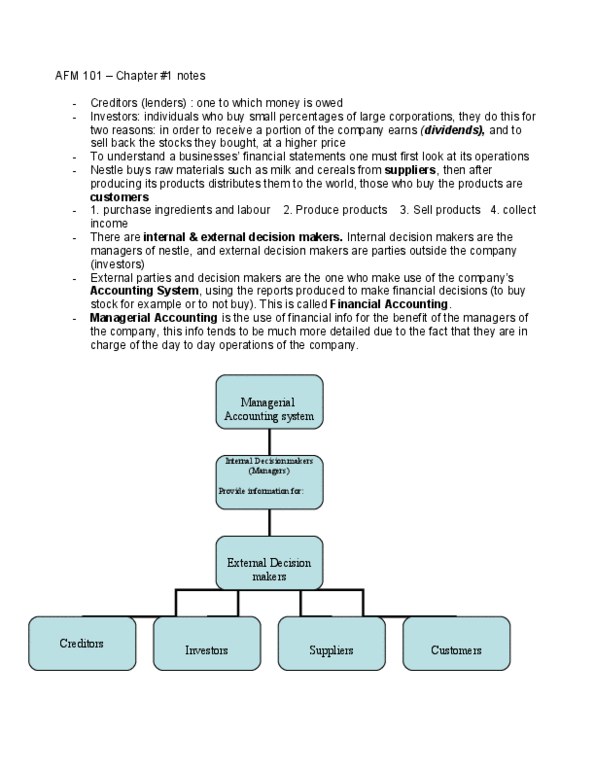

AFM101 Study Guide - Final Guide: Cash Flow Statement, Cash Cash, Retained Earnings

Get access

Related Documents

Related Questions

FSU Manufacturing, Inc. has the following financial statements data for 2014:

| Income Statement | Balance Sheet | |||

| Sales | $102,500 | Cash | $40,000 | |

| Cost of Goods | $50,000 | Fixed Assets | $55,000 | |

| SG&E Expenses | $35,000 | Total Assets | $95,000 | |

| EBIT | $17,500 | Accounts Payable | $12,000 | |

| Interest Expense | $2,500 | Long-term Debt | $25,000 | |

| Taxes | $6,000 | Retained Earnings | $28,000 | |

| Net Income | $9,000 | Paid-in Common Equity | $30,000 |

| Trait 1 | Use of financial statements | ||

| 1. | |||

| a. | Compute the firmâs debt ratio and current ratio. | ||

| b. | Is the firm profitable? Does the balance sheet balance? Explain. | ||

| c. | If the firm paid $5,000 in dividends in 2014, what was its retained earnings balance at the end of 2013? (20 points) | ||

| Trait 2 | Student relates financial ratios to improved business decisions | ||

| 2. | |||

| a. | Compute the firmâs net profit margin, total asset turnover, and financial leverage multiplier (also known as the equity multiplier). | ||

| b. | Explain what each of the three ratios above tells you about the firmâs performance and how they combine to form the firmâs return on equity. | ||

| c. | The financial data for the firmâs major competitors show on average a net profit margin of 16%, total asset turnover of 1.25, but comparable leverage. Identify some possible business decisions that the firm could make so that it would be as attractive an investment as its competitors. | ||

| Selectedcomparative financial statements of Haroun Company follow. |

| HAROUN COMPANY | ||||||||||||||||||||||||||||

| Comparative Income Statements | ||||||||||||||||||||||||||||

| For Years Ended December 31, 2015â2009 | ||||||||||||||||||||||||||||

| ($thousands) | 2015 | 2014 | 2013 | 2012 | 2011 | 2010 | 2009 | |||||||||||||||||||||

| Sales | $ | 2,287 | $ | 2,003 | $ | 1,822 | $ | 1,670 | $ | 1,559 | $ | 1,449 | $ | 1,188 | ||||||||||||||

| Costof goods sold | 1,644 | 1,337 | 1,150 | 1,006 | 935 | 875 | 697 | |||||||||||||||||||||

| Gross profit | 643 | 666 | 672 | 664 | 624 | 574 | 491 | |||||||||||||||||||||

| Operating expenses | 489 | 382 | 351 | 259 | 224 | 221 | 184 | |||||||||||||||||||||

| Netincome | $ | 154 | $ | 284 | $ | 321 | $ | 405 | $ | 400 | $ | 353 | $ | 307 | ||||||||||||||

HAROUN COMPANY | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Comparative Balance Sheets | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

December 31, 2015â2009 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

($ thousands) | 2015 | 2014 | 2013 | 2012 | 2011 | 2010 | 2009 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Assets | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Cash | $ | 152 | $ | 201 | $ | 209 | $ | 213 | $ | 222 | $ | 219 | $ | 226 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Accounts receivable, net | 1,093 | 1,148 | 1,039 | 797 | 702 | 665 | 469 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Merchandise inventory | 3,954 | 2,879 | 2,515 | 2,119 | 1,904 | 1,617 | 1,173 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Other current assets | 101 | 91 | 56 | 101 | 85 | 86 | 45 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Long-term investments | 0 | 0 | 0 | 312 | 312 | 312 | 312 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Plant assets, net | 4,839 | 4,820 | 4,217 | 2,378 | 2,458 | 2,185 | 1,875 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Total assets | $ | 10,139 | $ | 9,139 | $ | 8,036 | $ | 5,920 | $ | 5,683 | $ | 5,084 | $ | 4,100 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Liabilities and Equity | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Current liabilities | $ | 2,549 | $ | 2,144 | $ | 1,406 | $ | 1,170 | $ | 1,015 | $ | 960 | $ | 619 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Long-term liabilities | 2,725 | 2,374 | 2,310 | 1,072 | 1,096 | 1,186 | 890 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Common stock | 1,845 | 1,845 | 1,845 | 1,640 | 1,640 | 1,435 | 1,435 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Other paid-in capital | 461 | 461 | 461 | 410 | 410 | 359 | 359 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Retained earnings | 2,559 | 2,315 | 2,014 | 1,628 | 1,522 | 1,144 | 797 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Total liabilities and equity | $ | 10,139 | $ | 9,139 | $ | 8,036 | $ | 5,920 | $ | 5,683 | $ | 5,084 | $ | 4,100 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Complete the below table to calculate the trend percents for allcomponents of both statements using 2009 as the base year.(Round your percentage answers to 1 decimalplace.) **PLEASE FILL IN THE GRAPH DISPLAYED**â

**PLEASE FILL IN THE GRAPH DISPLAYED** | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Selectedcomparative financial statements of Haroun Company follow. |

| HAROUN COMPANY | ||||||||||||||||||||||||||||

| Comparative Income Statements | ||||||||||||||||||||||||||||

| For Years Ended December 31, 2015â2009 | ||||||||||||||||||||||||||||

| ($thousands) | 2015 | 2014 | 2013 | 2012 | 2011 | 2010 | 2009 | |||||||||||||||||||||

| Sales | $ | 2,287 | $ | 2,003 | $ | 1,822 | $ | 1,670 | $ | 1,559 | $ | 1,449 | $ | 1,188 | ||||||||||||||

| Costof goods sold | 1,644 | 1,337 | 1,150 | 1,006 | 935 | 875 | 697 | |||||||||||||||||||||

| Gross profit | 643 | 666 | 672 | 664 | 624 | 574 | 491 | |||||||||||||||||||||

| Operating expenses | 489 | 382 | 351 | 259 | 224 | 221 | 184 | |||||||||||||||||||||

| Netincome | $ | 154 | $ | 284 | $ | 321 | $ | 405 | $ | 400 | $ | 353 | $ | 307 | ||||||||||||||

HAROUN COMPANY | |||||||||||||||||||||

Comparative Balance Sheets | |||||||||||||||||||||

December 31, 2015â2009 | |||||||||||||||||||||

($ thousands) | 2015 | 2014 | 2013 | 2012 | 2011 | 2010 | 2009 | ||||||||||||||

Assets | |||||||||||||||||||||

Cash | $ | 152 | $ | 201 | $ | 209 | $ | 213 | $ | 222 | $ | 219 | $ | 226 | |||||||

Accounts receivable, net | 1,093 | 1,148 | 1,039 | 797 | 702 | 665 | 469 | ||||||||||||||

Merchandise inventory | 3,954 | 2,879 | 2,515 | 2,119 | 1,904 | 1,617 | 1,173 | ||||||||||||||

Other current assets | 101 | 91 | 56 | 101 | 85 | 86 | 45 | ||||||||||||||

Long-term investments | 0 | 0 | 0 | 312 | 312 | 312 | 312 | ||||||||||||||

Plant assets, net | 4,839 | 4,820 | 4,217 | 2,378 | 2,458 | 2,185 | 1,875 | ||||||||||||||

Total assets | $ | 10,139 | $ | 9,139 | $ | 8,036 | $ | 5,920 | $ | 5,683 | $ | 5,084 | $ | 4,100 | |||||||

Liabilities and Equity | |||||||||||||||||||||

Current liabilities | $ | 2,549 | $ | 2,144 | $ | 1,406 | $ | 1,170 | $ | 1,015 | $ | 960 | $ | 619 | |||||||

Long-term liabilities | 2,725 | 2,374 | 2,310 | 1,072 | 1,096 | 1,186 | 890 | ||||||||||||||

Common stock | 1,845 | 1,845 | 1,845 | 1,640 | 1,640 | 1,435 | 1,435 | ||||||||||||||

Other paid-in capital | 461 | 461 | 461 | 410 | 410 | 359 | 359 | ||||||||||||||

Retained earnings | 2,559 | 2,315 | 2,014 | 1,628 | 1,522 | 1,144 | 797 | ||||||||||||||

Total liabilities and equity | $ | 10,139 | $ | 9,139 | $ | 8,036 | $ | 5,920 | $ | 5,683 | $ | 5,084 | $ | 4,100 | |||||||

Complete the below table to calculate the trend percents for allcomponents of both statements using 2009 as the base year.(Round your percentage answers to 1 decimalplace.)

**PLEASE FILL IN THE GRAPH DISPLAYED**â

| Haroun Company | ||||||||||||||

| Income Statement Trends | ||||||||||||||

| For Years Ended December 31, 2015 | ||||||||||||||

| 2015 | 2014 | 2013 | 2012 | 2011 | 2010 | 2009 | ||||||||

| Sales | % | % | % | % | % | % | 100.0 | % | ||||||

| Cost of goods sold | 100.0 | |||||||||||||

| Gross profit | 100.0 | |||||||||||||

| Operating expenses | 100.0 | |||||||||||||

| Net income | % | % | % | % | % | % | 100.0 | % |

| Haroun Company | ||||||||||||||

| Balance Sheet Trends | ||||||||||||||

| December 31, 2015-2009 | ||||||||||||||

| 2015 | 2014 | 2013 | 2012 | 2011 | 2010 | 2009 | ||||||||

| Assets | ||||||||||||||

| Cash | % | % | % | % | % | %â | 100.0 | % | ||||||

| Accounts receivable, net | 100.0 | |||||||||||||

| Merchandise inventory | 100.0 | |||||||||||||

| Other current assets | 100.0 | |||||||||||||

| long-term investments | 100.0 | |||||||||||||

| Plant assets, net | 100.0 | |||||||||||||

| Total assets | % | % | % | % | % | % | 100.0 | % | ||||||

| Liabilities and Equity | ||||||||||||||

| Current Liablities | % | % | % | % | % | % | 100.0 | % | ||||||

| Long-term Liabilites | 100.0 | |||||||||||||

| Common Stock | 100.0 | |||||||||||||

| Other paid-in capital | 100.0 | |||||||||||||

| Retained earnings | 100.0 | |||||||||||||

| Total liabilites & equity | % | % | % | % | % | % | 100.0 | % |

**PLEASE FILL IN THE GRAPH DISPLAYED**