BU227 Study Guide - Final Guide: Cash Flow Statement, International Financial Reporting Standards, Deferral

Document Summary

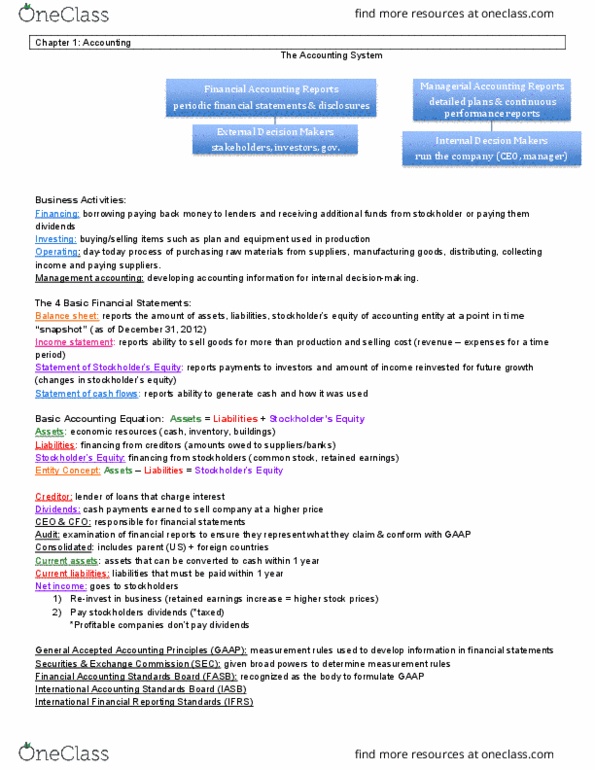

Bu227 introduction to financial accounting master note sheet. David scallen"s office: peters 2072 dscallen @ wlu. ca extension 2880. Cash flow statement profit is not the same as cash. (pay attention to this especially with a/r and a/p!) Totals net cash change for the period. Investing (from bu121: seems to have opposing effects of a balance sheet) Beginning retained earnings dividends + net income = ending retained earnings. Financial accounting: external use (by outsiders from the company) On track: if not, give an explanation as to why. Give key indicators to financial statements: a, l, oe changes, cash flow from one period to the next. While quarterly is most popular, never report less often than annually. Weekly: key report (had to have results of the previous week by a certain day of the current week) Scallen: worked in the food industry (those who were saying that scallen was an expert in the poultry industry weren"t lying. )