[Management and Organizational Studies 3370A/B] - Final Exam Guide - Comprehensive Notes for the exam (112 pages long!)

29 Nov 2016

School

Department

Professor

Document Summary

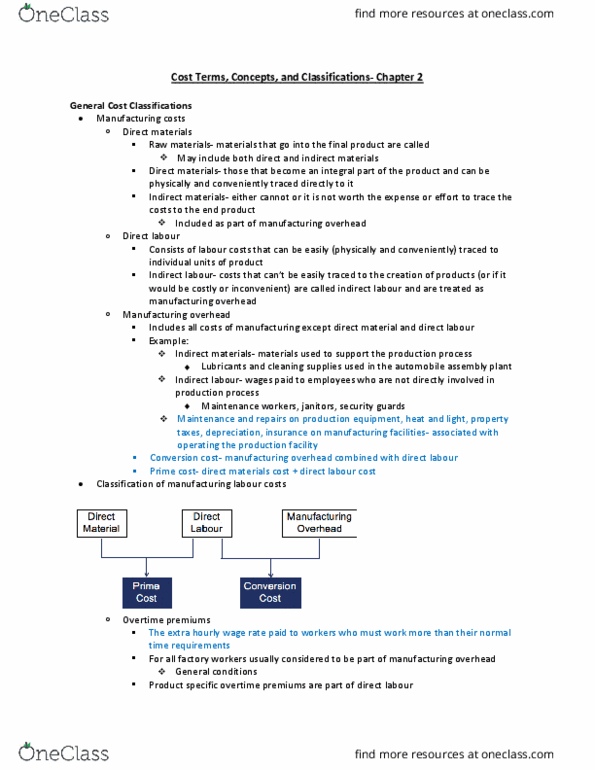

Lecture 2 ch2/3 summary of cost classifications. Classification of costs manufacturing costs often classified as following: direct material and direct material = prime cost direct labour and manufacturing overhead = conversion cost. Administrative costs all executive, organization, clerical costs. Product costs include direct materials, labour, and manufacturing overhead: all costs involved in acquiring or making product attached to product, inventory transferred to cogs expense account. Period costs include all selling and administrative costs: directly expensed in period they are occurred. Current assets: cash, receivables, prepaids, merchandise inventory. Current assets: cash, receivables, prepaid expenses, inventories. Raw materials material waiting to be processed. Cogs for manufacturers differs only slightly from cogs for merchandisers. Beginning balance + additions to inventory = ending balance + withdrawals from inventory: o/b + additions = total available withdrawals = ending balance. Calculates the cost of rm, dl, and moh used in production.