BBUS 2541 Study Guide - Reduced Properties, Variable Cost

Document Summary

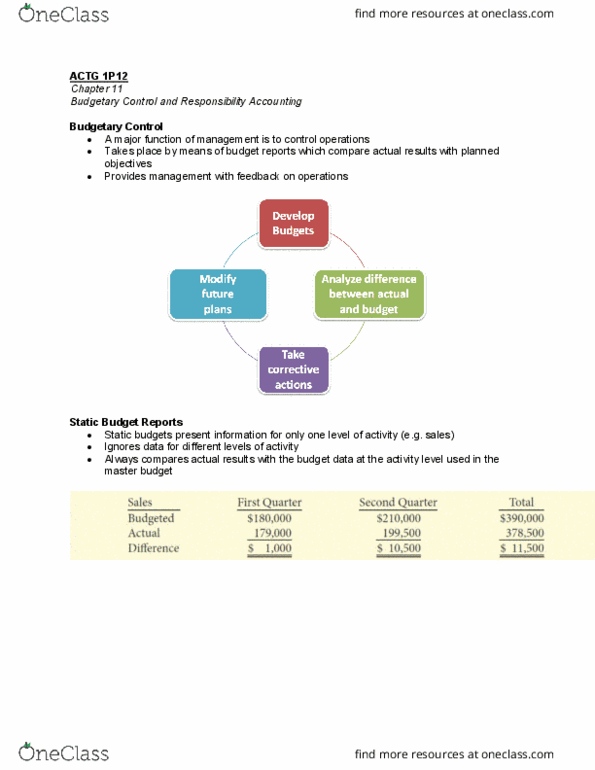

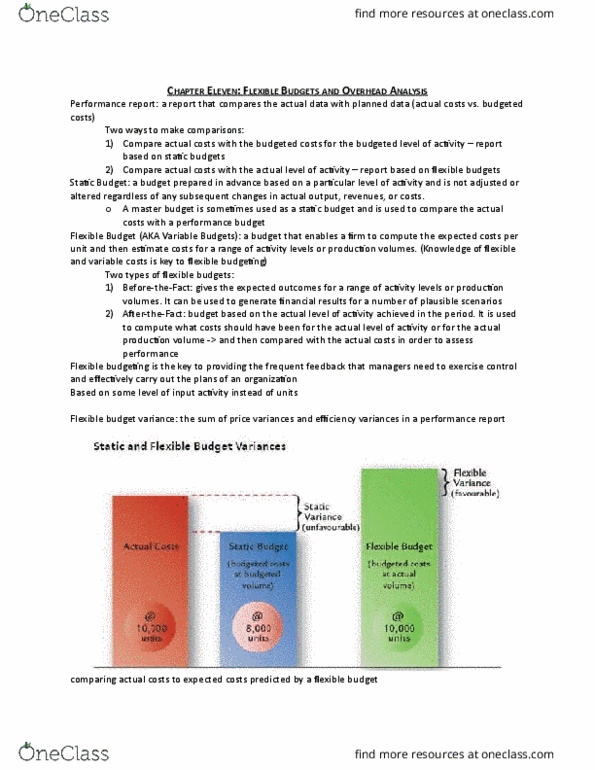

A static budget is based on a single expected activity level. In contrast, a flexible budget reflects data for several activity levels. Given the focus on a range of activity, a flexible budget would be more useful because it incorporates several different activity levels. Direct material used: ,880,000 72,000 units = . 00 per unit. Direct labour: ,000 72,000 units = . 00 per unit. Variable manufacturing overhead: ,000 72,000 units = . 50 per unit. Depreciation: ,000 3 months = ,000 per month. Supervisory salaries: ,000 3 months = ,000 per month. Other fixed manufacturing overhead: (,800,000 - ,000 - ,000) 3 months = ,000 per month. A performance report based on flexible budgeting is preferred. The report compares budgeted and actual performance at the same volume level, eliminating any variations in activity. In essence, everything is placed on a level playing field. The general manager"s warning is appropriate because of the sizable variances that have arisen.