BU111 Study Guide - Final Guide: Tax Bracket, Tax Rate, Surtax

19

BU111 Full Course Notes

Verified Note

19 documents

Document Summary

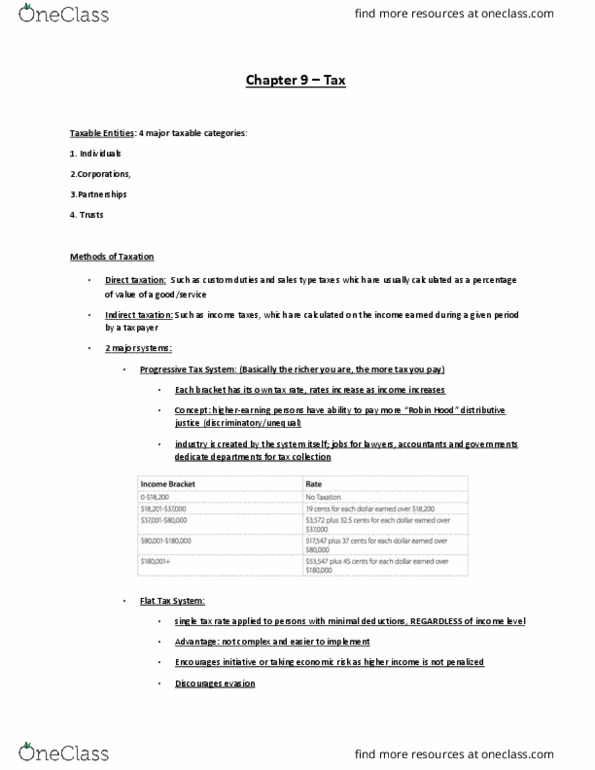

Personal tax law: pertains to taxation of individuals, pertains to the taxation of unincorporated businesses (sole proprietorships, partnerships) Corporate tax law: pertains to the taxation of private and public corporations. A graduated or progressive system based on an individual taxpayer"s level of taxable income: taxable income = total income allowable deductions. The higher an individual"s level of taxable income, the higher that individual"s marginal tax rate the more you make, the more you pay! Three different levels of tax must be paid by individuals living in ontario: federal tax (canada, provincial tax (ontario, provincial surtax (ontario) Marginal tax rate definition: strict definition: tax rate paid by an investor on his/her last dollar of taxable income earned. More useful definition: given tax bracket: the rate of tax applied to every dollar of taxable income earned within a. Determining an ontario resident"s marginal tax rate for 2010.