ECON 101 Final: Econ 101 - Microeconomics - All Chapters on Exam

78

ECON 101 Full Course Notes

Verified Note

78 documents

Document Summary

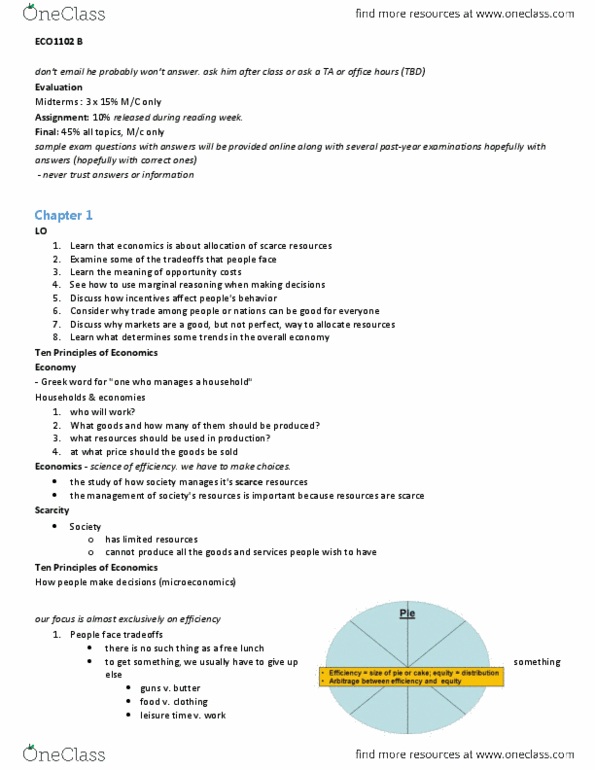

Labour aka human capital (the main factors of input/production whatever you use in a production process), physical capital (machines, computers, tools), Monopoly: even if you have one, you cannot charge the highest price (will not maximize your pro t because ppl demand will drop as people look for alternatives/substitutes. Car, cab, bikes instead of taking the bus). Even if there are no substitutes, charging very high is not a good way to maximize pro ts. Efficiency: the allocation of resources that maximizes total surplus (bene t) received by all members of a society. Equity: the fairness of distribution of well-being among the members of a society. How people make decisions: people face tradeoffs to get one thing you usually give up another. I. e. if you want to work 10 hrs instead of 8, then you have 2 hours less for leisure. Efficiency (bigger pie) vs equity (equal slices: opportunity cost what you give up to get what you want.