ADMS 1010 Study Guide - Midterm Guide: Mania, Neede, Investment Banking

11 Dec 2012

School

Department

Course

Professor

Document Summary

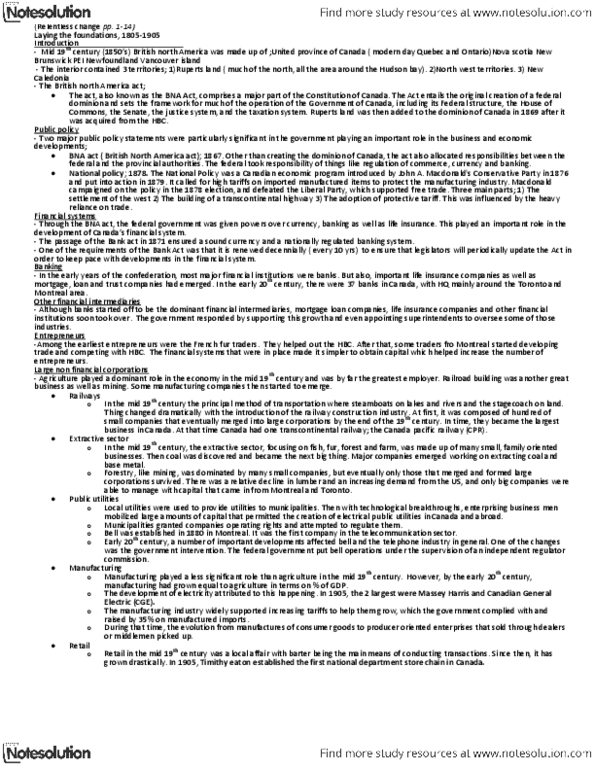

1850, british north america made up the upc, ns, nb, pei newfie, and vancouver. Interior of northern part of bna contained rupert s land (owned by hbc); nwt, and nc. 1867, parliament passed bna act creating the dominion of can. Canadas + ns + nb becoming provinces of the new dominion. 1869, dominion of can. expanding quickly and acquired rupert s land from hbc. Early 20c, can. had become a great colony of the crown and was on its way to becoming a nation. growing geographically and economically. 1850-early 20c, can s gdp more than double; 10th richest nation in the world. Accomplished through a blend of public policy, sound financial system, energetic entrepreneurship, and large non-corporations. Public policy: late 19c bna of 1867 and np of 1878. 1854, lord elgin british gg of can. Washington to negotiate reciprocity treaty in natural unprocessed goods between us and bna. 1860, reciprocity treaty short-lived when protectionist republicans was voted into power.