BU127 Study Guide - Midterm Guide: Bank Reconciliation, Accounts Receivable

6

BU127 Full Course Notes

Verified Note

6 documents

Document Summary

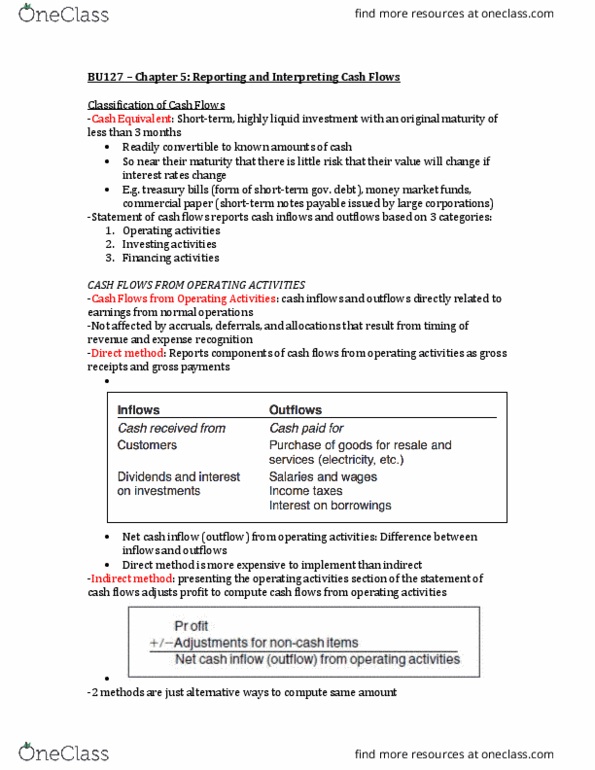

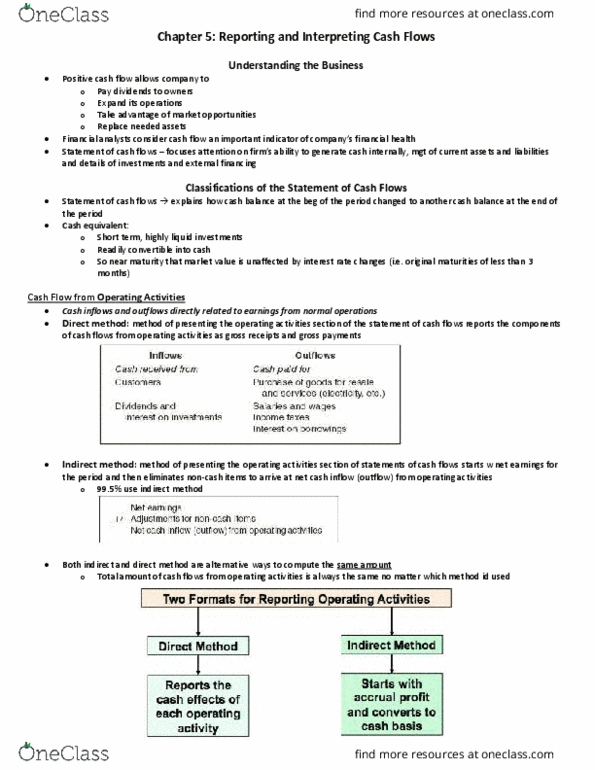

Must also be comparable, verifiable, timely, and understandable. Statement of cash flows (three sections: cash flows from operating activities, cash flows from investing activities, cash flows from financing activities. Additional (non-money) detailed supporting reported amounts in statements (revenue analysis, schedule of long-term assets, original cost, accumulated depreciation, carrying amounts) Relevant financial information not disclosed on the statements (stock options, legal matters, subsequent events) Chapter 7 reporting and interpreting sales revenue, receivables and cash. When you account for these items remember they reduce sales revenue and have a debit balance. Ex: visa charges 4% fee for credit card service: Debit accounts receivable for (3000 x 96%) = 2880. Bad debt expense is the expense associated with the estimated uncollectable trade receivables. Recorded in the journal at the end of the accounting period. Two methods: aging of trade receivables method, percentage of credit sales method. Focus on determining the desired balance in allowance for doubtful accounts on the balance sheet.