AFM 461 Study Guide - Midterm Guide: Foreign Tax Credit, Tax Credit, Dividend Tax

29 Mar 2014

School

Department

Course

Professor

Document Summary

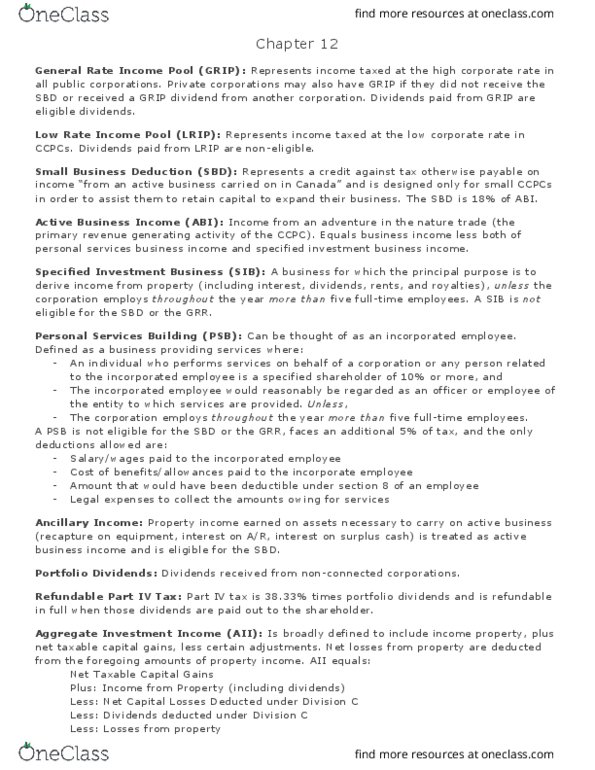

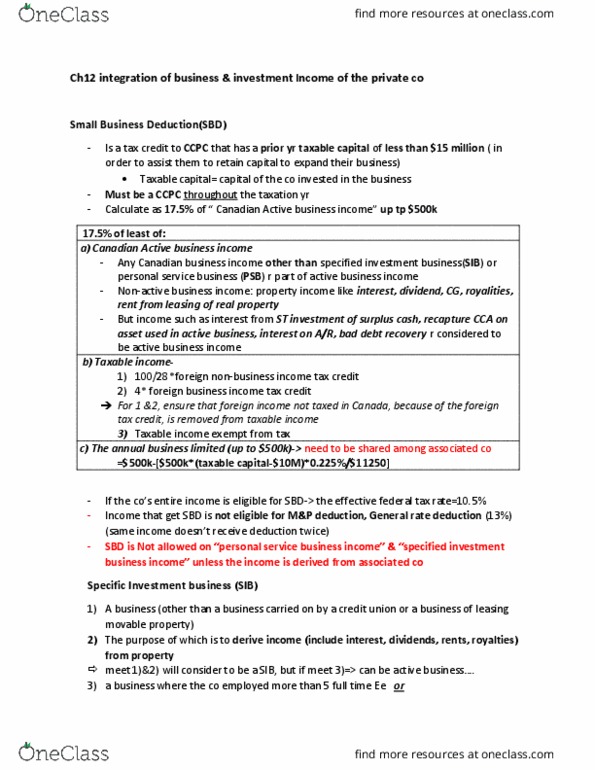

Federal abatement (10% of canadian sourced income) ------------------------ (xxxx) The amount of income eligible for the manufacturing and processing profits deduction: d is the corporation"s or the associated group"s, total taxable capital employed in canada for its preceding taxation year. The amount of income eligible for the small business deduction. Dividend refund (on dividends received from non-connected corp, 33%) ----- (xxxx) for every in taxable capital in excess of 10 million. Canada: 60% of the salary base of employees directly engaged in sr&ed, exception is with specified employee (an individual, together with the shares of the related individual, owns more than 10%) Lesser of: of their full salary, 2. 5 times the year"s maximum pensionable earnings for cpp purposes (51,100 for 2013) Step 1: calculate refundable dividend tax on hand. Step 2: calculate part iv tax on taxable dividends received (at 1/3%) Refundable dividend tax at end of the year: