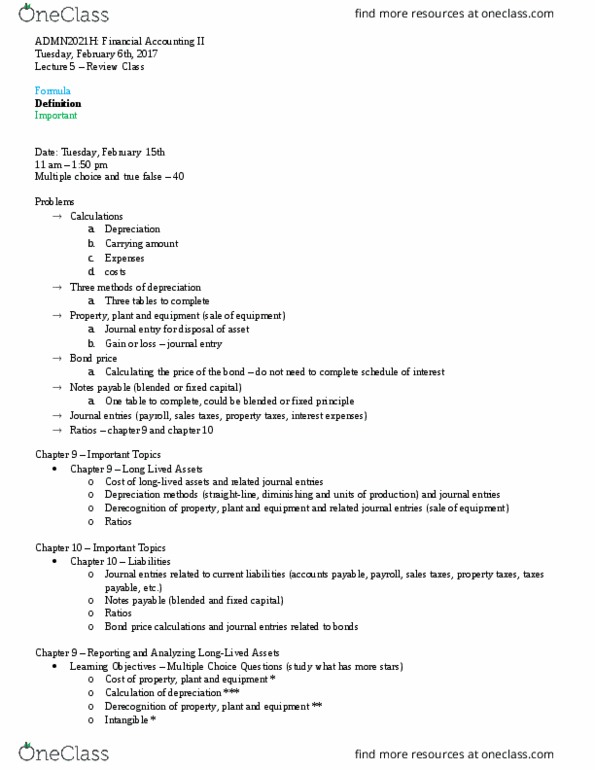

ADMN 2021H Study Guide - Midterm Guide: Qst, Title Search, Contingent Liability

28 Jun 2018

School

Department

Course

Professor

Definition

Example

Formula

Important

Problems (complete)

Calculations

a. Depreciation

b. Carrying amount

c. Expenses

d. costs

Three methods of depreciation

a. Three tables to complete

Property, plant and equipment (sale of equipment)

a. Journal entry for disposal of asset

b. Gain or loss – journal entry

Bond price

a. Calculating the price of the bond – do not need to complete schedule of interest

Notes payable (blended or fixed capital)

a. One table to complete, could be blended or fixed principle

Journal entries (payroll, sales taxes, property taxes, interest expenses)

Ratios – chapter 9 and chapter 10

Return on Assets

-Higher percentage means better return on assets

-Net income ÷ average total assets

-Higher is better

Asset Turnover Ratio

-Higher number of times turned over is better

-Net sales ÷ average total assets

oTo find average total assets, add then divide by 2 **

-Higher is better

Profit Margin

-Higher percentage means better profit margin

-Net income ÷ net sales

-Higher is better

-Divide percentage (return on assets) by decimal (asset turnover) to get profit margin

Journal entries

Understated or overstated accounts

Amortization journal entry

Statement of financial position Income statement

-Accumulated amortization – software (intangible assets)

-Accumulated depreciation – buildings (property, plant and

equipment)

-Accumulated depreciation – fixtures and equipment (property,

plant and equipment)

-Amortization expense (operating

expenses)

-Depreciation expense (operating

expenses)

-Impairment loss (operating expenses)

find more resources at oneclass.com

find more resources at oneclass.com

-Accumulated depreciation – leasehold improvements (property,

plant and equipment)

-Buildings (property, plant and equipment)

-Fixtures and equipment (property, plant and equipment)

-Goodwill (goodwill)

-Land (property, plant and equipment)

-Leasehold improvements (property, plant and equipment)

-Software – intangible assets (intangible assets)

-Trademarks (intangible assets)

-Operating leases (operating expenses)

-Reversal of impairment loss (operating

expenses)

Accounts that need to be debited in certain transactions

Cost of Land

-The purchase price

-Closing costs such as: title search, legal fees and survey costs

-Cost of clearing the land and removing unwanted buildings less any proceeds from salvaged materials

-Costs incurred to prepare the land for its intended use, such as clearing, draining, grading and filling

-Once the land is ready for its intended use, recurring costs, such as annual property taxes, and recorded as operating

expenditures

Land Improvements

-Driveways, fences, lighting, sidewalks, parking lots

-Land improvements are recorded separately from land and depreciated

Buildings

-Purchased:

oPurchase price, closing costs, costs needed to make the building ready for its intended use (remodeling),

replacing or repairing the roof, floors, electrical wiring and plumbing

-Being constructed:

oThe contract price, architects fees, building permits

oExcavation costs

oInternet costs incurred to finance a construction project, but limited to the construction period

Cost of Equipment

-Could be:

oDelivery equipment, office equipment, machinery, vehicles, furniture and fixtures and other similar assets

-The cost of the equipment should include:

oPurchase price, freight charges, insurance during transit, expenditures required in assembling, installing and

testing the unit

Straight-Line Method

-Depreciation is constant for each year of the assets useful life

-Cost – residual value = depreciable amount

-depreciable amount ÷ useful life in years = depreciation expense

-100% ÷ useful life in years = straight-line depreciation rate

example:

-cost = $33,000, residual value = $3,000, useful life = 5 years

-$33,000 – 3,000 = 30,000

-30,000 ÷ 5 = 6,000

-100% ÷ 5 = 20%

find more resources at oneclass.com

find more resources at oneclass.com

year Depreciable

amount

x depreciation rate = depreciation

expense

Accumulated

depreciation

Carrying amount

$33,000

2018 $30,000 20% $6,000 $6,000 27,000

2019 30,000 20% 6,000 12,000 21,000

2020 30,000 20% 6,000 18,000 15,000

2021 30,000 20% 6,000 24,000 9,000

2022 30,000 20% 6,000 30,000 3,000

= $30,000

Double-Diminishing Balance Method

-produces a decreasing annual depreciation expense over an assets useful life

-annual depreciation expense is calculated by multiplying the carrying amount by the depreciation rate

-100% ÷ useful life in years = depreciation rate

-depreciation rate = straight line rate x multiplier

omultiply deprecation rate by two for DOUBLE diminishing

-can be applied using different rates

-carrying amount at the beginning of the year x deprecation rate = depreciation expense

example:

-cost = $33,000, residual value = $3,000, useful life = 5 years

-100% ÷ 5 = 20%

-$33,000 x (20% x 2) = $13, 200

Year Carrying amount

at beginning of

year

x deprecation rate = deprecation

expense

Accumulated

deprecation

Carrying amount

$33,000

2018 $33,000 40% $13,200 $13,200 19,800

2019 19,800 40% 7,920 21,120 11,880

2020 11,880 40% 4,572 25,872 7,128

2021 7,128 40% 2,851 28,723 4,277

2022 4,277 40% 1,277 * 30,000 3,000

= $30,000

** adjusted to that the carrying amount will be equal to the residual value

Units-of-Production Method

-useful life is expressed in terms of total units of production or activity expected from the asset

-useful for factory machines, vehicles, airplanes

-cost – residual value = depreciable amount

-depreciable amount ÷ estimated total units of activity = depreciable amount per unit

-depreciable amount per unit x units of activity during that year = depreciation expense

example:

-cost = $33,000, residual value = $3,000, useful life = 5 years, useful life in kilometers = 100,000

-$33,000 – 3,000 = 30,000

-30,000 ÷ 100,000 = 0.30

-0.30 x 15,000 = 4,500

Year Units of

production

Depreciable

amount

Depreciation

expense

Accumulated

depreciation

Carrying amount

$33,000

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Calculations: depreciation, carrying amount, expenses, costs. Three methods of depreciation: three tables to complete. Property, plant and equipment (sale of equipment) Journal entry for disposal of asset a: gain or loss journal entry. Bond price: calculating the price of the bond do not need to complete schedule of interest. Notes payable (blended or fixed capital: one table to complete, could be blended or fixed principle. Journal entries (payroll, sales taxes, property taxes, interest expenses) Ratios chapter 9 and chapter 10. Higher percentage means better return on assets. Higher number of times turned over is better. Net sales average total assets: to find average total assets, add then divide by 2 ** Divide percentage (return on assets) by decimal (asset turnover) to get profit margin. Accumulated depreciation buildings (property, plant and equipment) Accumulated depreciation fixtures and equipment (property, plant and equipment) Accumulated depreciation leasehold improvements (property, plant and equipment) Accounts that need to be debited in certain transactions.