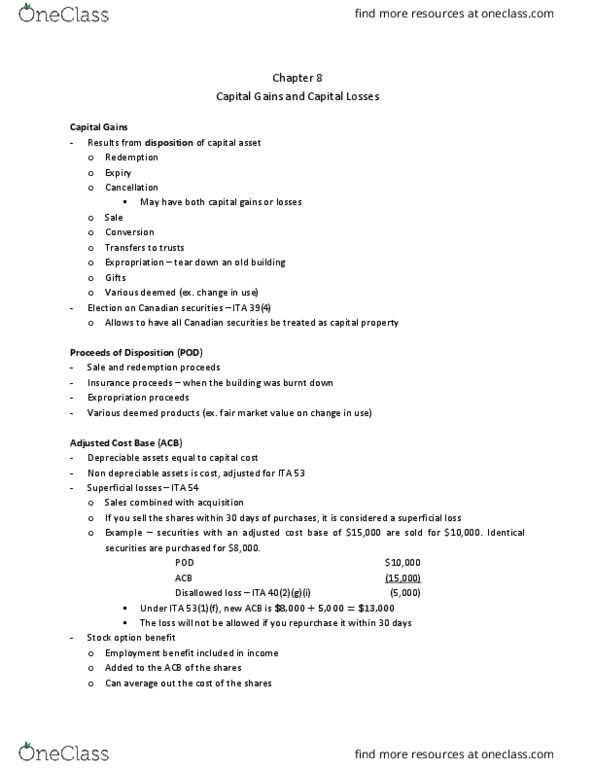

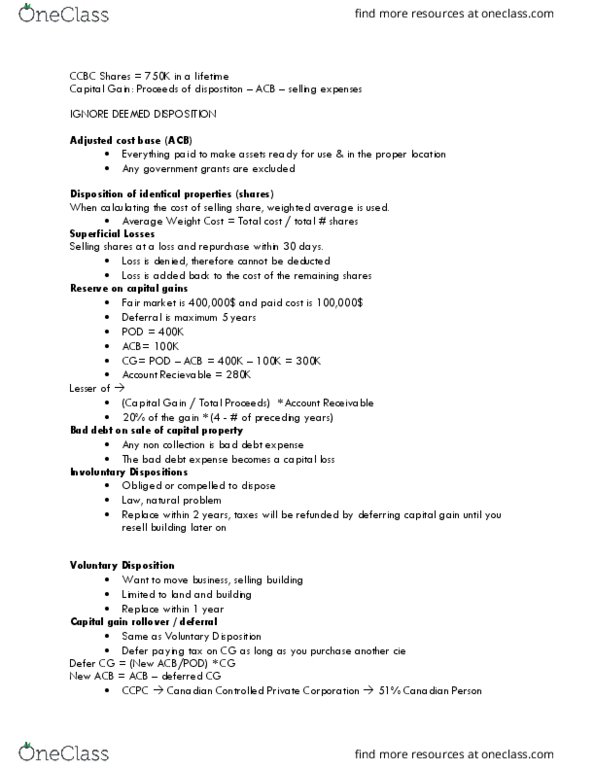

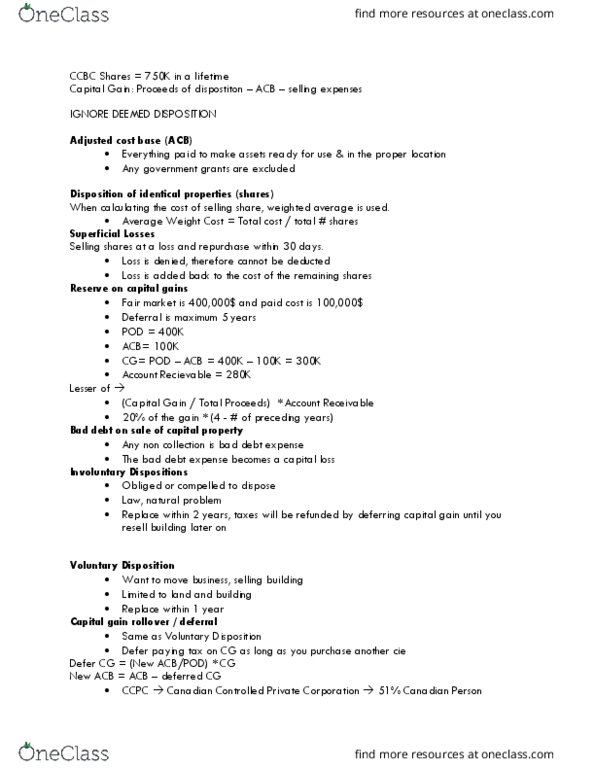

Cg intro/timeline: cg/cl a(cid:396)e due to ta(cid:454)pa(cid:455)e(cid:396)"s dispositio(cid:374) of (cid:272)ap that used to p(cid:396)odu(cid:272)e bus/property income, timeline, until 1972: no tax. Insurance proceeds: expropriation proceeds, various deemed proceeds fmv o(cid:374) i(cid:374) use, formula for cg or cl: @ nov 27, 2016 to jan 27, 2017: if purchase 100 shares @ /share, dec loss would be disallowed. @ dec 27, 2016: sell shares @ /share (market price) to offset cg dispose. Loss would be added to acb of the new shares substituted property. New shares acb = new share acquisition p + (old share acqui p sell p) If dispose part of property, portion of total acb must be allocated to disposition on reasonable basis: e. g. 200m2 of 500m2 sold, 500m2 has acb of 6,000,000. Allocate 2,400,000 (40% b/c 200/500) of 6,000,000 (total acb) to land sold. Limit of reserve to lesser of: reasonable amt.