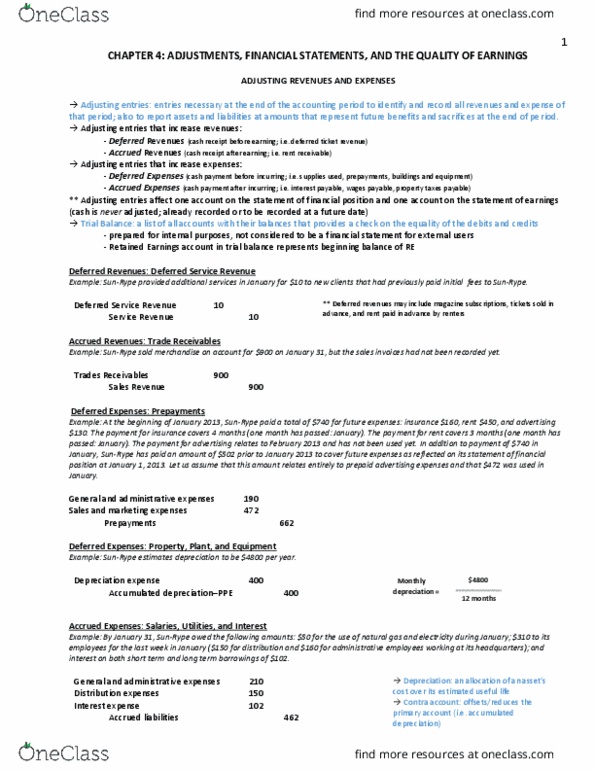

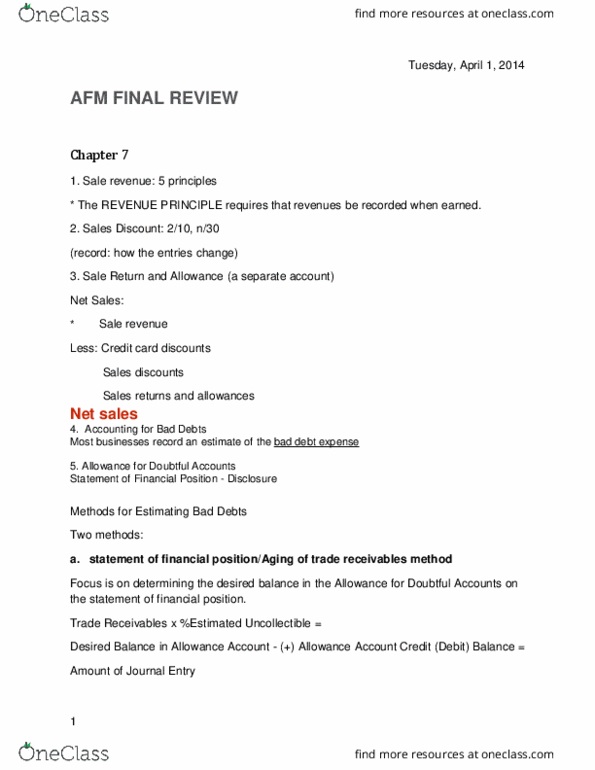

AFM101 Midterm: Midterm Solution v3.0.pdf

Get access

Related Documents

Related Questions

The following selected transactions were completed by Fasteners Inc. Co., a supplier of buttons and zippers for clothing:

| 20Y3 | ||

| Nov. | 21 | Received from McKenna Outer Wear Co., on account, a $54,000, 60-day, 7% note dated November 21 in settlement of a past due account. |

| Dec. | 31 | Recorded an adjusting entry for accrued interest on the note of November 21. |

| 20Y4 | ||

| Jan. | 20 | Received payment of note and interest from McKenna Outer Wear Co. |

Journalize the entries to record the transactions. If no entry is required, simply skip to the next transaction. Refer to the Chart of Accounts for exact wording of account titles. Assume a 360-day year when calculating interest. Round answers to the nearest dollar amount.

| CHART OF ACCOUNTS | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Fasteners Inc. Co. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| General Ledger | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

On January 1 of Year 1, Bryson Company obtained a $197,000, four-year, 5% installment note from Campbell Bank. The note requires annual payments of $55,556, beginning on December 31 of Year 1.

Required:

| a. Prepare a table for this installment note, similar to the one presented in Exhibit 4 . | |

| b. Journalize the entries for the issuance of the note and the four annual note payments. Refer to the Chart of Accounts for exact wording of account titles. | |

| c. Describe how the annual note payment would be reported on the Year 1 income statement. |

Chart of Accounts

| CHART OF ACCOUNTS | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Bryson Company | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| General Ledger | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Amortization Table

Shaded cells have feedback.

a. Prepare a table for this installment note, similar to the one presented in

Exhibit 4

. Round amounts to the nearest dollar.

| Amortization of Installment Notes | |||||

| A | B | C | D | E | |

| For the Year Ending Dec. 31 | January 1 Carrying Amount | Note Payment | Interest Expense | Decrease in Notes Payable | Dec. 31 Carrying Amount |

| Year 1 | |||||

| Year 2 | |||||

| Year 3 | |||||

| Year 4 | |||||

Points:

20 / 23

Feedback

Check My Worka. Review

Exhibit 4

in the text. The cash payment is the same in each year. The interest and principal repayment, however, change each year. This is because the carrying amount (book value) of the note decreases each year as principal is repaid, which decreases the interest.

After the final payment, the carrying amount on the note is zero, indicating that the note has been paid in full.

Journal

Shaded cells have feedback.

b. Journalize the entries for the issuance of the note and the four annual note payments. Enter transactions for Year 1 on page 10 of the journal, Year 2 on page 12, Year 3 on page 15, and Year 4 on page 17. Refer to the Chart of Accounts for exact wording of account titles.

Question not attempted.

PAGE 10

JOURNAL

ACCOUNTING EQUATION

Score: 0/63

| DATE | DESCRIPTION | POST. REF. | DEBIT | CREDIT | ASSETS | LIABILITIES | EQUITY | |

|---|---|---|---|---|---|---|---|---|

| 1 | ||||||||

| 2 | ||||||||

| 3 | ||||||||

| 4 | ||||||||

| 5 |

Points:

0 / 12

Question not attempted.

PAGE 12

JOURNAL

ACCOUNTING EQUATION

Score: 0/37

| DATE | DESCRIPTION | POST. REF. | DEBIT | CREDIT | ASSETS | LIABILITIES | EQUITY | |

|---|---|---|---|---|---|---|---|---|

| 1 | ||||||||

| 2 | ||||||||

| 3 |

Points:

0 / 7

Question not attempted.

PAGE 15

JOURNAL

ACCOUNTING EQUATION

Score: 0/37

| DATE | DESCRIPTION | POST. REF. | DEBIT | CREDIT | ASSETS | LIABILITIES | EQUITY | |

|---|---|---|---|---|---|---|---|---|

| 1 | ||||||||

| 2 | ||||||||

| 3 |

| debit | credit | ||

| 100 | Cash | 54,339 | |

| 110 | Investment Securities--AFS | 72,000 | |

| 115 | ACCRUED INTEREST RECEIVABLE | 1000 | |

| 130 | Accounts Receivable | 48,607 | |

| 131 | Allowance for Doubtful Accounts | 3,022 | |

| 132 | Allowance for Sales Returns and Allowances | 972 | |

| 140 | Merchandise Inventory | 449,807 | |

| 150 | Prepaid Insurance | 7,434 | |

| 160 | Store Supplies | 2,700 | |

| 170 | Land | 285,820 | |

| 180 | Building | 476,895 | |

| 181 | Accumulated Depreciation: Building | 55,027 | |

| 182 | Office & Store Equipment | 163,941 | |

| 183 | Accumulated Depreciation: Office & Store Equipment | 54,763 | |

| 184 | Delivery Trucks | 198,545 | |

| 185 | Accumulated Depreciation: Delivery Trucks | 41,260 | |

| 200 | Accounts Payable | 51,274 | |

| 210 | FICA Taxes Payable | 5,406 | |

| 220 | FEDERAL INCOME TAX WITHHOLDING PAYABLE | 3,401 | |

| 230 | Unemployment Taxes Payable | 814 | |

| 240 | Union Dues Payable | 180 | |

| 250 | Salaries & Wages Payable | 37,085 | |

| 260 | accured utility payable | 506 | |

| 280 | Mortgage Payable | 200,000 | |

| 281 | Accrued Interest Payable | 667 | |

| 300 | Common Stock | 100,000 | |

| 301 | PIC in Excess of Par | 1,000,000 | |

| 350 | Retained Earnings | 85,937 | |

| 400 | Sales | 1,779,369 | |

| 401 | Sales Returns | 36,893 | |

| 402 | Sales Discounts | 12,027 | |

| 490 | INTEREST REVENUE | 1,000 | |

| 500 | Purchases | 0 | |

| 501 | Purchase Returns | 0 | |

| 502 | Purchase Discounts | 0 | |

| 520 | Freight In | 0 | |

| 550 | cost of goods sold | 1,157,524 | |

| 600 | Salaries & Wages Expense | 304,693 | 0 |

| 605 | Payroll Tax Expense | 41,573 | 0 |

| 610 | Advertising Expense | 11,874 | 0 |

| 620 | REPAIR EXPENSE | 1,700 | 0 |

| 630 | STORE SUPPLIES EXPENSE | 10,021 | 0 |

| 640 | Utilities Expense | 20,410 | 0 |

| 650 | INSURANCE EXPENSE | 6,034 | 0 |

| 660 | DEPRECIATION EXPENSE | 46,459 | 0 |

| 670 | DOUBTFUL ACCOUNTS EXPENSE | 928 | 0 |

| 800 | Interest Expense | 9,459 | 0 |

| Totals | 3,420,683 | 3,420,683 |

Prepare a balance sheet as of December 31, 2016.(Remember that part of the mortgage payable should be classified asa current liability and the remainder as a long termliability.)