RSM424H1 Study Guide - Final Guide: Capital Gain, Small Business

11 Jun 2017

School

Department

Course

Professor

Document Summary

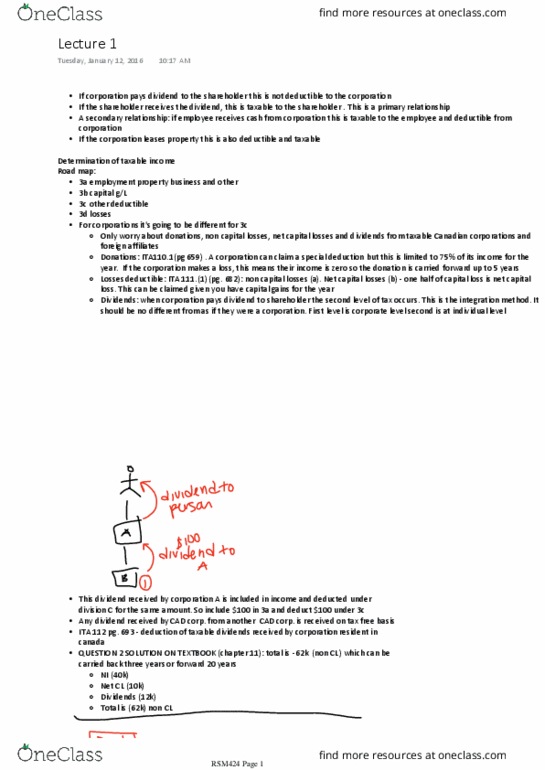

Ita s55(2) deemed proceeds or gain [capital gain stripping] Usually specify r/e amount (earned after 1971) safe income xx xx (xx) Less: safe income (=r/e: designated as a separate dividend) Note that an election is required to have the two dividends ([deemed dividend r/e] & [r/e]) treated as separate dividends. Without the election, the entire deemed dividend would be re- characterized as proceeds. > r/e, we need to adjust the proceeds of disposition since tax-free proceeds is not enough to pay for the non-taxable dividend xx xx (x) xx. In general terms, a sbc is a ccpc with 90% or more of the fmv of its assets: Used in an active business carried on in canada by the corporation or a related corporation, or. Shares or debts of a connected sbc, or. At any time (determination time), a share that meets the following tests: Sbc test: an sbc at determination time, owned by.