RSM100Y1 Study Guide - Telemarketing, Price Skimming

Document Summary

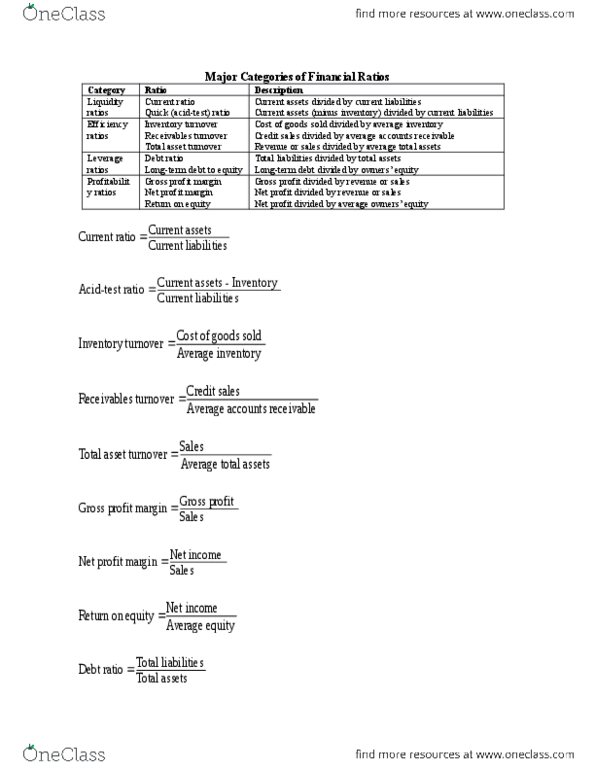

Inventory tu rnover ratio: measures average number of times inventory is sold and restocked, or how quickly inventory is produced and sold. Average inventory is the start-of-the-year inventory + end-year inventory divided by two. Accounting is a comprehensive information system for collecting, analyzing, and communicating financial information, measuring business performance and translating them into management decisions. Bookkeeping, on the other had, is just the recording of accounting transactions. The accounting i nformation system (ais) is an organized procedure for identifying, measuring, recording, and retaining financial information so that it can be used in statements and management reports. People who use this information include: business managers, employees and unions. Investors and creditors: tax authorities, the government. Controller is the head of ais, someone who manages all of the accounting activities of the firm. Financial accounting notifies external users about the activities of the company as a whole.