FINE 2000 Study Guide - Final Guide: Inventory Turnover, Asset Turnover, Cash Cash

138 views33 pages

Document Summary

Leverage ratios (how heavily the company is in debt): Value of total leases; the amount of every dollar of long-term capital which is in the form of ltd (ltd + value of leases) Ltd + value of leases + preferred equity + common equity. The amount of debt financing (as compared to equity financing) The extent to which interest is covered by earnings (banks prefer to lend to firms whose earnings are far in excess of interest payments) The extent to which interest is covered by the cash flow from operations. Interest payments + (current debt repayment + current lease obligations)/(1-tax rate) How many times greater ebit plus depreciation and amortization is relative to the fixed charges the company is obliged to make. Liquidity ratios (how easily a firm can lay its hands on cash): A rough measure of the company"s potential reservoir of cash; nwc as a proportion of total assets. *net working capital = current assets current liabilities.

Get access

Grade+20% off

$8 USD/m$10 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

40 Verified Answers

Related Documents

Related Questions

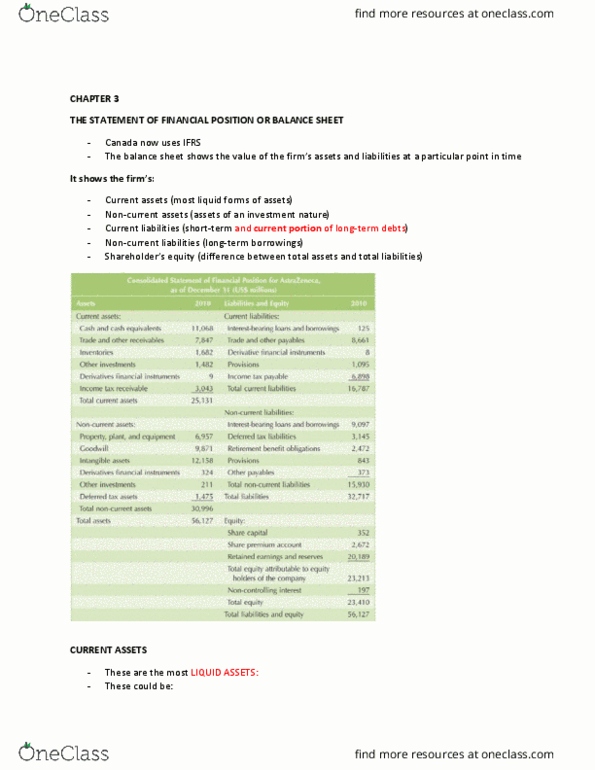

| Joshua & White Technologies: December 31 Balance Sheets | ||||||

| (Thousands of Dollars) | ||||||

| Assets | 2010 | 2009 | ||||

| Cash and cash equivalents | $21,000 | $20,000 | ||||

| Short-term investments | 3,759 | 3,240 | ||||

| Accounts Receivable | 52,500 | 48,000 | ||||

| Inventories | 84,000 | 56,000 | ||||

| Total current assets | $161,259 | $127,240 | ||||

| Net fixed assets | 218,400 | 200,000 | ||||

| Total assets | $379,659 | $327,240 | ||||

| Liabilities and equity | ||||||

| Accounts payable | $33,600 | $32,000 | ||||

| Accruals | 12,600 | 12,000 | ||||

| Notes payable | 19,929 | 6,480 | ||||

| Total current liabilities | $66,129 | $50,480 | ||||

| Long-term debt | 67,662 | 58,320 | ||||

| Total liabilities | $133,791 | $108,800 | ||||

| Common stock | 183,793 | 178,440 | ||||

| Retained Earnings | 62,075 | 40,000 | ||||

| Total common equity | $245,868 | $218,440 | ||||

| Total liabilities and equity | $379,659 | $327,240 | ||||

| Joshua & White Technologies December 31 Income Statements | ||||||

| (Thousands of Dollars) | ||||||

| 2010 | 2009 | |||||

| Sales | $420,000 | $400,000 | ||||

| Expenses excluding depr. and amort. | 327,600 | 320,000 | ||||

| EBITDA | $92,400 | $80,000 | ||||

| Depreciation and Amortization | 19,660 | 18,000 | ||||

| EBIT | $72,740 | $62,000 | ||||

| Interest Expense | 5,740 | 4,460 | ||||

| EBT | $67,000 | $57,540 | ||||

| Taxes (40%) | 26,800 | 23,016 | ||||

| Net Income | $40,200 | $34,524 | ||||

| Common dividends | $18,125 | $17,262 | ||||

| Addition to retained earnings | $22,075 | $17,262 | ||||

| Other Data | 2010 | 2009 | ||||

| Year-end Stock Price | $90.00 | $96.00 | ||||

| # of shares (Thousands) | 4,052 | 4,000 | ||||

| Lease payment (Thousands of Dollars) | $20,000 | $20,000 | ||||

| Sinking fund payment (Thousands of Dollars) | $0 | $0 | ||||

| Ratio Analysis | 2010 | 2009 | Industry Avg | |||

| Liquidity Ratios | ||||||

| Current Ratio | 2.38 | 2.52 | 2.58 | |||

| Quick Ratio | 1.17 | 1.41 | 1.53 | |||

| Asset Management Ratios | ||||||

| Inventory Turnover | 1.11 | 1.22 | 7.69 | |||

| Days Sales Outstanding | 45.63 | 43.80 | 47.45 | |||

| Fixed Assets Turnover | 1.92 | 2.00 | 2.04 | |||

| Total Assets Turnover | 3.81 | 5.64 | 1.23 | |||

| Debt Management Ratios | ||||||

| Debt Ratio | 32.1% | |||||

| Times-interest-earned ratio | 15.33 | |||||

| EBITDA coverage ratio | 4.18 | |||||

| Profitability Ratios | ||||||

| Profit Margin | 9.57% | 8.63% | 8.86% | |||

| Basic Earning Power | 19.16% | 18.95% | 19.48% | |||

| Return on Assets | 10.59% | 10.55% | 10.93% | |||

| Return on Equity | 21.87% | 19.35% | 16.10% | |||

| Market Value Ratios | ||||||

| Earnings per share | NA | |||||

| Price-to-earnings ratio | 10.65 | |||||

| Cash flow per share | NA | |||||

| Price-to-cash flow ratio | 7.11 | |||||

| Book Value per share | NA | |||||

| Market-to-book ratio | 1.72 | |||||

| a. Has Joshua & White's liquidity position improved or worsened? Explain. | ||||||

| The position of JW has worsend because there ration has fallen from 1.41 to 1.17 | ||||||

| b. Has Joshua & White's ability to manage its assets improved or worsened? Explain. | ||||||

| c. How has Joshua & White's profitability changed during the last year? | ||||||

| d. Perform an extended Du Pont analysis for Joshua & White for 2008 and 2009. | ||||||

| ROE = | PM x | TA Turnover x Equity Multiplier | ||||

| 2010 | ||||||

| 2009 | ||||||

| e. Perform a common size analysis. What has happened to the composition | ||||||

| (that is, percentage in each category) of assets and liabilities? | ||||||

| Common Size Balance Sheets | ||||||

| Assets | 2010 | 2009 | ||||

| Cash and cash equivalents | ||||||

| Short-term investments | ||||||

| Accounts Receivable | ||||||

| Inventories | ||||||

| Total current assets | ||||||

| Net fixed assets | ||||||

| Total assets | ||||||

| Liabilities and equity | 2010 | 2009 | ||||

| Accounts payable | ||||||

| Accruals | ||||||

| Notes payable | ||||||

| Total current liabilities | ||||||

| Long-term debt | ||||||

| Total liabilities | ||||||

| Common stock | ||||||

| Retained Earnings | ||||||

| Total common equity | ||||||

| Total liabilities and equity | ||||||

| Common Size Income Statements | 2010 | 2009 | ||||

| Sales | ||||||

| Expenses excluding depr. and amort. | ||||||

| EBITDA | ||||||

| Depreciation and Amortization | ||||||

| EBIT | ||||||

| Interest Expense | ||||||

| EBT | ||||||

| Taxes (40%) | ||||||

| Net Income | ||||||

| f. Perform a percent change analysis. What does this tell you about the change in profitability | ||||||

| and asset utilization? | ||||||

| Percent Change Balance Sheets | Base | |||||

| Assets | 2010 | 2009 | ||||

| Cash and cash equivalents | ||||||

| Short-term investments | ||||||

| Accounts Receivable | ||||||

| Inventories | ||||||

| Total current assets | ||||||

| Net fixed assets | ||||||

| Total assets | ||||||

| Base | ||||||

| Liabilities and equity | 2010 | 2009 | ||||

| Accounts payable | ||||||

| Accruals | ||||||

| Notes payable | ||||||

| Total current liabilities | ||||||

| Long-term debt | ||||||

| Total liabilities | ||||||

| Common stock | ||||||

| Retained Earnings | ||||||

| Total common equity | ||||||

| Total liabilities and equity | ||||||

| Base | ||||||

| Percent Change Income Statements | 2010 | 2009 | ||||

| Sales | ||||||

| Expenses excluding depr. and amort. | ||||||

| EBITDA | ||||||

| Depreciation and Amortization | ||||||

| EBIT | ||||||

| Interest Expense | ||||||

| EBT | ||||||

| Taxes (40%) | ||||||

| Net Income | ||||||

| Joshua & White Technologies: December 31 Balance Sheets | ||||||

| (Thousands of Dollars) | ||||||

| Assets | 2010 | 2009 | ||||

| Cash and cash equivalents | $21,000 | $20,000 | ||||

| Short-term investments | 3,759 | 3,240 | ||||

| Accounts Receivable | 52,500 | 48,000 | ||||

| Inventories | 84,000 | 56,000 | ||||

| Total current assets | $161,259 | $127,240 | ||||

| Net fixed assets | 218,400 | 200,000 | ||||

| Total assets | $379,659 | $327,240 | ||||

| Liabilities and equity | ||||||

| Accounts payable | $33,600 | $32,000 | ||||

| Accruals | 12,600 | 12,000 | ||||

| Notes payable | 19,929 | 6,480 | ||||

| Total current liabilities | $66,129 | $50,480 | ||||

| Long-term debt | 67,662 | 58,320 | ||||

| Total liabilities | $133,791 | $108,800 | ||||

| Common stock | 183,793 | 178,440 | ||||

| Retained Earnings | 62,075 | 40,000 | ||||

| Total common equity | $245,868 | $218,440 | ||||

| Total liabilities and equity | $379,659 | $327,240 | ||||

| Joshua & White Technologies December 31 Income Statements | ||||||

| (Thousands of Dollars) | ||||||

| 2010 | 2009 | |||||

| Sales | $420,000 | $400,000 | ||||

| Expenses excluding depr. and amort. | 327,600 | 320,000 | ||||

| EBITDA | $92,400 | $80,000 | ||||

| Depreciation and Amortization | 19,660 | 18,000 | ||||

| EBIT | $72,740 | $62,000 | ||||

| Interest Expense | 5,740 | 4,460 | ||||

| EBT | $67,000 | $57,540 | ||||

| Taxes (40%) | 26,800 | 23,016 | ||||

| Net Income | $40,200 | $34,524 | ||||

| Common dividends | $18,125 | $17,262 | ||||

| Addition to retained earnings | $22,075 | $17,262 | ||||

| Other Data | 2010 | 2009 | ||||

| Year-end Stock Price | $90.00 | $96.00 | ||||

| # of shares (Thousands) | 4,052 | 4,000 | ||||

| Lease payment (Thousands of Dollars) | $20,000 | $20,000 | ||||

| Sinking fund payment (Thousands of Dollars) | $0 | $0 | ||||

| Ratio Analysis | 2010 | 2009 | Industry Avg | |||

| Liquidity Ratios | ||||||

| Current Ratio | 2.38 | 2.52 | 2.58 | |||

| Quick Ratio | 1.17 | 1.41 | 1.53 | |||

| Asset Management Ratios | ||||||

| Inventory Turnover | 1.11 | 1.22 | 7.69 | |||

| Days Sales Outstanding | 45.63 | 43.80 | 47.45 | |||

| Fixed Assets Turnover | 1.92 | 2.00 | 2.04 | |||

| Total Assets Turnover | 3.81 | 5.64 | 1.23 | |||

| Debt Management Ratios | ||||||

| Debt Ratio | 32.1% | |||||

| Times-interest-earned ratio | 15.33 | |||||

| EBITDA coverage ratio | 4.18 | |||||

| Profitability Ratios | ||||||

| Profit Margin | 9.57% | 8.63% | 8.86% | |||

| Basic Earning Power | 19.16% | 18.95% | 19.48% | |||

| Return on Assets | 10.59% | 10.55% | 10.93% | |||

| Return on Equity | 21.87% | 19.35% | 16.10% | |||

| Market Value Ratios | ||||||

| Earnings per share | NA | |||||

| Price-to-earnings ratio | 10.65 | |||||

| Cash flow per share | NA | |||||

| Price-to-cash flow ratio | 7.11 | |||||

| Book Value per share | NA | |||||

| Market-to-book ratio | 1.72 | |||||

| a. Has Joshua & White's liquidity position improved or worsened? Explain. | ||||||

| The position of JW has worsend because there ration has fallen from 1.41 to 1.17 | ||||||

| b. Has Joshua & White's ability to manage its assets improved or worsened? Explain. | ||||||

| c. How has Joshua & White's profitability changed during the last year? | ||||||

| d. Perform an extended Du Pont analysis for Joshua & White for 2008 and 2009. | ||||||

| ROE = | PM x | TA Turnover x Equity Multiplier | ||||

| 2010 | ||||||

| 2009 | ||||||

| e. Perform a common size analysis. What has happened to the composition | ||||||

| (that is, percentage in each category) of assets and liabilities? | ||||||

| Common Size Balance Sheets | ||||||

| Assets | 2010 | 2009 | ||||

| Cash and cash equivalents | ||||||

| Short-term investments | ||||||

| Accounts Receivable | ||||||

| Inventories | ||||||

| Total current assets | ||||||

| Net fixed assets | ||||||

| Total assets | ||||||

| Liabilities and equity | 2010 | 2009 | ||||

| Accounts payable | ||||||

| Accruals | ||||||

| Notes payable | ||||||

| Total current liabilities | ||||||

| Long-term debt | ||||||

| Total liabilities | ||||||

| Common stock | ||||||

| Retained Earnings | ||||||

| Total common equity | ||||||

| Total liabilities and equity | ||||||

| Common Size Income Statements | 2010 | 2009 | ||||

| Sales | ||||||

| Expenses excluding depr. and amort. | ||||||

| EBITDA | ||||||

| Depreciation and Amortization | ||||||

| EBIT | ||||||

| Interest Expense | ||||||

| EBT | ||||||

| Taxes (40%) | ||||||

| Net Income | ||||||

| f. Perform a percent change analysis. What does this tell you about the change in profitability | ||||||

| and asset utilization? | ||||||

| Percent Change Balance Sheets | Base | |||||

| Assets | 2010 | 2009 | ||||

| Cash and cash equivalents | ||||||

| Short-term investments | ||||||

| Accounts Receivable | ||||||

| Inventories | ||||||

| Total current assets | ||||||

| Net fixed assets | ||||||

| Total assets | ||||||

| Base | ||||||

| Liabilities and equity | 2010 | 2009 | ||||

| Accounts payable | ||||||

| Accruals | ||||||

| Notes payable | ||||||

| Total current liabilities | ||||||

| Long-term debt | ||||||

| Total liabilities | ||||||

| Common stock | ||||||

| Retained Earnings | ||||||

| Total common equity | ||||||

| Total liabilities and equity | ||||||

| Base | ||||||

| Percent Change Income Statements | 2010 | 2009 | ||||

| Sales | ||||||

| Expenses excluding depr. and amort. | ||||||

| EBITDA | ||||||

| Depreciation and Amortization | ||||||

| EBIT | ||||||

| Interest Expense | ||||||

| EBT | ||||||

| Taxes (40%) | ||||||

| Net Income | ||||||