ACCT 323 Study Guide - Midterm Guide: Fixed Cost, Finished Good, Cost Driver

28 Oct 2016

School

Department

Course

Professor

Document Summary

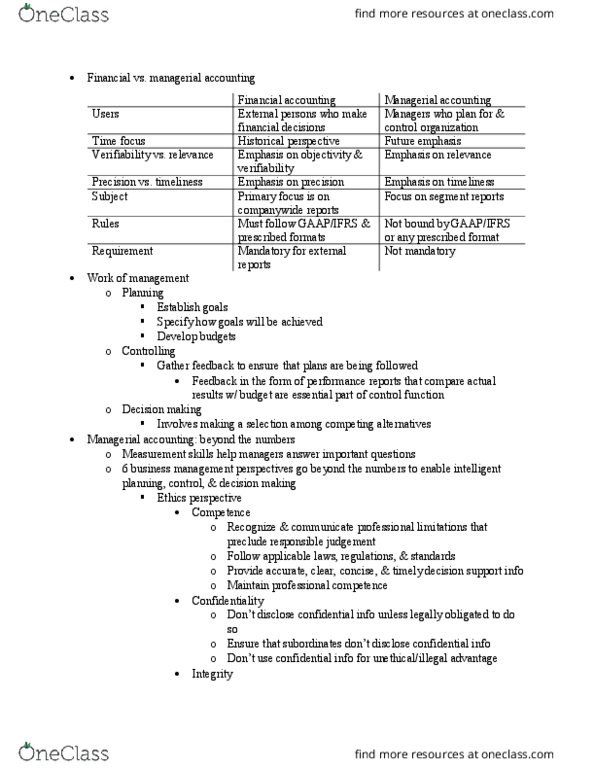

Chapter 1 - managerial accounting and management decisions. Role of managerial accounting: assists managers by providing relevant info to improve decision making. Chapter 2 - cost terms, concepts and classifications. Manufacturing costs - divided into direct materials, direct labour and manufacturing overhead. Direct materials: materials that become an integral part of the finished product and can be conveniently traced to it. Note - raw materials are any materials used in the final product; a finished product can be raw material for another product; raw materials can be both direct or indirect materials. Direct labour: factory labour costs that can be conveniently traced to individual units of product. Manufacturing overhead - all costs associated with manufacturing, except direct materials and direct labour. Indirect materials: small items of materials used in a finished product; cost of tracing exceeds benefits. Indirect labour: labour costs of janitors, supervisors, materials handlers and other factor workers that cannot be conveniently traced to individual units of product.