ACTG 2010 Study Guide - Final Guide: Current Liability

Document Summary

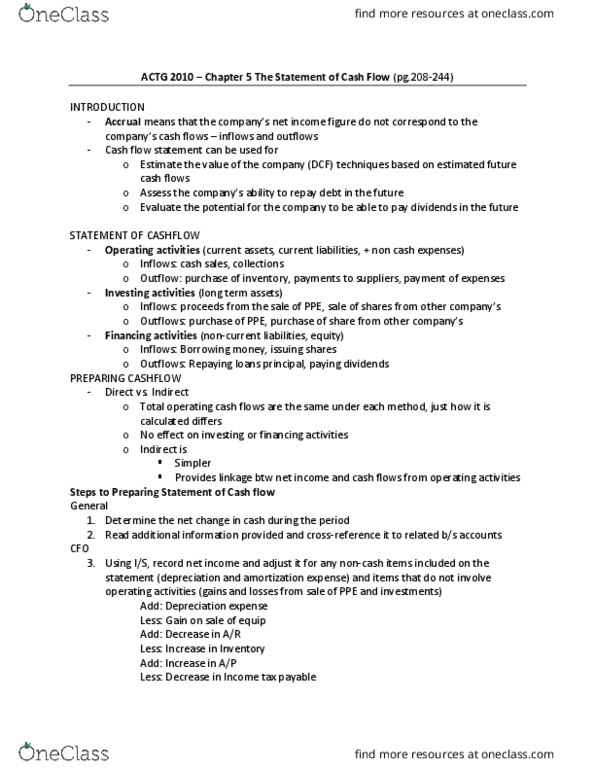

Cash flow statement that tells you in and outflow of cash cash is 1st item on statement of financial position reconciling change of cash on balance sheet from opening to closing. 3 elements (in this order: operating activities. Current assets, current liabilities & profit on balance sheet. Outflow: paying suppliers/buying inventory, paying rent for building, paying salaries. 2 methods: direct preferred under ifrs. Indirect most commonly used (focusing on this one: operating activities. Net income: add back/subtract any non cash item (+ depreciation expense) (- gain on disposal of assets) (+ write off assets) Increase in ar cash outflow: decrease in ar cash inflow. Increase in inventory cash outflow: decrease in inventory cash inflow, decrease in ap cash outflow. Increase in ap cash inflow: investing activities. Capital assets, equity (with surplus cash) ex. acquiring a new company. Inflow: selling long term assets, selling investments: financing activities. Non current liabilities, share capital and dividends on balance sheet.