MGAC50H3 Study Guide - Final Guide: Property Income

Document Summary

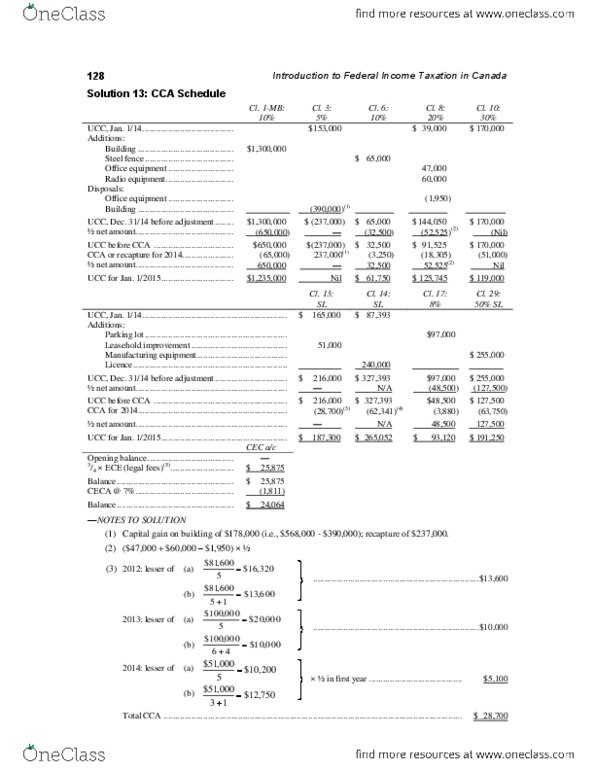

Solution 23: income and taxable income, ordering rules. Taxable income (equal to personal and employment tax credit bases) ,000 ,000 (carried forward from 2010 [sec. ,000 1/2 = (2) personal-use property losses denied. (3) other capital property 2014. Allowable capital losses (1/2 ,000) $ Less: allowable business investment loss applied in par. Balance which can be carried forward or backward as a net capital loss $ 375 (4) (a) rrsp contribution deduction for 2013 would be limited by the lesser of: (i) 18% of 2012 earned income (,250) = ,985 (ii) ,820. Unused rrsp contribution room to be carried forward (,985 ,000) $ (b) rrsp deduction for 2014 would be limited to the lesser of: (i) 18% of 2013 earned income (see below: ,000) = ,160 (ii) ,270. 2013 (i) net tcgs for the year $ 4,500 (ii) total adjusted net cls* $ 25,000. $ 20,875 (6) non-capital loss arising in 2010 $ 33,000 (19,808)