ACCT 1510 Final: Principles of Financial Accountring - FULL notes for review (Ch. 1-10)

20 Jun 2018

School

Department

Course

Professor

CHAPTER 1 – Accounting and the Financial Statements

- Accounting = the process of identifying, measuring, recording, and communicating financial

information about a company’s business activities so that decision makers can make

informed decisions

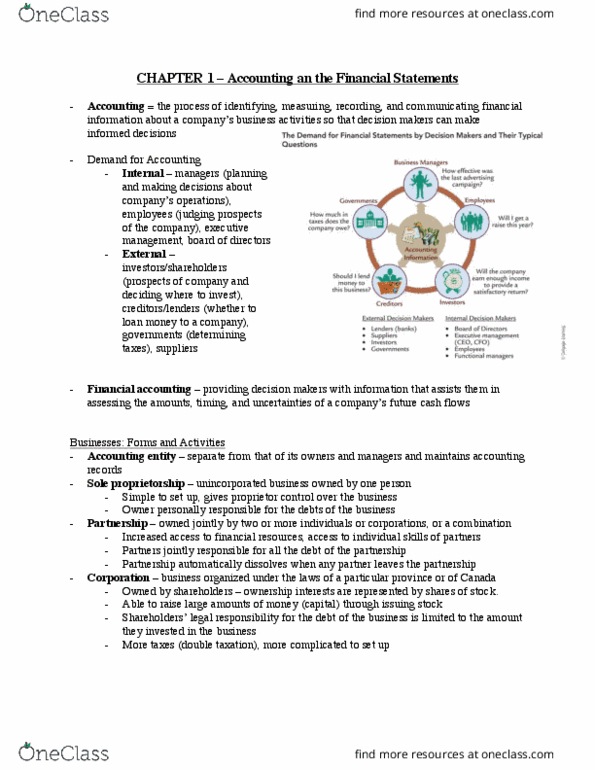

- Demand for Accounting

- Internal – managers (planning

and making decisions about

company’s operations),

employees (judging prospects

of the company), executive

management, board of directors

- External –

investors/shareholders

(prospects of company and

deciding where to invest),

creditors/lenders (whether to

loan money to a company),

governments (determining

taxes), suppliers

- Financial accounting – providing decision makers with information that assists them in

assessing the amounts, timing, and uncertainties of a company’s future cash flows

Businesses: Forms and Activities

- Accounting entity – separate from that of its owners and managers and maintains accounting

records

- Sole proprietorship – unincorporated business owned by one person

- Simple to set up, gives proprietor control over the business

- Owner personally responsible for the debts of the business

- Partnership – owned jointly by two or more individuals or corporations, or a combination

- Increased access to financial resources, access to individual skills of partners

- Partners jointly responsible for all the debt of the partnership

- Partnership automatically dissolves when any partner leaves the partnership

- Corporation – business organized under the laws of a particular province or of Canada

- Owned by shareholders – ownership interests are represented by shares of stock.

- Able to raise large amounts of money (capital) through issuing stock

- Shareholders’ legal responsibility for the debt of the business is limited to the amount

they invested in the business

- More taxes (double taxation), more complicated to set up

Business Activities

- Financing Activities – obtaining funds necessary to start and operate a business, through

shares (equity) or borrowing money (debt)

- Creditor – person to whom the corporation owes money (ex. bank)

- Liability – the obligation to repay a creditor

- Notes payable – borrowing money with promise to repay amount borrow plus

interest

- Bond payable – type of note payable, for large amounts of money

- Common stock – dollar amount paid to a corporation for shares, basic ownership in a

corporation

- Dividends – distribution of a portion of company’s earnings to shareholders

- Assets – economic resources of a corporation, creditors and shareholders have a

claim to them

- Shareholder’s liabilities – residual interest in the assets of a corporation that remain

after deducting its liabilities, to be paid out after liabilities are paid out

- Investing Activities – buying assets that enable operation

- Property, plant, equipment (land, buildings, machinery), intangible assets (copyrights,

patents)

- Assets – future economic benefits that a corporation controls

- Operating Activities – to generate revenue

- Revenue – the increase in assets that results from the sale of products and services

- Results of operating activities – cash, accounts receivable (the right to collect and

amount due from customers), supplies, inventory (products held for resale)

- Short-term cash needs – establishing line of creditors with company’s bank (lender)

- Expenses – the costs of assets used, or liabilities created, in the operation of the

business

- Liabilities

- Account payable – obligation to

repay a supplier for goods

purchased on credit

- Wages payable – amounts owed

to employees for work performed

- Incomes taxes payable – taxes

owed to the government

- Net income – revenues > expenses

- Net loss – expenses > revenues

Four basic Financial Statements:

- Financial statement – set of standardized reports, detailing and summarizing transactions

- provide information that will assist investors, creditors, and others make judgement

and predictions that will serve as the basis for the various decisions they make

1. Statement of Financial Position (Balance Sheet)

- Reports the resources (assets) owner by a company and the claims against those resources

(liabilities and shareholder’s equity) at a specific point in time

- How a company obtained its resources

- Whether a company will be able to pay back its obligations when they become due

Fundamental accounting equation:

Resources (what it owns) = Sources of Financing (what it owes)

Assets = Liabilities + Shareholders’ Equity

a. Assets:

- Current Assets – can be converted into cash within one year (or slightly longer,

depending on operating cycle) – listed in order of liquidity

- Cash

- Short-term investment or marketable securities – investments in the debt and

shares of other companies; government securities held for sale in the next fiscal

year (cash invested in cash and bonds (bonds-can immediately resell)

- Accounts receivable – the right to collect and amount due from customers

- Inventories – goods or products held for resale to customers

- Other current assets – ex. Prepaid expenses (rent, insurance etc.) and supplies

- Non-current assets – takes over a year to convert into cash

- Long-term (capital) investments – ex. shares, bonds, real estate

- Property, plant and equipment – tangible, long-lived, productive assets used by

a company to produce revenue (ex. buildings, land, equipment)

- Accumulated depreciation (contra-asset account) – companies allocate

a portion of the asset’s coast as an expense in each period in which the

asset is used (the cost is spread across several years)

- Intangible Assets – provide a benefit to the company over a number of years, but

lack physical substance (ex. goodwill, patents, copyrights)

Document Summary

Chapter 1 accounting and the financial statements. Accounting = the process of identifying, measuring, recording, and communicating financial information about a company"s business activities so that decision makers can make informed decisions. Internal managers (planning and making decisions about company"s operations), employees (judging prospects of the company), executive management, board of directors. External investors/shareholders (prospects of company and deciding where to invest), creditors/lenders (whether to loan money to a company), governments (determining taxes), suppliers. Financial accounting providing decision makers with information that assists them in assessing the amounts, timing, and uncertainties of a company"s future cash flows. Accounting entity separate from that of its owners and managers and maintains accounting records. Sole proprietorship unincorporated business owned by one person. Simple to set up, gives proprietor control over the business. Owner personally responsible for the debts of the business. Partnership owned jointly by two or more individuals or corporations, or a combination.