ECO100Y5 Study Guide - Final Guide: Human Capital, Monetarism, Aggregate Demand

53

ECO100Y5 Full Course Notes

Verified Note

53 documents

Document Summary

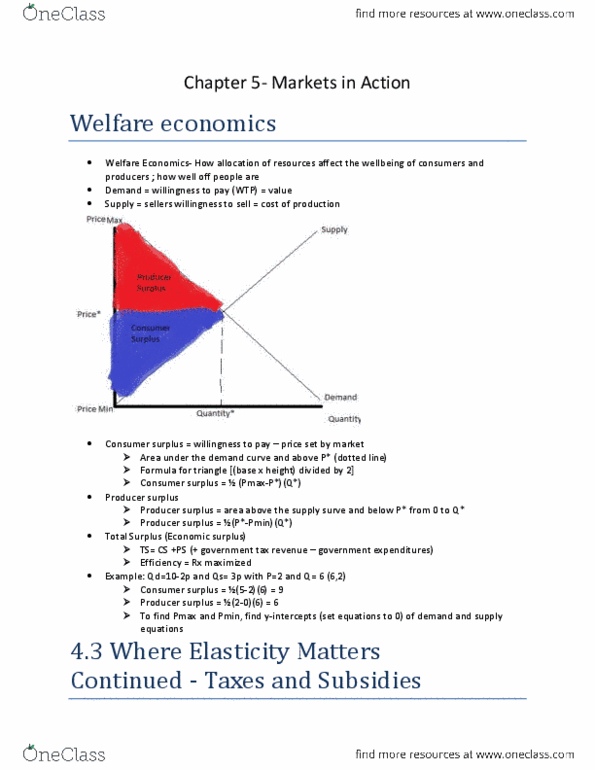

To find the opportunity cost - > you find the highest value out of all the values: $ 15, $ 10, ( 15 is the opportunity cost) Normative statement is a statement that cannot be backed. it is an opinion. Price ceiling: lead to excess demand, with the quantity exchanged being less than in the free market equilibrium. Price floor: a floor that is set at or below the equilibrium price has no effect beacuse free market equilibrium remains attainable. Club goods: museums, roads, marginal cost for letting one more person in is zero, fees are charged when goods become rivalous. Common property resources: water, lakes, grazing land, over use becomes a problem. Mc = change in tc / change in q. R = p x q average revenue = p x q / q marginal revenue = change in total revenue / change in quantity change in deposit = change in reserve x 1/rr.