ECON202 Study Guide - Final Guide: Aggregate Supply, Demand Curve, Consumption Function

16 Oct 2011

School

Department

Course

Professor

Document Summary

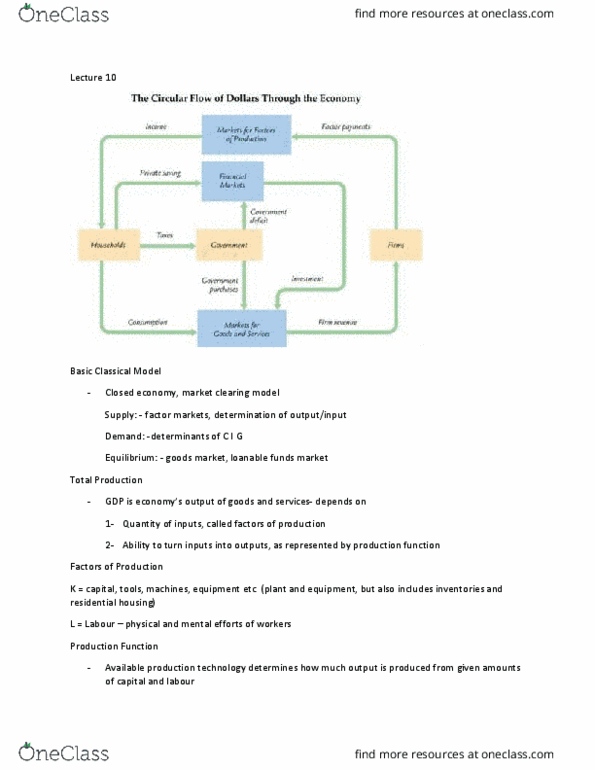

National income: where it comes from and where it goes. Supply side factor markets (supply, demand, price: determination of output/income. Demand side: determinants of c, i, and g. Equilibrium: goods market loanable funds market. K = capital: tools, machines, and structures used in production. L = labor: the physical and mental efforts of workers. Shows how much output (y ) the economy can produce from k units of capital and l units of labor reflects the economy"s level of technology, assume some level of technology. Initially y1 = f (k1 , l1 ) Scale all inputs by the same factor z: k2 = zk1 and l2 = zl1 (e. g. , if z = 1. 2, then all inputs are increased by 20%) If constant returns to scale, y2 = zy1. If increasing returns to scale, y2 > zy1. If decreasing returns to scale, y2 < zy1.