Business Administration 1220E Study Guide - Sensitivity Analysis, Floating Charge, Making Money

2 Dec 2012

School

Department

Professor

40

Business Administration 1220E Full Course Notes

Verified Note

40 documents

Document Summary

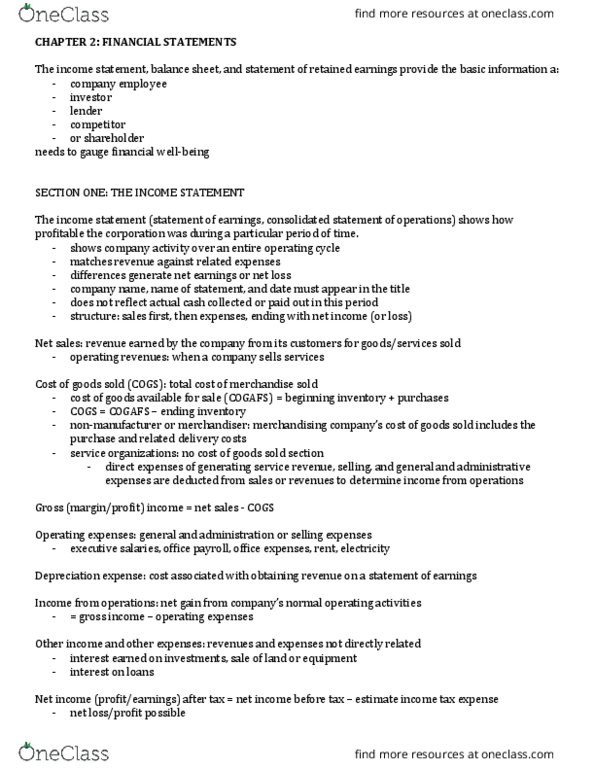

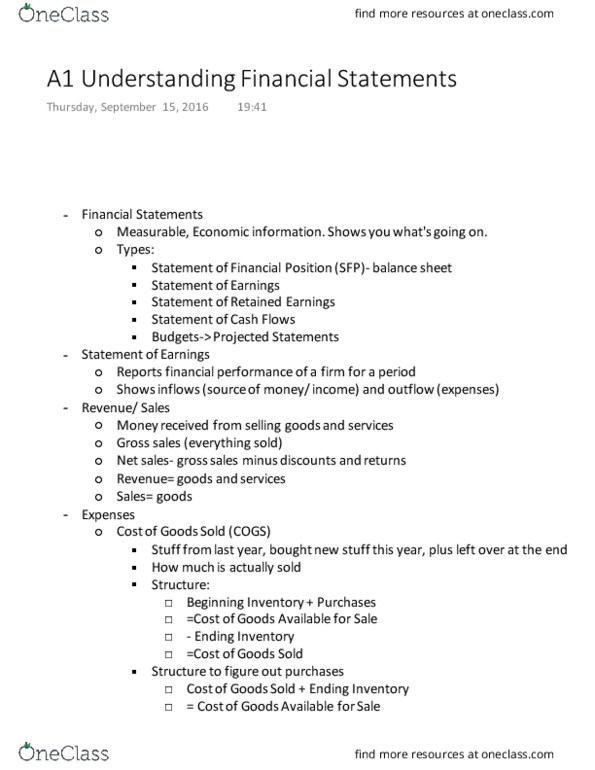

The basics statement of earnings, balance sheet and statement of. How much money an organization is making over a period of time. Matches the revenue generated from selling goods or services against the expenses used to generate them the difference will result in a net earnings or net loss. Beginning inventory + purchases = cogafs ending inventory = cogs. Non-manufacturer- includes the purchase and delivery costs. Manufacturer- reflects all costs associated with the transformation of unprocessed raw materials into finished good available for sale. Serve organizations no product, direct expenses of generating service revenue. Company name, statement name, date at top. Includes depreciation expense (how much the asset lost value just this year) Only depreciate the asset for as long as it exists (ex: new renovation, only depreciate it when it is finished) If a year starts in january and the renovation is finished in march, only depreciate it for.