BUS 251 Study Guide - Revenue Recognition, Trial Balance, Accounts Receivable

14 Dec 2012

School

Department

Course

Professor

Document Summary

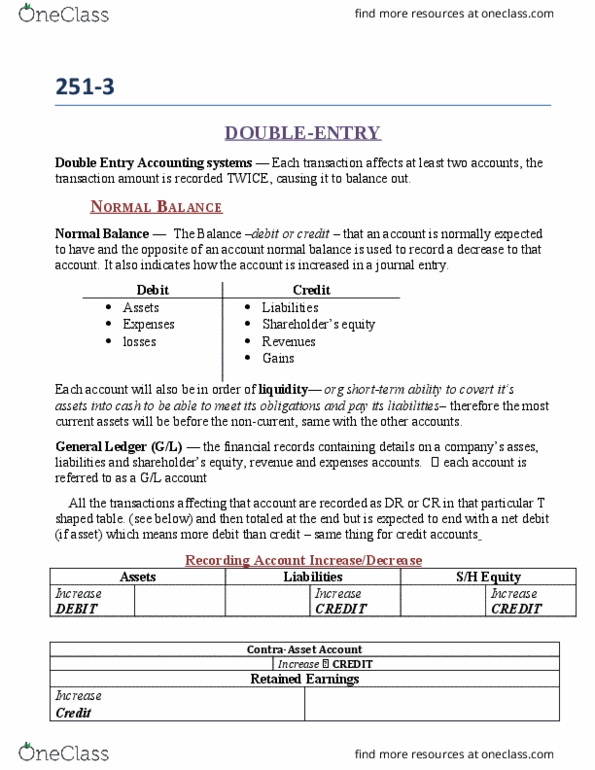

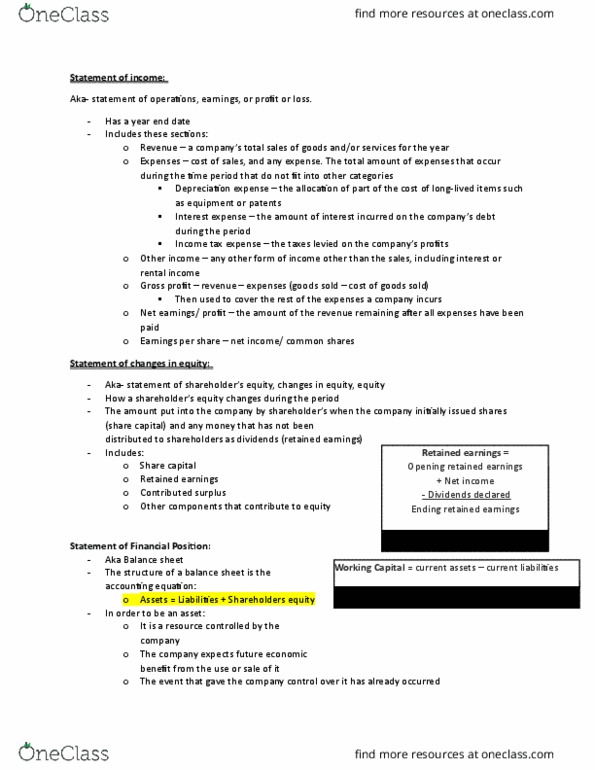

Financial statements are often part of the annual report which is prepared annually by the management of the business and made available to all owners of the business. Income statement: measures the performance (net income/profit/earnings) over a period of time. Sales/revenues: increases in the company"s wealth arising from providing goods or services to customers. Expenses: decreases in the company"s wealth incurred in order to earn revenues. Sales revenue cogs = gross margin. Balance sheet: measures a company"s position at a point in time. Describes the organizations resources and where they came from. Assets: resources over which the company already has in control, which will provide future economic benefits from the use. Liabilities: obligations that will have to be paid by the organization in the future. Includes share capital(increases when more shares are issued by the company) and retained earnings (increases when the company reports a profit and decreases when dividends are paid out)