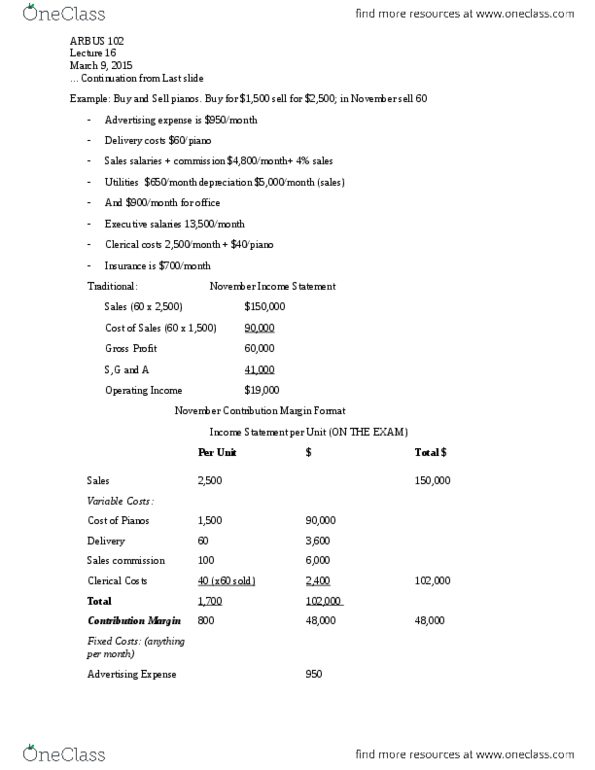

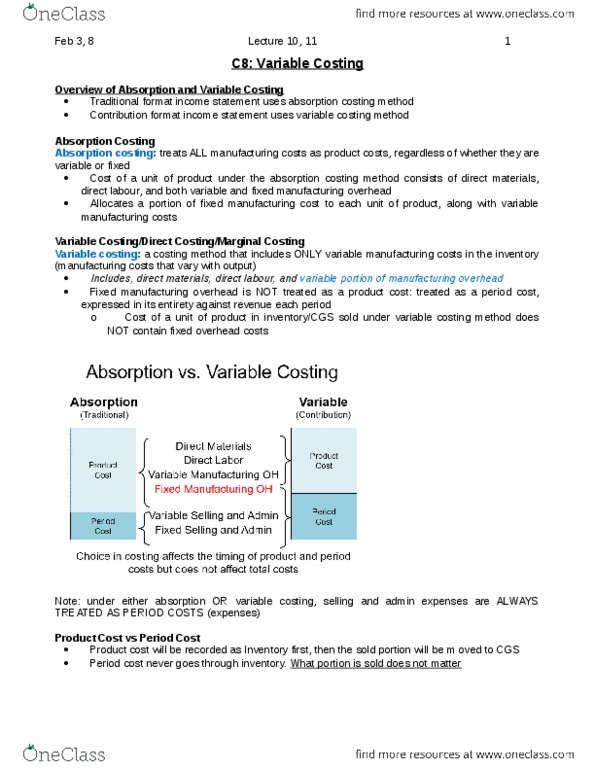

AFM102 Study Guide - Final Guide: Business Opportunity, Contribution Margin, Earnings Before Interest And Taxes

Document Summary

Get access

Related Documents

Related Questions

The Hampshire Company manufactures umbrellas that sell for$12.50 each. In 2014, the company made and sold 60,000 umbrellas.The company had fixed manufacturing costs of $216,000. It also hadfixed costs for administration of $79,525. The per-unit costs ofeach umbrella are as follows:

Direct Materials: $3.00

Direct Labor: $1.50

Variable Manufacturing Overhead: $0.40

Variable Selling Expenses: $1.10

Using the information above, perform a cost-volume-profit (CVP)analysis by completing the steps below.

1. Compute net income before tax.

2. Compute the unit contribution margin in dollars and thecontribution margin ratio for one umbrella.

3. Calculate the break-even point in units and dollars ofrevenue.

4. Calculate the margin of safety:

In units

In sales dollars

As a percentage

5. Calculate the degree of operating leverage.

6. Assume that sales will increase by 20% in 2015. Calculate thepercentage of before-tax income for this increase. Providecalculations to prove that your percentage increase is correctbased on the operating leverage calculated in step 5.

7. Compute the number of umbrellas that Hampshire is required tosell if it plans to earn $150,000 in income before taxes by usingthe target income formula. Proof your calculation.

8. A company that specializes in tours in England has offered topurchase 5,000 umbrellas at $11 each from Hampshire. The variableselling costs of these additional units will be $1.30 as opposed to$1.10 per unit. Also, this production activity will incur another$15,000 of fixed administrative costs. Should Hampshire agree tosell these additional 5,000 umbrellas to the touring business?Provide calculations to support your decision.

| Requirement 1 | ||||

| Units | Price | Totals | ||

| Sales | X | $ | $ | |

| Variable Costs | X | $ | $ | |

| Fixed Costs | $ | |||

| Net Income | $ | |||

| Requirement 2 | ||||

| Contribution Margin per Unitin Dollars = Selling Price â Variable Costs | ||||

| Selling Price | Variable Costs | Contribution Margin per Unit | ||

| Contribution Margin Ratio =Contribution Margin/Selling Price | ||||

| Contribution Margin | Selling Price | Contribution Margin Ratio | ||

| Requirement 3 | ||||

| Break-Even Point = Fixed Costs/ Contribution Margin | ||||

| Fixed Costs | Contribution Margin | Break-Even Point in Units (Rounded) | ||

| Break-Even Point in Units XSelling Price per Unit = Break-Even Point Sales | ||||

| Break-Even Point in Units | Selling Price per Unit | Break-Even Point in Sales (Rounded) | ||

| Requirement 4A | ||||

| Margin of Safety in Units =Current Unit Sales â Break-Even Point in Unit Sales | ||||

| Current Unit Sales | Break-Even Point in Sales | Margin of Safety in Units | ||

| Requirement 4B | ||||

| Margin of Safety in Dollars =Current Sales in Dollars â Break-Even Point Sales in Dollars | ||||

| Current Sales in Dollars | Break-Even Point in Dollars | Margin of Safety in Dollars | ||

| Requirement 4C | ||||

| Margin of Safety as aPercentage = Margin of Sales in Units / Current Unit Sales | ||||

| Margin of Safety in Units | Current Unit Sales | Margin of Safety Percentage | ||

| Requirement 5 | ||||

| Degree of Operating Leverage =Contribution Margin / Operating Income | ||||

| Contribution Margin | Operating Income | Operating Leverage | ||

| Requirement 6 | ||||

| Units | $ Per Unit | Totals | ||

| Sales | X | $ | $ | |

| Variable Costs | X | $ | $ | |

| Fixed Costs | $ | |||

| Net Income | $ | |||

| Operating Leverage | Times % Increase | Increase would be XX% | ||

| Prior Income | $ | From Part 1 | ||

| Increase | $ | Prior Income X XX% Above | ||

| Total | $ | |||

| Requirement 7 | ||||

| Targeted Income = (Fixed Costs+ Target Income) / Contribution Margin | ||||

| Fixed Costs + Target Income | Divided by Contribution Margin | # of Units (Rounded) | ||

| Fixed Costs | $ | |||

| Target Income | $ | |||

| Total | $ | $ | X | |

| # of Units Above X $ Per Unit | ||||

| Proof | Revenue | XX,XXX X $XX.XX | $ | |

| Variable Costs | XX,XXX X $X.XX | $ | ||

| Contribution Margin | $ | |||

| Fixed Costs | $ | |||

| Net Income | $ | |||

| Requirement 8 | ||||

| Sales Mix | ||||

| Current | Specialty | Total | ||

| Expected Sales Units | X | X | ||

| Revenue = Sales X Price | $ | $ | $ | |

| Variable Costs X Units | $ | $ | $ | |

| Contribution Margin | $ | $ | $ | |

| Fixed Costs | $ | $ | $ | |

| Operating Income | $ | |||

| Prior Net Income FromRequirement 1 | $ | |||

| Additional Operating Income | (Operating Income Above Less Prior Income) | $ | ||

| Decision With Explanation | ||||

Financial and Managerial Accounting, 13th Edition Carl S.Warren, James M. Reeve, Jonathan E. Duchac

Contribution Margin and Contribution Margin Ratio

For a recent year, McDonald's company-owned restaurants had thefollowing sales and expenses (in millions):

| Sales | $18,602.5 |

| Food and packaging | $ 6,318.2 |

| Payroll | 4,710.3 |

| Occupancy (rent, depreciation, etc.) | 4,195.2 |

| General, selling, and administrative expenses | 2,445.2 |

| 17,668.9 | |

| Income from operations | $ 933.6 |

Assume that the variable costs consist of food and packaging,payroll, and 40% of the general, selling, and administrativeexpenses.

a. What is McDonald's contribution margin?Round to the nearest tenth of a million (one decimal place).

$ million

b. What is McDonald's contribution marginratio? Round to one decimal place.

%

c. How much would income from operationsincrease if same-store sales increased by $900 million for thecoming year, with no change in the contribution margin ratio orfixed costs? Round your answer to the nearest tenth of a million(one decimal place).

$ million

2.

Break-Even Sales and Sales to Realize Income from Operations

For the current year ended March 31, Benatar Company expectsfixed costs of $1,250,000, a unit variable cost of $100, and a unitselling price of $140.

a. Compute the anticipated break-even sales(units).

units

b. Compute the sales (units) required torealize income from operations of $150,000.

units

Feedback

a. Fixed costs divided by the unit contribution margin equalsbreak-even point in units.

b. (Fixed costs + Target profit) divided by unit contributionmargin = sales units.

Learning Objective 3.

3.

Beck Inc. and Bryant Inc. have the following operating data:

| Beck Inc. | Bryant Inc. | |||

| Sales | $1,250,000 | $2,000,000 | ||

| Variable costs | 750,000 | 1,250,000 | ||

| Contribution margin | $500,000 | $750,000 | ||

| Fixed costs | 400,000 | 450,000 | ||

| Income from operations | $100,000 | $300,000 | ||

a. Compute the operating leverage for Beck Inc.and Bryant Inc. If required, round to one decimal place.

| Beck Inc. | |

| Bryant Inc. |

b. How much would income from operationsincrease for each company if the sales of each increased by 20%? Ifrequired, round answers to nearest whole number.

| Dollars | Percentage | |

| Beck Inc. | $ | % |

| Bryant Inc. | $ | % |

c. The difference in the of income fromoperations is due to the difference in the operating leverages.Beck Inc.'s operating leverage means that its fixed costs are apercentage of contribution margin than are Bryant Inc.'s.

1. Robbieâs Ribs has the following sales and costinformation:

Average number of pounds sold per year - 39,750

Average selling price per pound of ribs - $11.50

Variable expenses per pound:

Raw material - $3.70

Variable labor and overhead - $3.20

Annual fixed costs:

Production expenses - $37,300

Selling & Administrative expenses $15,186

The companyâs tax rate is 30%. The companyâs costs have slowlybeen rising and profits rapidly falling. Robbie Shaw, companypresident, has asked your help in answering the followingquestions:

What is the contribution margin per pound of ribs? Thecontribution margin ratio?

What is the break-even point in pounds of ribs? In dollars?

How much revenue must be generated to produce $39,749 of pretaxincome? How many pounds of ribs would this level of revenuerepresent?

How much revenue must be generated to produce $24,500 after-taxincome? How many pounds of ribs would this represent?

2. The following is financial information relative to twocompanies in the same industry:

| Category | Alpha | Omega |

|---|---|---|

| Sales | $10,000,000 | $10,000,000 |

| Variable Cost | 5,000,000 | 2,000,000 |

| Contribution Margin | 5,000,000 | 8,000,000 |

| Fixed Costs | 3,000,000 | 6,000,000 |

| Operating Income | $2,000,000 | $2,000,000 |

Calculate the operating leverage for each firm.

If sales increased 10% for each firm, the variable cost per unitdid not change, and the fixed costs did not change, what would bethe change in operating income?

If sales decreased 20% for each firm, the variable cost per unitdid not change, and the fixed costs did not change, what would bethe change in operating income?

Discuss the nuances of operating leverage and its relation torisk.

3. WaterSports USA sells three types of wake boards. Informationrelative to sales in units and dollars are given in the tablebelow:

| Sales Category | Wakeman | Jumper | Novice | Total |

|---|---|---|---|---|

| Sales in Units | 1,000 | 5,000 | 2,000 | 8,000 |

| Price per Unit | $200 | $150 | $100 | |

| Variable cost per Unit | $150 | $100 | $50 |

Fixed costs are projected to be $100,000. Carry all calculationsto four decimal places.

Compute the contribution margin per unit.

Compute the weighted contribution margin.

Compute the break-even in total units.

Compute the break-even per product.

Discuss briefly the usefulness of the computation in thebusiness world.