ACTG 2011 Study Guide - Midterm Guide: Gross Margin, Cash Flow, Current Liability

Document Summary

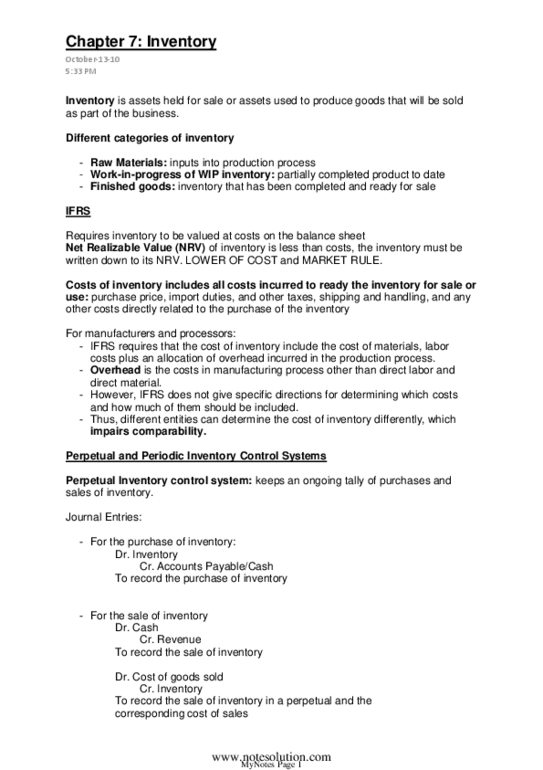

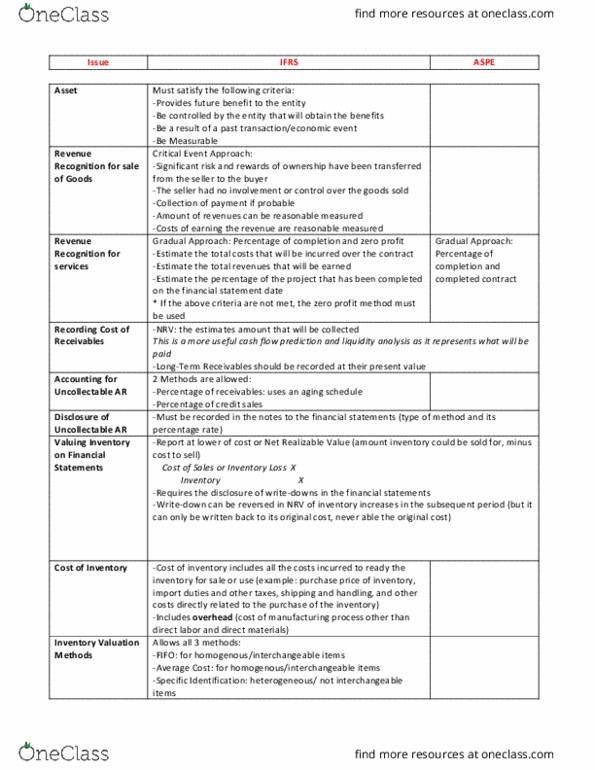

Actg 2011 midterm notes (chapter 7 chapter 9) Goods available for production (raw materials, wip, materials used in supplying service- which are expensed when revenue is recognized) Ifrs states that exclusions of overheard are: storage, administration costs, selling and marketing, and waste. Aspe doesn"t have to include overhead costs. Overhead costs can be expensed instead minimize taxes. Inventory systems (choice b/w system is an internal control issue) Revenue: @ end of the period (adjusting entry) Dr. cogs [= bi + purchases ei) Purchases: purchases is an expense account; purchases aren"t recognized as revenue (but at end of period it"s all the same, cost of stolen items automatically included in cogs; weakness b/c can"t tell if there"s a problem with theft. Pose internal control issues: need to count inventory; have security procedures, segregation of duties so that managers can fulfill stewardship responsibilities; if not theft: miscount, lost, misplaced. When overload of storage: can signify impairment recommend lcm cost.