ECO100Y1 Study Guide - Gross Domestic Product

72 views2 pages

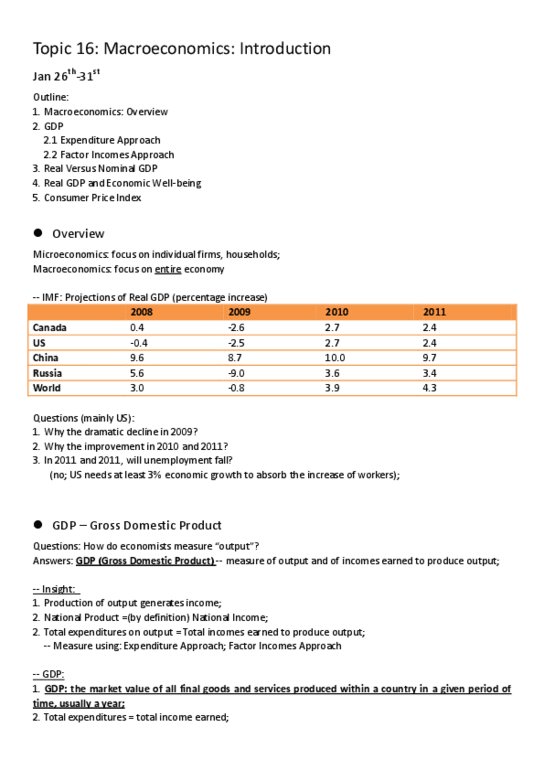

Document Summary

Each firm"s contribution to total output is equal to its value added. Value added = value of firm"s output - values of all intermediate goods and services. Sum of all values added produced in an economy is the economy"s total output (gdp) Gross domestic product (gdp): total value of goods and services produced in the economy during a given period. Expenditure approach: gdp = ca + ia + ga + (xa - ima) Ia = investment in plant and equipment, residential construction, inventory accumulation. Ga = government purchases of goods and services (xa - ima) = net exports of goods and services. Personal income: c + s + personal taxes. Desired aggregate expenditure (ae): sum of desired or planned spending on domestic output by households, firms, governments, and foreigners. Ae = c + i + g + (x - im) Net domestic income: ae - cca (depreciation) - indirect taxes (less subsidies)

Get access

Grade+20% off

$8 USD/m$10 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

40 Verified Answers

Related textbook solutions

Related Documents

Related Questions

|

||||||||||||

|

||||||||||||

|

|

||||||||||||

|

|

||||||||||||

|

|

||||||||||||

|

||||||||||||

|

||||||||||||

|

|

||||||||||||

|

|

||||||||||||

|

|

||||||||||||

|

||||||||||||

|

||||||||||||

|

|

||||||||||||

|

|

||||||||||||

|

|

||||||||||||

|

||||||||||||

|

||||||||||||

|

|

||||||||||||

|

|

||||||||||||

|

|

||||||||||||

|

||||||||||||

|

j